WANT TO DISCOVER MORE?

he German federal government has declared its aim to reduce greenhouse gases to a level 55% lower than that of 1990. It goes so far as to envisage complete carbon neutrality by 2050, which is in harmony with the aims of the European Green Deal. In order to achieve this, about 14 million vehicles, or 30% of existing vehicles on the road in Germany, would have to be powered solely by electricity by 2030.

With these regulatory conditions in the background it seems understandable that most European automotive manufacturers are consolidating their exit strategies now and some are envisaging short-term withdrawal scenarios. Audi, for example, is planning the final sales run of its combustion engines for 2025, except for the Chinese market. Production of conventionally powered cars is due to finally end in 2033. Its allied brand Volkswagen and competitors such as BMW and Daimler are following similar approaches.

So the paradigm shift from classic combustion motor power to purring e-powertrain seems to be sealed. For the German supplier industry, which with a share of about 22 per cent is the second largest supplier in the global market, this opens up the opportunity to further develop their leading role.

An industrial standard for the high volt architecture (HV) of future vehicle platforms is being established in the electric powertrain sector. The battery system, the e-axis and high-performance electronics are the central components of the electrified powertrain. The battery system constitutes 70 to 80 per cent of the total cost of the powertrain. The concept of central HV architectures is increasingly prominent in the future vehicle platforms up to 2030, in which the individual components of the high-performance electronics are moved to one location at the rear. The aim of this is to gain significant advantages when it comes to material costs and system complexity.

High performance electronics have a significant effect on range, charging time and durability of vehicle batteries. This is another reason why automotive manufacturers increasingly consider installing power electronics like inverters, DC converters and control devices themselves, for part of this volume. In this way the manufacturers can develop their own evaluation skills alongside the established suppliers, and in the tendering process they can negotiate with the suppliers on an equal footing.

The components of the e-powertrain are increasingly subject to heavy pressure on prices, which is partly the result of economies of scale through rising unit sales and increasing customer acceptance of electric drive systems.

New registrations for electric vehicles rose during the past year by 264 per cent in Germany alone, and globally the increase was 38 per cent. By 2026 we estimate that the production of purely electric vehicles will rise by more than 200 per cent.

At the same time as the rise in volume, we can expect price reductions of up to 50 to 70 per cent for individual components in the e-powertrain. To counteract this, the big suppliers are increasingly entering development partnerships with semiconductor manufacturers. They are focusing on improvement of efficiencies in power electronics, in order to increase the range of battery-electric vehicles. Suppliers are hoping to counteract price reductions in the long term with technological innovations of this sort.

2021 is a decisive year for suppliers, as they need to get the tenders for the new e-platforms into position and thus secure their share of the e-mobility growth market. This also appears to be a targeted approach against a background of job retainment. Because of the planned discontinuation of the combustion business and the lower staff intensity needed to make electric engines, suppliers are under intense pressure to overcompensate for the expected gap with new projects in the e-mobility sector. The result is a bitter pricing competition for the benefit of the end customer, to make electromobility affordable for the general public.

Berylls Strategy Advisors would be happy to support you in this key decision process.

Arthur Kipferler complements the expertise of the Berylls partner team in the fields of market & customer, technologies, sales, and digitalization, as well as in the development and implementation of corporate, product, and regional strategies.

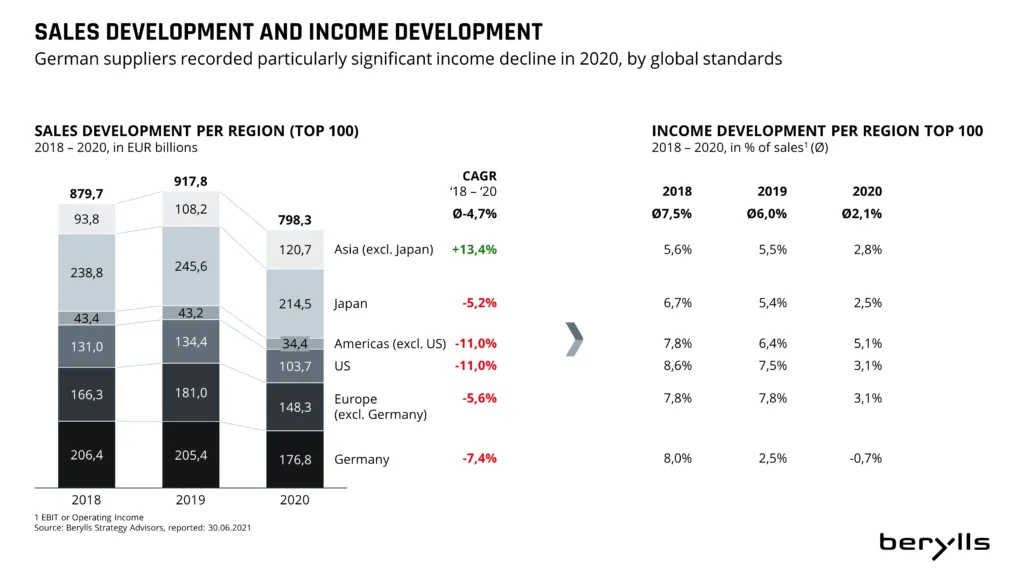

or automotive suppliers, the year 2020 was exceptional. The scale of the disruption can be summarized in four statements: growth was only really possible through acquisitions; one in four companies recorded losses; a Chinese supplier made it into the Top 100 for the first time, and electromobility set the direction for the whole industry.

Looking in more detail at the numbers, turnover among the 100 largest automotive suppliers as identified by Berylls Strategy Advisors was 12.7 per cent down compared with 2019, when turnover increased by 4.3 per cent. Profitability among the top 100 declined by 58.1 per cent in 2020 in comparison with the previous year, and the average margin of the companies surveyed stood at 2.6 per cent less in 2020 – less than a half of the 6 per cent achieved in 2019.

After a stormy year, for which the omens were already clear in 2019, the analysis by Berylls shows that whereas normally ten companies with the strongest growth in turnover could be selected, this time there were only eight. That was the number achieving a greater turnover than in the previous year. The 9th and 10th places in 2020 went to the two suppliers showing the least reduction in turnover in the Top 100. The main reasons for this are the effects of the Coronavirus pandemic. In the course of the past year both OEMs and suppliers had production stoppages. These stoppages along with reduced demand were the cause of significant loss of sales for the companies. It was mainly through acquisitions that companies such as BorgWarner (Delphi Technologies), Weichai Power (Aradex, VDS) or Infineon (Cypress) succeeded in increasing sales into a respectable double figure range.

There were mergers throughout the year. For example, Hitachi Automotive Systems, Keihin Corporation, Showa Corporation and Nissin Kogyo merged with the Japanese “Top 20” supplier (planned turnover for 2021 of 13 billion euros) Hitachi Astemo.

It was mainly the Coronavirus pandemic and the resulting production stoppages which caused sales drops for the automotive suppliers industry in the past year. Every second German supplier is currently planning additional job reductions because of the effects of the crisis. To add to this, sales fell considerably and costs did not fall to the same extent. One prominent example for the problems caused by the pandemic is the German cable and wiring specialist Leoni, which had already got into difficulties beforehand and is included in the 2020 Top 100 companies even with a negative margin. 80 factories belonging to this supplier all over the world were closed at various times, and the majority of its 4,800 staff in Germany were on short-time work. Rescue came in the form of a guarantee issued by Bavaria, Niedersachsen and Nordrhein-Westfalen for an operating loan. This prevented the company from going bankrupt, and it promises improvements in sales and results for the current year. Some smaller German suppliers which are not included in the Top 100 had to tread the path to insolvency in 2020, such as rim manufacturer BBS, the battery factory Moll, the aluminium casting experts Finoba, the plastic components manufacturer Weberit Dräbing, and the die-cast components manufacturer Minda KTSN. Some have already been taken over by investors or at least have the prospect of a restructuring. So the wave of bankruptcies announced in the previous year’s report has well and truly arrived. However, unlike the finance crisis of 2009 it has turned out to be a lot milder and mostly affects medium-sized companies in the supplier industry.

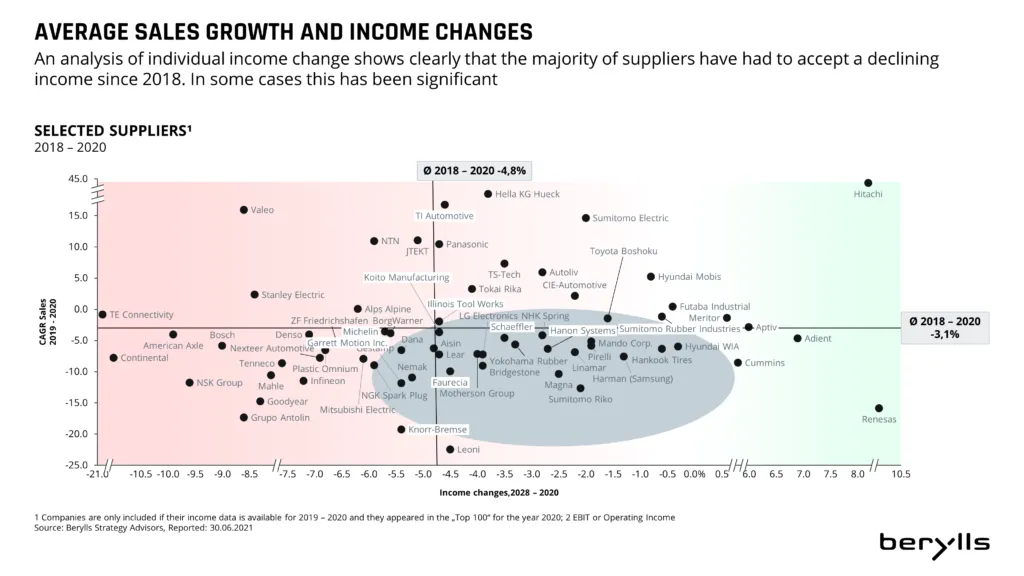

Five German and five Japanese Top 100 companies were making a loss in 2020 and account for over a half of the 17 suppliers with a negative margin. However, taken as a whole these companies are more like exceptions for Germany and Japan, as a total of 17 German and 27 Japanese automotive suppliers are represented in the Top 100. Germany’s loss-making companies are ZF Friedrichshafen, Continental, Bosch, Mahle and Leoni. The US loss-making companies range from American Axle which leads the loss-making companies with a -8.4 per cent operating income margin, to Goodyear which has a -0.1 per cent operating income margin and is the last on the negative list. Three Japanese companies are nudging zero growth: NTN (-1.1 percent OI), JTEKT (-0.7 per cent OI) and Denso (-0.7 per cent OI). The loss side consists of manufacturers from various fields, from mechanics to electronics.

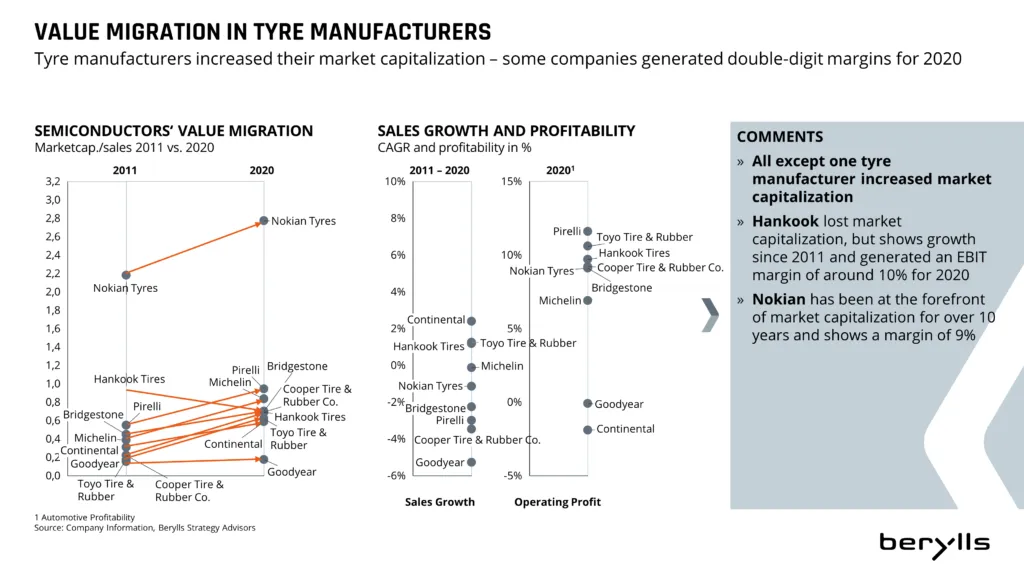

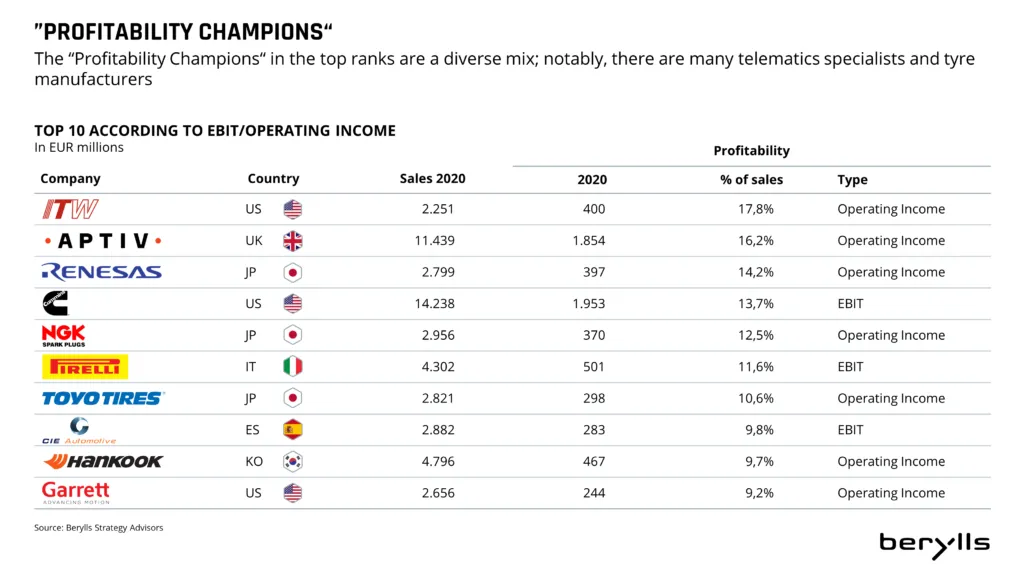

On the other side, this year’s “Profitability Champions“ are also from a very heterogeneous field. The most profitable companies occupying the top ten places are a varied mixture. The top performers come from six different countries and it is mostly telematic specialists and tyre manufacturers realizing positive margins. The top 3 most profitable companies in 2020 are Illinois Tool Works (USA, 17.8 per cent OI), Aptiv (Great Britain, 16.2 per cent OI), and Renesas (Japan, 14.2 per cent OI). The manufacturers with the highest margins were all tyre manufacturers: Pirelli (Italy, 11.6 per cent EBIT), Toyo Tire Corporation (Japan, 10.6 per cent OI), and Hankook Tires (Korea, 10.6 per cent OI). This is despite considerably lower demand in 2020 which had a negative effect on the margins of many other suppliers.

For the sixth year running Bosch is top of the list of the 100 largest automotive suppliers worldwide. The places immediately below Bosch, down to 9th place, go to the same companies as in the previous year. Weichai Power secures 10th place as the first Chinese company in the Top 10, dislodging Valeo (consistently at 10th or 11th place since 2017). This Chinese motor specialist is already well-known as one of the rare sales winners in 2020 and was only at 27th place when the Top 10 list was first published in 2011. Some companies did better than others in the crisis year, and this is largely dependent on geographical location. Suppliers based in Asia and/or with customers in Asia were able to profit from the ability of these countries to regain an attractive economy relatively early. Denso sends Continental down to third place and secures the 2020 silver medal. Magna slides from place four to place five, while ZF profits mainly from the acquisition of Wabco. Also, competitors Michelin and Bridgestone swop positions and now occupy places 8 and 9.

In the past year the effects of the Coronavirus pandemic converged with strong growth in the electromobility sector. Automotive suppliers had falls in sales and production stops to contend with and the majority could not avoid making job cuts. Battery and semiconductor manufacturers remain on a growth path, and so manufacturers such as CATL are increasingly looking for new staff. But European OEMs are dependent on Asian manufacturers such as CATL, Panasonic, BYD or LG Chem. In order to counteract this dependency, Germany will be developed into a European battery centre in the coming years. Various corporations are already working with battery specialists, both on the OEM side and on the supplier side, and throughout Europe Germany is scheduling by far the most projects in the battery manufacturing sector. By 2030 up to 100,000 new jobs will be created in Germany for this sector. German automotive suppliers such as Dräxlmaier, Webasto or Elring, which are already suppliers of battery technology, can also benefit from this.

Suppliers are increasingly adapting their strategies under the keywords electromobility and future technologies. LG is leaving the smartphone business and planning to concentrate on the growth area of components for electro vehicles, networked devices and artificial intelligence. BorgWarner would like to base their growth on acquisitions and at the same time develop more in the electro sector. Infineon’s strategy is to strengthen their core business with semiconductors and the exploitation of new growth markets, and this is what led to the above-mentioned acquisition of Cypress.

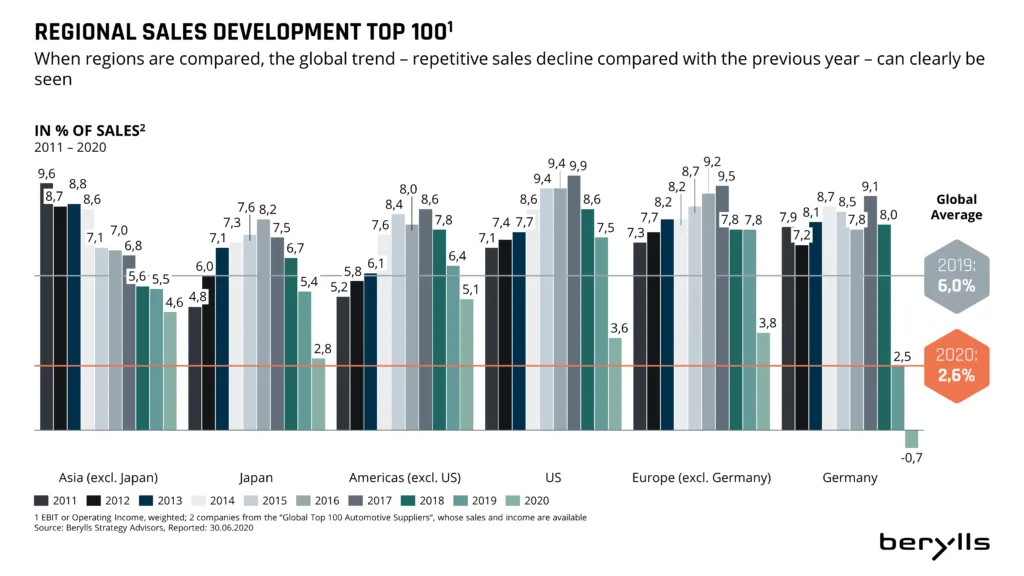

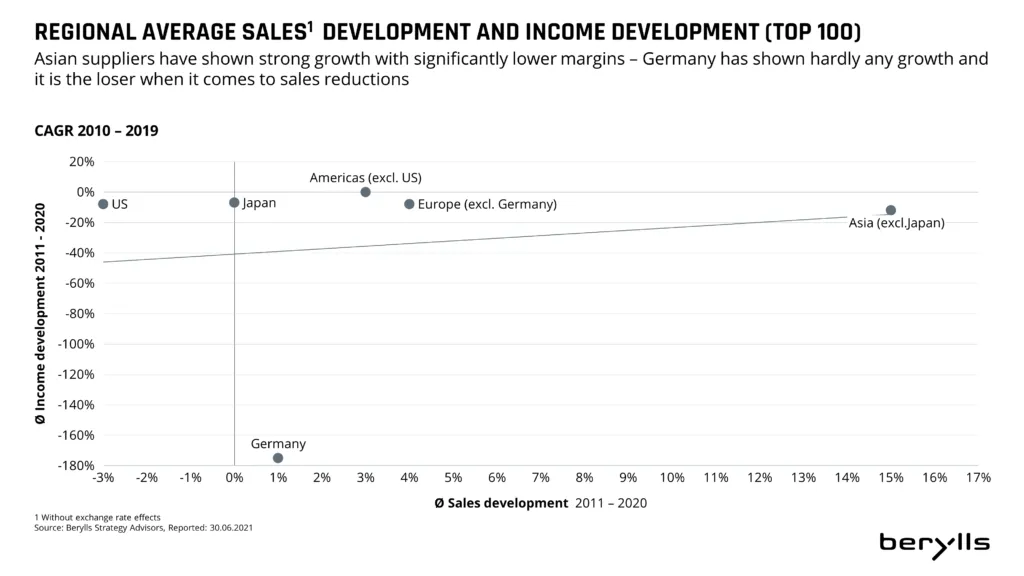

Berylls has been observing the Top 100 worldwide automotive suppliers for ten years. During this time there has been much movement and change both on the markets and on the shop floor. Back in 2011 the industry was on an upswing after the global financial crisis. After that, sales rose year on year, from 2011 onwards (663 billion euros) until 2019 (914 billion euros), by 38 per cent altogether which is a yearly average of 4.1 per cent. And the profitability of the 100 largest suppliers improved every year until 2017, standing at consistently over 7 per cent from 2012 until 2018. In 2020 the total sales of the Top 100 stood at around 800 billion euros – about 20 per cent above the level ten years ago. Profitability, on the other hand, stands at an all-time low of only around 3 per cent – although in 2020 this was largely determined by the pandemic. In 2019, the year before the pandemic, the margin still stood at 6 per cent, a comparable level to 2011 (6.7 per cent). So what has been going on these past ten years?

The geographic distribution of the large suppliers changed in the course of time. There were marked relocations of suppliers from Germany, Japan and the US to Asia. Asian suppliers (apart from Japan) have been forfeiting profitability since 2011 due to their huge sales growth, but have increasingly appeared in the Top 100.

Nine times as many Chinese suppliers made it into the Top 100 in 2020 as in 2011. At that time only Weichai Power was on the list, at 25th place; for 2020 they are ranked 10th, and they now have eight other Chinese companies spread out over the whole of the Top 100 behind them.

The biggest sales winners since 2011 are ZF Friedrichshafen and Tenneco. Bosch took over the top position from Continental in 2015 and has successfully defended this position every year since then. Continental held the top position from 2011 until 2014, slightly ahead of Bosch every year. The Top 100 companies recorded four completely loss-free years between 2013 and 2016.

The best progress within the Top 100 was made by Dräxlmaier (+ 31 places), Grupo Antolin (+ 25 places), and NGK Spark Plug (+ 21 places). The companies who lost the most places were TS Tech (- 41 places), Pirelli (- 31 places) and Meritor (-28 places, after splitting up).

Some companies were seen to come and go during the last decade. Concerns such as Johnson Controls and Honeywell split off their automotive sectors. The suppliers TRW, Delphi Technologies, Calsonic, Behr and Wabco were taken over. Yet more were not able to keep up with the continual sales increases exhibited by the other Top 100 participants and were removed because they were too small, for example IAC, Rheinmetall Automotive and Cooper Standard. The splitting off of parts of companies has also led to new additions over the years. So current occupants of the Top 100 such as Aptiv, Adient, Clarios or Garret Motion have been there for a few years now in the course of their independence. Some suppliers have made it onto the top performers‘ list under their own steam because of strong growth in sales, such as Flex-N-Gate, CATL, Piston Group an the German representatives Aunde, Freudenberg and Infineon.

The coming 10 years will see more marked upheaval. Suppliers with a high proportion of combustion engines like Mahle, BorgWarner, Tenneco or Eberspächer will be pushed to the bottom if they do not take countermeasures. Electric/electronic concerns with strong software skills, like Continental, Bosch or Hella, will grow disproportionately. The Asian concerns, especially the Chinese supplier companies such as the players from IT and entertainment electronics, Huawei, Samsung and LG, will continue to gain importance through acquisitions (also) from traditional companies. The emphasis will shift more strongly in the direction of Asia. However, German suppliers are well equipped to master the next phase of the transformation.

Berylls Strategy Advisors would be happy to support you in this key decision process.

Arthur Kipferler complements the expertise of the Berylls partner team in the fields of market & customer, technologies, sales, and digitalization, as well as in the development and implementation of corporate, product, and regional strategies.

eutschland war einmal Vorreiter bei der Brennstoffzelle. Doch neue Impulse, um die Technologie in der Breite zu etablieren, kommen aktuell überwiegend aus Asien.

Während sich Deutschland darauf festlegt, die Brennstoffzelle vor allem im Fern- und Güterverkehr zu fördern, planen China, Japan und Korea massive Investitionen auch bei PKW.

Anders als in Deutschland hat man dort erkannt, dass der PKW zwar nicht die Anwendung der ersten Stunde, sehr wohl aber der zukünftige Volumenträger der Brennstoffzelltechnologie sein wird.

China leitet sogar den größten Teil der vorhandenen Mittel für sogenannte New Energy Vehicles (NEV) auf FCEVs um – die bessere Skalierbarkeit der Ladeinfrastruktur von Brennstoffzellen ist dabei in Chinas Megacitys der entscheidende Faktor.

Ein weltweiter Absatz von über einer Million FCEVs im Jahr 2030 ist absolut realistisch. China allein hat sich für das Jahr 2030 dieses Ziel gesetzt; Toyota und Hyundai planen bis dorthin ebenfalls jeweils 500.000 FCEVs zu produzieren.

Damit droht Deutschland ein weiteres Mal bei einer zu großen Teilen in Deutschland mitentwickelten Technologie den Anschluss zu verlieren.

Einst galt Deutschland als Vorreiter beim Thema Wasserstoff. Die Bundesregierung versucht – auch mit Mitteln des kürzlich verabschiedeten Konjunkturpakets zur Eindämmung der wirtschaftlichen Folgen der Corona-Pandemie – inzwischen verlorenes Territorium wiedergutzumachen. Sie verfolgt dabei die Strategie, die Brennstoffzelle vor allem im Fern- und Güterverkehr zu fördern, nicht jedoch bei PKW.

Mit Blick auf den Absatz von FCEVs (Fuel Cell Electric Vehicles) scheint die Bundesregierung mit dieser Strategie richtig zu liegen. Im Jahr 2019 waren lediglich drei Modelle verfügbar, von denen weltweit insgesamt nur knapp 7.000 FCEVs verkauft wurden. Mittelfristig werden kaum neue Modelle hinzukommen. Die meisten deutschen OEMs haben FCEVs entweder ganz aufgegeben oder planen höchstens ein Derivat in Kleinserie einzuführen. Aus Hersteller-Sicht konkurrieren FCEVs nämlich nicht nur mit BEVs, sondern auch mit Plug-in-Hybriden und sogar 48V-Systemen um immer knapper werdende Entwicklungsbudgets. Die Herausforderung, die ohnehin schon schwierige Symbiose von konventionellen und alternativen Antriebssträngen zusätzlich um FCEVs zu ergänzen, ist den meisten OEMs schlicht zu teuer. Zuletzt verkündete daher auch Mercedes, dass der erst 2019 eingeführte GLC F-Cell wohl ohne Nachfolger bleiben wird.

Neue Impulse, die Brennstoffzelle in der Breite zu etablieren, kommen vor allem aus Asien. So planen Toyota und Hyundai bis 2030 jährlich 500.000 FCEVs allein für den Einsatz in PKW zu produzieren. Erst kürzlich meldete Toyota zudem die Gründung eines Joint-Ventures mit vier in China lokal ansässigen OEMs zur Herstellung von Brennstoffzellen für Nutzfahrzeuge.

Die Brennstoffzelltechnologie ist vielfach erprobt und insbesondere im Nutzfahrzeugbereich schon gut etabliert. Nach Angaben des US-Energieministeriums sind allein in den USA etwa 20.000 wasserstoffbetriebene Gabelstapler im Einsatz. Der zum US-Konzern PACCAR gehörende Nutzfahrzeughersteller Kenworth nutzt in wechselnder Kooperation mit dem kanadischen Brennstoffzellenhersteller Ballard und Toyota bereits Testflotten kommerziell. In der Schweiz plant die private Initiative H2 Mobilität bis zum Jahr 2025 rund 1.600 mit Brennstoffzellen ausgerüstete LKW in Betrieb zu nehmen. Und das mit über US $ 700 Millionen finanzierte US-Amerikanische Startup Nikola sieht für das Jahr 2021 die Markteinführungen von Brennstoffzellen betriebenen LKW für den Fernverkehr vor.

Der Schweizer Initiative H2 Mobilität gehören neben dem Einzelhändler Coop auch Tankstellenbetreiber und Logistikunternehmen an. Das Konsortium bündelt somit alle nötigen Kompetenzen von der Erzeugung und Betankung bis zum Betreiben der LKW. In Los Angeles liefert Toyota neben den Brennstoffzellen für den Antrieb zudem stationäre Systeme. Diese Bündelung erlaubt eine gesamtwirtschaftliche positive Bilanz, in der sich der Anwendungsfall als Ganzes mittelfristig ohne Subventionen trägt. Ein solcher Ansatz ist überall da übertragbar, wo sich Regelverkehre ergeben. Aber selbst im logistischen Fernverkehr fahren inzwischen viele LKWs entlang fixer Routen – z.B. auch die sogenannten Milkruns, welche die Teileversorgung der OEMs sicherstellen. Vor kurzem haben Hyundai und der amerikanische LKW-Motorenhersteller Cummins ein Abkommen geschlossen, um gemeinsam Brennstoffzellantriebe zu entwickeln. Hyundai will dabei sein Wissen um die Brennstoffzellen einbringen, Cummins das Know-how rund um den Antriebsstrang. Zunächst wird der Fokus auf den nordamerikanischen Automarkt gelegt und beide Partner werden die Brennstoffzellen nicht nur für den Einsatz in Autos entwickeln, sondern auch für stationäre Systeme, etwa für Notstromversorgungen.

Voraussichtlich werden nur wenige OEMs in eine eigene FCEV-Technologie investieren. Der Großteil der Antriebseinheiten wird von spezialisierten Herstellern ganzer Brennstoffzellensysteme kommen. Im LKW-Bereich ist es heute schon üblich, dass OEMs auf eine Mischung aus Eigenentwicklungen und zugekauften Antriebssystemen setzen. Dies ermöglicht eine Volumenbündelung auf nur wenige Systeme bei entsprechend geringeren Entwicklungskosten für den einzelnen Abnehmer. Hersteller wie Ballard, SHPT, Doosan oder Bosch schaffen auf diese Weise branchenübergreifende Skalen und kombinieren Kompetenzen und Technologien über ein breites Spektrum von Anwendungen. Selbst Toyota und Hyundai legen ihre Systeme so aus, dass sie in PKW und LKW gleichermaßen zum Einsatz kommen können.

Auch das von Kenworth verwendete System besteht aus zwei Einheiten des Mirai-Systems. Und das nicht ohne Grund, denn China, Korea und Japan streben langfristig klar den Einsatz von Brennstoffzellen im PKW an.

Derzeit gibt es global nicht mehr als 400 Wasserstoff-Tankstellen. Japan verfügt mit 100 Stationen über das weltweit größte Netzwerk an H2-Zapfsäulen. Es folgen Deutschland mit 90 und der US-amerikanische Bundesstaat Kalifornien mit etwa 50 Stationen; in Korea und China sind es derzeit nur ca. 20 an der Zahl. Korea, Japan und China planen bis zum Jahr 2030 jeweils rund 1.000 H2-Tankstellen in Betrieb zu nehmen. China will dafür sogar den größten Teil der vorhandenen Mittel für sogenannte New Energy Vehicles (NEV) auf FCEVs umleiten und so bis zum Jahr 2030 rund 1 Million FCEVs auf die Straße bringen. Ausschlaggebend für das Umdenken in China ist dabei die bessere Skalierbarkeit der H2-Ladeinfrastruktur.

China, Japan und Korea eint der Versuch, durch eine enge Verzahnung von Unternehmen und öffentlicher Hand, die Brennstoffzellentechnologie auf eine breite industrielle Basis zu stellen. Anders als in Deutschland liegt der Schwerpunkt in allen drei Ländern jedoch auf dem PKW als zukünftigem Volumenträger. Hier zeigt sich deren Erfahrung im Zuge der Entwicklung von Lithium-Ionen-Batterien: Um die Auslastung von zeitweise leer stehenden Zellfabriken zu erhöhen, wurde lange Zeit der Einsatz von Lithium-Ionen-Batterien in stationären Anwendungen forciert – der Durchbruch kam jedoch erst mit dem Großserieneinsatz im PKW.

Der von Deutschland eingeschlagene Weg, Brennstoffzellen in erster Linie für LKW, Schiff- und Luftfahrt zu nutzen, greift langfristig zu kurz. Länder wie China, Korea und Japan haben erkannt, dass der PKW zwar nicht die Anwendung der ersten Stunde, sehr wohl aber der zukünftige Volumenträger der Brennstoffzelltechnologie sein und ihr so zum Durchbruch verhelfen wird.

Ein Volumen von einer Million FCEVs im Jahr 2030 ist leicht möglich. Das entspräche einem weltweiten Marktanteil von nur einem Prozent – und genau dem Wert, den sich China als Ziel gesetzt hat. Toyota und Hyundai planen ebenfalls ihre Fertigungskapazitäten bis 2030 auf jeweils 500.000 Stück auszubauen. Zum Vergleich: Um eine ähnlich große Zahl an FCEVs in LKWs auf die Straße zu bringen, müssten fast ein Drittel aller weltweit verkauften LKW auf Brennstoffzellen umgerüstet werden.

Die von den deutschen OEMs und der Bundesregierung verfolgte Strategie birgt somit die Gefahr, dass Deutschland zwar viel in die weitere Industrialisierung der Brennstoffzelle investiert, aber am entstehenden Massenmarkt nur ungenügend partizipiert. Konsequent wäre das Vorgehen der Bundesregierung nur, wenn – anstatt auf FCEV zu setzen – neben den BEVs auch E-Fuels gefördert würden.

Die Strategie, abzuwarten, bis eine gestiegene (oder künstlich herbeigeführte) Nachfrage die Produktion von Brennstoffzellenfahrzeugen in Großserie zulässt, wird nicht aufgehen. Es muss vorher gehandelt werden.

Als Gewinner der Brennstoffzellen-Technologie werden solche OEMs hervorgehen, die es schaffen, ihre Technologie über eine Vielzahl verschiedener, auch nicht-automobiler Anwendungen zu skalieren.

Dazu werden diese sich selbst als Unternehmer und Partner in Kooperationen einbringen müssen. Denn als OEM sind sie nur dann interessant, wenn sie potenziellen Käufern ganzheitliche Lösungen anbieten können, die neben dem Fahrzeug auch das Betanken und sogar die Erzeugung von Wasserstoff beinhalten.

Zulieferer sollten nicht auf die OEMs warten, sondern direkte Kontakte zur neuen Riege von Systemherstellern knüpfen.

Da diese in der Mehrzahl in Asien sitzen, sollte auch die Brennstoffzellstrategie unmittelbar aus den Standorten vor Ort getrieben werden.

Gleichzeitig darf der Einsatz im PKW nicht aus dem Auge verloren werden. Das betrifft sowohl die technische Auslegung neuer Systeme als auch die genaue Beobachtung der Märkte – insbesondere in Asien.

Andreas Radics

Andreas Radics (1973) ist seit 2001 als Strategieberater in der Automobilindustrie tätig und blickt darüber hinaus auf mehr als vier Jahre Berufs- und Führungserfahrung in der Industrie zurück. Bevor er als Gründungspartner 2011 Berylls ins Leben rief und aufbaute, war er bei den international agierenden Strategieberatungen Gemini Consulting und Oliver Wyman tätig.

Er zählt zu den führenden Köpfen für Mergers & Acquisitions sowie für die Entwicklung und Umsetzung von Unternehmensstrategien in der Automobilindustrie, ist Experte für eMobility und ausgewiesener Kenner des US-Marktes.

Studium der Betriebswirtschaftslehre an der Katholischen Universität Eichstätt, Wirtschaftswissenschaftliche Fakultät Ingolstadt.

igns of a storm brewing - As it was, at the end of 2020, the year 2021 was not looking very promising. Despite a fundamentally positive outlook for the motoring industry, the uncertainties of 2018 and 2019 looked set to continue. Structural change, as well as consumer reticence and vehicle sales stagnation were harbingers of the end of a decade of strong growth.

The year 2019 also showed us that structural change would not proceed quickly – more likely step by step. The merger of Magneti Marelli and Calsonic; Continental’s founding of the company spin-off Vitesco; Tenneco’s takeover of Federal Mogul – all were signs of persistent, continual change for the car industry and its suppliers.

The German M&A market had hardly cooled off at all in 2019, with 293 transactions compared to 295 the previous year. But banks were already viewing credit payments to the car industry with concern, because of the difficult market setting. Despite cheap money and zero-interest policies, an icy wind was blowing around the financing of classical car manufacturers.

New technologies remained risky because of the uncertain market and legal position, as well as the halting monetization and sustainability of business models being trialed. At the same time, the traditional car business seemed to have an ever-closer expiry date. After a long period of growth, pressure for change grew strongly, and there was a push for appropriate investments and strategy changes in the supplier industry.

It took a little while for OEMs and suppliers to accept that they could only reach their targets in CASE technologies through collaboration, because the investments were too enormous for them to be able to manage on their own. But at the same time, political and social problems were destabilizing the market, and rapid change and monetization of new technologies – for example, connectivity services and cybersecurity – failed to emerge.

If we look at profit development in the last few years (-1.5 percent in 2019 compared to 2018, for the biggest 100 suppliers), we can see that there were numerous companies in the lower third of the supply industry which had slipped into the loss zone even before the Covid-19 crisis began in 2020. This alone would be manageable in the short term, but with structural change, the question arises as to whether or not many business models will be sustainable in the future. If old business is wobbling and new business is not yet firmly established, tensions arise and all participants need great skill and dexterity to adopt a clear plan out of the crisis and avoid insolvency.

If we look at the history of how insolvencies develop in the car industry in German-speaking countries, the number since 2010 has involved around 20 (±10) companies a year. However, the global financial crisis of 2008/09 demonstrates that this number can rise sharply in an economic crisis: there were over 80 insolvencies in 2009. Every percentage point of negative development in gross domestic product (GDP) leads to a proliferation in the number of insolvencies. In 2009, the GDPs of major automobile markets fell by between 2 percent and 6 percent (for example, in Germany, Japan, Great Britain and the US), whereas China showed strong growth of around 9 percent.

When it came to vehicle sales in 2009, Great Britain were particularly badly affected, with declines of between 10 percent and 20 percent. Thanks to an environmental bonus, Germany was able to generate a sales surplus of around 20 percent in 2009 compared with 2008, and in this way fended off a deep crisis. However, sales volumes decreased significantly in 2010, to significantly below the pre-crisis level (down 6 percent compared with 2008) and it was not until 2011 that they reached comparable levels again. All these figures are intended to give an idea of the future direction of sales after the Covid-19 economic crisis.

The current situation shows a similar picture for GDP forecasts as for sales. In April the IMF forecast declines of 6 percent for the US, 7 percent for Germany, Great Britain and France, 5 percent for Japan and a rise of 1.2 percent for China. If we line up the numerous crystal balls showing sales forecasts for 2020 and hazard a glimpse into an uncertain future, we will see a corridor reaching from declines of 20 percent to 25 percent for the global car market. There are pessimistic scenarios which paint an even more dismal picture.

Despite support measures for the DACH region – D (Germany), A (Austria) and CH (Switzerland) – Berylls is forecasting a sixfold increase in average insolvency figures for the period March 2020 to mid-2021. Altogether this will probably result in around 120 automobile companies sliding into insolvency. According to Berylls’ forecasts, up to 100,000 jobs will be affected.

Given that the automobile world was a very different one in 2009, after 2020 it will be more difficult to realize a similar story of successful recovery. On the contrary, Covid-19 could accelerate structural change in the German-speaking/European supply industry and even drive insolvencies above 120. The structural damage caused by this insolvency tsunami would be more significant, and the development of new structures would take considerably longer, prolonging the recovery phase. It is also unclear to what extent the banks are prepared to pay out money for the development of new motoring areas after the painful reduction of credit to car suppliers.

The same applies when we look at private equity companies, which can currently find better opportunities for ambitious returns in other industries. Rescue by investors and M&A activities looks difficult; on the one hand, sales prices have risen too high in the last few years while on the other, many financial investors are anxious either not to advance into sectors which they will not be able to sell later, or be unable to handle high expectations of returns. Strategists will proceed very carefully, for the moment preferring to keep hold of their money and wait for better times to make strategic acquisitions.

For takeovers out of insolvency there will be strategists who will have had wish lists for a potential expansion of their own portfolio for quite some time. So the following years could bring further insolvencies, perhaps above the 20 per year mark, and accelerate consolidation. In terms of sales, currently around €12 billion are in play, which come from suppliers who have got into difficulties this year and become insolvent. Reliable forecasts for the actual extent of this will not be calculated until the third and fourth quarter, by which time the number of notable insolvencies can be better quantified and described. We already have some notable examples: Veritas, DGH Druckguss Heidenau and Finoba.

One of the lessons from 2009 should be to avoid a downward spiral of continual pessimistic forecasts. It was such a spiral that tore through the car industry and led to the situation in 2009 in which significantly fewer vehicles were being produced globally than were required on the market. Whereas global demand only reduced by almost three million vehicles, almost nine million fewer were produced than in the previous year. A lack of communication and transparency over highly complicated supply chains made planning more difficult for all concerned, and it was existing vehicles which finally had to fill the trade gap.

If the industry does not manage to make a better job of orchestrating the ramp-up this time, and if participants do not read market opportunities properly, more damage could be done than in 2009. We must avoid a situation where capital is gained from the financial stress suffered by normally solid companies. In the medium term this would be alleviated if transformation was actually abandoned altogether. This is the reason why people are increasingly calling for structures to be created in which companies in trouble can find a safe harbor (e.g. takeovers using a fund created by banks, investors or unions). However, OEMs have an interest in keeping their highly complex supply chains stable and carrying out the supplier transformation in coordinated channels. It is not known whether “problem companies” might also land in this safe harbor – companies which would have been better wound up – otherwise the pace of this wise change in the industry will be slowed down.

The market will be reassessed, and it must be steered with measured judgement and supported at the right point. Alongside investments for CASE, other investments are needed to rebuild the supply chain, ranked in a similar way. The top priority at the moment is to secure liquidity, especially as many car suppliers in the supply chain are system-relevant. This alone is a mammoth task for the industry, and it is not enough on its own. New ideas are needed, for example the transparency mentioned earlier, to steer the ramp-up on the basis of demand.

In addition to all this, a mixture of purchase incentives to support the industry, including sustainability and environmental demands, needs to be provided through hybrids, battery electric vehicles (BEVs) or fuel cell electric vehicles (FCEVs). However, structural problems should not be concealed, and short-term purchase incentives should not again lead to medium-term over-capacity and an incorrect vehicle portfolio that runs contrary to long-term climate goals.

When it comes to rescue funds for suppliers, we should proceed with clear criteria for system relevance, continuation of structural change and a clear central control body, compatible with the market reassessment of “zombie firms.”

The setting of these parameters will define whether or not we will see an even higher number of insolvencies. There should be opportunities for all participants (including suppliers, banks, private equity firms, OEMs and politicians) to continue the change which has been set in motion, to transform the car industry. Powerful waves seem unavoidable, but they must be prevented from getting bigger and forming a tsunami.

Dr. Jan Dannenberg (1962) has been a consultant for the automotive industry since 1990 and became a founding partner of Berylls Strategy Advisors in May 2011. Until spring 2011, he worked with Mercer Management Consulting and Oliver Wyman in Munich, Germany, on international projects – for five years as Associate Partner, and another three years as Partner. He is a recognized specialist in innovation and brand management in the automotive industry, and primarily advises suppliers and investors on strategy, M&A and performance improvement. In addition he is Managing Director at Berylls Equity Partners, an investment company that specializes on mobility enterprises.

Bachelor of Arts in economics at Stanford University, USA; business administration and doctorate degree at the University of Bamberg, Germany.

ovid-19: A unique situation - Never before has a global crisis hit the automobile industry with such speed and impact.

Within just a few weeks, large areas of car production had come to a standstill, with serious results: break-up of supply chains, announcement of short-time working, temporary factory closures and laying-off of temporary staff. Rapid expenditure control coupled with protection for employees’ health were the first steps taken by every supplier. Now, after three months’ experience of the coronavirus crisis, factories can start up again and companies face the challenge of finding the right way to carry out the ramp-up and forecast demand.

It is obvious to nearly every supplier that coronavirus will mark a turning point for their company. Even before the pandemic lockdown, firms were having to put the brakes on spending. The OEMs’ wave of cost savings, for example Daimler with €1.5 billion (November 2019), BMW with €12 billion up to the year 2022 (March 2020) by means of “Performance Next”, and the VW brand with €15 billion in savings planned up to the year 2023 (March 2019), were combined with demands that suppliers reduce their prices again.

In the current climate, familiar measures are being taken, such as adaptation of capacity in the manufacturing process, selective redundancies, optimization of working capital, and easing of terms with outside creditors. The hope is that there will be a rapid and marked recovery. There is nothing wrong with this per se, and in the past these restructuring projects and slim, efficiency-oriented business models have guaranteed companies’ survival and success again and again. But the risks are priced in, and they will rise significantly after the immediate Covid-19 crisis passes.

CASE investments must continue to be made, in order to keep up with the transformation of the supplier industry – the amortization of these expenses is being delayed and that makes the position even more insecure. The future development of the automobile industry, especially with regard to production runs and vehicle classes, segments and power units, is unpredictable. The catchword for this is VUCA: Volatility, Uncertainty, Complexity, Ambiguity. Safeguarding of the supply chain for JIT/JIS delivery is hardly possible while some factories might be suddenly standing empty and others do not manage the ramp-up or restart their output.

The result is that an operations and performance crisis can rapidly turn into a financial and liquidity crisis. Then shareholders, creditors and banks will expect more than the usual improvements. In any case these will be nowhere near enough, because adaptations and restructuring requirements will be more substantial, more fundamental and more profound in the coming two years than they have been in the last 30. Every car supplier must be prepared to accept significant restructuring measures.

The right ingredients for success in an intelligent restructuring are decisive. First, there needs to be process reliability: the restructuring must be carried out in a sustainable and pragmatic way. Above all it is crucial to find a holistic solution which coordinates all the control levers and quickly identifies and reacts to the causes of the crisis.

Secondly, restructuring expertise is needed: alongside the company’s own internal team it is essential to have access to external restructuring expertise. Experience, knowledge and networking skills among all company roles are essentials too. Moreover, if the restructurer can keep a certain emotional distance this can save the company culture from damage.

Thirdly, automobile know-how is important: as well as knowing about the car industry, it is important to know how to make improvements. Benchmarks from the sector’s best players in matters of costs, earning power, financial structure and so on, help to quickly identify the right savings opportunities or structures. Finally, there needs to be stakeholder insight: anything which is important for a bank should never be unimportant to the OEM. And it is precisely when there is a crisis that the car supplier must be fair to everyone.

Berylls has identified nearly 30 control levers from six categories which need to be investigated in the context of intelligent restructuring programs – and used if there are any problems – in order to tackle the company crisis quickly and specifically, and solve it. It is not enough to simply reduce costs. Every company crisis is unique. Whereas for one supplier it might be mainly the financial and debt structure that is problematic, for another it could be the situation with the client that is the main cause.

On the one hand, identification of the cause of the crisis should be carried out alongside the dimensions of strategy, governance, operations, overheads, financing and transparency. On the other hand, crisis management should guarantee that a coordinated and holistic solution works for each individual control lever. Liquidity crises must be handled with a different dynamic, and often in a more pragmatic way, than a strategy crisis. This requires not only substantial experience in the process of crisis management and restructuring, but also sound knowledge about which solutions are sustainable specifically for the car industry. Anyone tackling restructuring in this intelligent, holistic way will emerge from the crisis in a stronger position.

Dr. Jan Dannenberg (1962) has been a consultant for the automotive industry since 1990 and became a founding partner of Berylls Strategy Advisors in May 2011. Until spring 2011, he worked with Mercer Management Consulting and Oliver Wyman in Munich, Germany, on international projects – for five years as Associate Partner, and another three years as Partner. He is a recognized specialist in innovation and brand management in the automotive industry, and primarily advises suppliers and investors on strategy, M&A and performance improvement. In addition he is Managing Director at Berylls Equity Partners, an investment company that specializes on mobility enterprises.

Bachelor of Arts in economics at Stanford University, USA; business administration and doctorate degree at the University of Bamberg, Germany.

he impact that digitalization has already had on the car industry can be measured in one figure: €119 billion. That is the amount which has flowed into start-ups in the form of risk capital and other financial resources so far, according to a recent Berylls survey, How mobility start-ups are transforming the global automotive industry. Some 1,003 start-up companies were investigated, with some amazing results.

We are already seeing the effects of new digital business models on the roads. In the US and to some extent in China, the major car service agencies, or “ride hailing” companies, have changed mobility behavior. In many cities there is no longer a taxi service to the airport, for example.

Mobility service providers are systematically expanding their networks nationally and internationally. Of the 10 start-ups which have attracted the most investment, six are ride hailing services: DiDi (China), Uber (US), Grab (Singapore), Ola (India), Lyft (USA), and Ucar (China). As one example, in the seven years since it was founded, Lyft has expanded to cover 95 percent of the US population. Its services are available in 700 towns and cities, and with a stock market value of $15.6 billion and turnover of $2.16 billion, Lyft is only one of the successes of digitalization. The other companies in the Top 10 (Tesla, NIO, Faraday Future, and Cruise) are focusing on the production of electric vehicles and/or autonomous driving. Altogether, the 10 biggest start-ups have raised 49 percent of the total risk capital.

The focus segments for mobility start-ups are currently: ride hailing (with €44.1 billion in risk capital); vehicle construction, especially electric cars and self-driving cars (€28.4 billion); shared mobility services, such as SHARE NOW (€15.8 billion); electric and electronic components (€11.6 billion); connectivity solutions for vehicles (€1.8 billion); used vehicle sales (€1.6 billion); payment systems (€1.5 billion); “last mile” freight traffic (€1.5 billion); digital infrastructure connectivity (€1.1 billion); and Industry 4.0 applications for the car industry (€1 billion).

The three leading segments are attracting 75 percent of investment resources and the 10 major ones cover more than 90 percent. Berylls investigated more than 150 sectors along the car supply chain in the course of our research, which identified enormous potential for further start-ups in emerging sectors.

We expect substantial new investor demand in start-up segments including: cloud services and cyber security; sensors and sensor system integration in connection with autonomous driving (lidar, radar etc.); physical and digital infrastructure for driving electric vehicles; new human machine interface (HMI) systems such as augmented reality; speech and gesture recognition; connectivity services for the vehicle (such as remote diagnosis and remote steering); and vehicle subscriptions. These areas and others are under-represented when it comes to entrepreneurship and risk capital, and in future we expect many different opportunities to arise for start-up companies.

From the point of view of the German car industry, an increasing readiness in German-speaking countries to establish or support new digital business models with risk capital is a welcome development. Over the past three years, more than 30 start-ups have been established in the DACH region (D – Germany, A – Austria, CH – Switzerland), offering innovative mobility solutions.

Although Berlin and Munich have nowhere near the status of Silicon Valley or Tel Aviv in the tech industry, more and more new automobility companies are starting up in Germany. Financing is more readily available: all German car manufacturers as well as major suppliers (such as Bosch, ZF, Continental and Mahle) have recognized that they can gain access to technological innovation by investing risk capital. Other large DAX-listed companies including Allianz and Siemens are also investing in mobility start-ups. If Daimler was the most active investor in start-ups in 2017, in 2018 it was BMW. The BMW Group and BMW iVenture have been happy to spend a lot of money on their participation and takeovers of Parkmobile, DriveNow, Moovit, Fair.com, May Mobility, Caroobi, Lunewave, Critical TechWorks and Graphcore. Their financial contributions have exceeded €300 million.

The hype about more “unicorns” (privately owned start-up companies valued at $1 billion or more) to come is by no means over, and the example of AUTO1.com in 2018 shows that the next ones could come from Germany. AUTO1.com is a Europe-wide online marketplace with its own stock of vehicles, which has been concentrating on commercial car wholesalers. The group also runs the internet platform “Wir kaufen ein Auto” [“We’re buying a car”] for private vehicle sales. SoftBank, the highly active Japanese investor, has paid €460 million for a 20 percent share in AUTO1.com. This values the company at €2.3 billion, making the Berlin start-up a genuine unicorn.

Dr. Jan Dannenberg

here is a rift tearing through the car supplier landscape, and it is getting wider and wider: large enterprises versus medium-sized businesses, internal combustion engine champions versus CASE (connected, autonomous, shared and electric vehicles) converts, Triad countries versus China, established companies versus start-ups. The dynamic force driving forward the transformation of numerous companies, and indeed the whole industry, is breathtaking.

Bosch has sold its turbocharger (BMTS, 2017) and starter-generator (SEG Automotives, 2018) businesses. Honeywell spun off its turbocharger unit, Garrett Motion, in 2018. GKN, which was sold to the financial investor Melrose, also in 2018, is separating off single units step by step (for example Powder Metallurgy, 2019). Delphi has been divided up into two companies, Aptiv (automobile electronics and advanced safety technology) and Delphi Technologies (electric vehicles and combustion engines). Continental is planning the spin-off and sale of its powertrain division for mid-2019. FCA has pulled out of the supplier business completely with the sale of Magneti Marelli to Calsonic Kansei (2019).

Since the sale of Federal Mogul to Tenneco, the company has been divided into two units: aftermarket/ride performance and powertrain technology. After the sale of its internal division (Yangfeng Automotive Solutions, 2015) and the spin-off of Adient (2016), Johnson Controls has now sold its last automobile segment, Power Solutions (2018). Nearly every 10th supplier from the Top 100 (based on sales) has gone through a dramatic change in the last two years. What lies behind these carve-outs, spin-offs, divisions and IPOs?

The so-called “tipping point,” from where there will be no more growth in the production of components for combustion engines, is getting nearer. The peak will be reached between 2023 and 2025. At the moment, the large car industry suppliers can still exit their combustion engine and transmission businesses and get a solid price for them. Prices being obtained currently stand at an EBIT multiple of 5 to 6 (for comparison, car suppliers without combustion engine business stand at an EBIT multiple of 10 to 12, so twice as high).

This separation from the combustion engine business is almost comparable with the spin-off of “bad banks” carried out after the financial crisis: “toxic” business areas are removed and so can no longer damage the remaining part of the company. If complete withdrawal from internal combustion engines (ICEs) is actually to take place by 2050, as announced by many national governments, Conti, Bosch, Magneti Marelli and co could be gradually leaving this risk-laden business behind them. However, if ICEs continue to play a part in the more distant future, an attractive investment opportunity could emerge. In this case, a similar rule applies for the ”last man standing” of the ICE business as for some digital business models: the winner takes it all.

The anticipated downfall of the combustion engine is being exacerbated by the total focus on CASE technologies. Traditional innovation fields for car interiors, exteriors, powertrain or chassis are disappearing from public discussion. Anything without the attributes associated with artificial intelligence, cybersecurity, Big Data, autonomous driving features or blockchain is hardly noticed. It seems that the development and survival of the car industry will only be possible with the help of digital solutions.

The following comparison shows just how big the difference between “digital” and “traditional” has grown. In the years 2017/18, the start-up WayRay, a manufacturer of holograph-enhanced reality technologies and user interfaces, was able to raise venture capital amounting to $98 million. The company currently has 50 employees and a turnover of $3.5 million. Last year the supplier Proseat (seat cushion maker, turnover of €291 million and 2,100 employees) was sold to a Japanese competitor and valued at around €45 million. Based on the sales multiple, WayRay was valued at a factor of 180 times higher than Proseat. The rift between CASE or start-ups and traditional modules or suppliers could hardly be wider.

For years now, large supplier groups have been earning higher returns than medium-sized businesses (8 percent EBIT margin in comparison with around 6 percent) and they show stronger growth. The consolidation process for the whole car supplier industry is continuing. In the Global Top 100 survey, Berylls estimates that a 60 percent share of total sales will go to the 100 largest suppliers by 2025. The share is currently just over 50 percent. The large supplier groups have a more global structure and easier access to the capital markets. They also have more competitive cost structures because they have sites in low-cost countries, and they invest large sums of money in the development of CASE technologies or buy themselves the necessary skills through company takeovers.

Medium-sized businesses, meanwhile, have their agility and entrepreneurship, their specialization in niche areas and their cost awareness to enable them to hold their ground as suppliers.

Will the fractures running through the auto supplier industry be made more permanent in the next few years – will the differences between the two groups of companies increase? From what we know today, traditional and digital business models are moving away from each other with increasing speed. But this does not mean that traditional business models are heading for immediate disaster; rather that new opportunities are presenting themselves for the remaining market participants in traditional areas.

On the one hand this is because the number of competitors is reducing through market exits, and the remaining cake, although smaller, will be shared between fewer people. On the other hand it is due to continuing high numbers of combustion engines being made in the medium and long term: those condemned to death might live longer than expected after all.

Dr. Jan Dannenberg (1962) has been a consultant for the automotive industry since 1990 and became a founding partner of Berylls Strategy Advisors in May 2011. Until spring 2011, he worked with Mercer Management Consulting and Oliver Wyman in Munich, Germany, on international projects – for five years as Associate Partner, and another three years as Partner. He is a recognized specialist in innovation and brand management in the automotive industry, and primarily advises suppliers and investors on strategy, M&A and performance improvement. In addition he is Managing Director at Berylls Equity Partners, an investment company that specializes on mobility enterprises.

Bachelor of Arts in economics at Stanford University, USA; business administration and doctorate degree at the University of Bamberg, Germany.

10-year period of sustained growth and record results in the car supply industry has come to an end. The digital revolution, OEMs’ customer focus, and the expansion of automotive supply chains around infrastructure provision and mobility operations are all dramatically changing the economics for suppliers. Berylls has identified eight challenges to which every car supplier CEO needs to respond:

The car industry used to exercise tight discipline in its supply system, with clear structures along the whole chain, good planning reliability and solid forecasting, as well as reliable relationships. VUCA, or Volatility, Uncertainty, Complexity and Ambiguity, in today’s auto industry has resulted in massive disruption to the established supply system. VUCA forces are increasing significantly, making forecasting more difficult or even impossible. Management based on experience, stability and certainty is also made more difficult. Minor unplanned deviations can have a major impact on suppliers and lead to a chain reaction along the value creation process.

CEOs need to create an organizational and management model to reliably manage their companies against this backdrop of VUCA.

The years 2010 to 2018 were golden ones for the car supply industry, marked by sustained growth, widespread cost controls, strengthening of equity structures, solid financing and improved competitiveness. But the next five years will be very different, with disproportionally higher costs to contend with – the result of wage increases in the east, acquisitions in the west and rising prices for raw materials – alongside a reduction in productivity improvements. Financing will be more difficult, too – with higher interest rates and the car industry viewed by banks as a “crisis industry.” The period will see increased complexity in customer profiles, limitations on globalization (increasing logistics costs) and a requirement for high investment in innovation. The average EBIT margin of 8 percent for supply enterprises and 6-7 percent for medium-sized companies will shrink to around 5 percent by 2025.

CEOs need to switch to “sustained restructuring mode” to secure the operating efficiency of their highly complex value creation systems in an ever-changing world.

CASE (connected, autonomous, shared and electric) vehicle technologies are at the heart of change in mobility services. Because of their systemic interlinkages, strong functional improvement of the “mobility” product and high levels of intervention in existing solutions, their development, production and implementation are expensive and lengthy. CASE is expensive and up to now has delivered few – if any – financial improvements for companies in the car industry. This will not change in the coming decade; investments in the development of CASE technologies will run into double-figure billions. At the same time value is flowing out of the traditional profit sources, especially the internal combustion engine (ICE).

New developments by OEMs are being suspended, investments are not being made, financial resources are getting scarce. The balancing act between years of loss-making investments in CASE technologies and non-existent profits from the traditional business can no longer be managed. The losers in this development are ICE-dependent companies (which still represent 25 to 30 percent of value creation in the car industry), traditional low-tech suppliers and the typical medium-sized businesses which can no longer afford tough and risky business. On the other hand, the winners are the large enterprises (such as Bosch, Conti and ZF), car suppliers in the CASE field, new mobility start-ups and niche specialists.

CEOs need to leave behind former approaches, develop new business models to participate in the change in the car industry initiated by CASE, and at the same time tackle high numbers of fundamental innovations with long amortization times against a backdrop of faltering core businesses.

Competition in the supplier industry has always been merciless. Weak suppliers are rapidly sifted out according to the “survival of the fittest”. But this was happening within a stable economic system. The sustained and continuous development that has made the car industry and its suppliers highly innovative was based on a system in which any changes would be financed from the system itself. Innovations would be introduced into the market in small steps and skills would be built up gradually.

However, that system has now ruptured. A recent Berylls survey of 1,000 mobility start-ups shows over in the past five years, more than €180 billion has been invested in mobility venture capital. During the same period, only about half that amount was spent on investment in research and advance development for traditional automobile players.

Start-ups are looking more for disruptive innovations than revolutionary developments: a complete car from a 3D printer, cars which hover above ground, flying vehicles, zero-waste cars etc. These visionary business models coupled with absolutely “infinite” financial and intellectual resources are now clashing in a competition for the best mobility solution of the future, creating a clash of cultures with established suppliers.

CEOs need to assess two things: the risks posed to their business models by tech start-ups with disruptive approaches and the opportunities these bring from which their companies can profit.

In developed societies, the disadvantages of individual mobility are becoming more and more apparent: unsustainable use of natural resources, traffic accidents, time wasted in traffic jams and pollution (air, noise and water). The car is increasingly the scapegoat for all these problems and young people are turning away from it. Other industries and careers – and the companies associated with them – are gaining social prestige and attracting talent away from the erstwhile flagship auto industry.

CEOs need to make their companies, and indeed the whole car industry, attractive again to continue attracting the best talent.

The collaboration between OEMs and suppliers over the past 30 years has never been co-operative, marked by cost pressure, supplier-customer relations and tough competition. This is not going to change in the future. However, system-relevant players in specific areas, and in areas which are critical for OEMs, are the exception. Because of VUCA and the enormous upheaval going on in the sector, it is almost impossible for OEMs to maintain reliable and stable relationships with their suppliers. The once clear and – to a certain degree – predictable future is dissolving and reliability is declining rapidly. The result is that production start-ups are delayed, vehicle projects are suddenly cancelled, quantities are considerably less than planned, or they increase significantly, specifications are changed at the last minute, and commercial agreements are broken.

In parallel to this, completely new customer relationships are developing with tech start-ups or Asian start-up OEMs, who have little or no knowledge of the mechanisms of the car industry (and possibly do not even want to acquire any). The tectonic changes began a long time ago; Asian and in particular Chinese OEMs, combined with the Chinese automobile market – which has grown in importance because of its size – are bringing about a shift in the balance of power. China has replaced Europe, Japan or the US as the measure of all things for the car industry. Will Daimler, BMW or Audi become the Telefunken, Grundigs and DUALS of the 2020s?

CEOs need to adapt their companies to the new global balance of power when it comes to interacting with their customers.

The whole balance of power in the mobility industry is shifting to China and Asia more broadly. Every third car is produced in China. In future China will be growing twice as fast as the other core markets. In relation to future technology for e-mobility, growth and market penetration are already higher in China than in the rest of the world. There is also great willingness to invest in new OEM markets and mobility start-ups in China. Furthermore, China is buying out suppliers in hi-tech countries; takeovers of western OEMs are not excluded. State economic policy has defined the mobility industry as a key industry and is supporting its advancement. In short, China is set to become the “North Star” of key markets for OEMs. For the traditional car industry this means that they need to become more Chinese. And that goes for all aspects of their own business model.

CEOs need to bridge the gap between the build-up of skills in China and the securing of skills in the west.

The whole of the automotive value creation system is based on increasingly smooth and efficient processes: zero PPMs, JIT/JIS deliveries, simultaneous engineering, and so on. And this system has to work all over the world. Target prices for components are calculated on the basis of organizations functioning “perfectly.” The reality looks different: production start-up problems, quality costs, overtime caused by interface problems and high staff turnover in BCC countries. The majority of car suppliers have clear deficits in their business systems because, for the most part, things do NOT run perfectly.

CEOs need to establish high-performance organizations which are “best in class” at fulfilling all customer requirements, while at the same time ensuring profitability.

Our outlook in summary? The last 10 years were a piece of cake compared to the challenging agenda of the next 10.

Dr. Jan Dannenberg (1962) has been a consultant for the automotive industry since 1990 and became a founding partner of Berylls Strategy Advisors in May 2011. Until spring 2011, he worked with Mercer Management Consulting and Oliver Wyman in Munich, Germany, on international projects – for five years as Associate Partner, and another three years as Partner. He is a recognized specialist in innovation and brand management in the automotive industry, and primarily advises suppliers and investors on strategy, M&A and performance improvement. In addition he is Managing Director at Berylls Equity Partners, an investment company that specializes on mobility enterprises.

Bachelor of Arts in economics at Stanford University, USA; business administration and doctorate degree at the University of Bamberg, Germany.

ndeterred by talk of the end of the combustion engine and the possibility of autonomous taxi fleets – and with supposedly dwindling enthusiasm for cars in Europe – the worldwide 100 largest suppliers are again looking back on a successful business year. However, new competition looms and this will ensure movement, especially in the lower rankings.

To gain an overview of the 10 largest international car suppliers of the past year, it is enough to take a look at the Top 100 of 2016: there were no promotions and no demotions among the leaders in the past year. Bosch is unchallenged in first position, with €47.4 billion in turnover (company area – Mobility Solutions), followed by Continental (€44 billion) and Denso (converted to €36.4 billion).

The top three are stubbornly defending their positions and have occupied these rankings in Berylls’ list of Top 100 suppliers for the past two years. However, compared with the previous year, the distance between them and the occupant of fourth position (€2.9 billion in turnover) has grown markedly (2016: €1.7 billion). The reason for the top three’s success is the fact that globally very few cars leave the production line without any components supplied by these leading players. And this applies whether they are budget cars or luxury limousines, electric vehicles or conventionally powered models.

A glance at the broader Top 100 table reveals a divided picture: declines in sales can be identified in many places. Eight companies out of the Top 20 show negative sales developments, particularly Asian and American companies. However, it is not poor performance that is responsible for this, but particularly severe exchange-rate effects in 2017. The results of Berylls’ Top 100 are shown in euros, and all other relevant currencies lost value significantly against this over the period. The dollar was hit especially hard, and on the reference date of December 31, 2017, it lost more than 12 percent of its value against the euro. It is very unusual for all exchange rates to fall against the euro, and this was last seen in 2013.

In the current survey, the average increase in turnover among all suppliers was only 0.9 percent. In 2016 – a year when the dollar was considerably stronger – it was about 6 percent. If the exchange rate effect is removed, the supplier industry can look back on an average turnover growth of 8.6 percent – so on that basis, turnover growth strengthened in the past year.

For German suppliers in particular, things were running smoothly in 2017. There are 18 German companies in the Top 100. Knorr-Bremse (braking systems) is represented again, at number 87, after a sales increase of 16 percent. Freudenberg is among the big winners, with a jump in position from 84 to 60 after their full consolidation of the former joint venture, Vibracoustics. On average, German suppliers moved up five places in the rankings in the past year. One reason for this is the continuing innovation power of the Germans. For an example, we just need to look back at the number of patents applied for from 2010 to 2017 for technologies associated with autonomous driving. Here Bosch reigns supreme, ranked first with 958 applications, followed by Audi with 516 patents, and Continental third with 439 patents. Neither Asian nor American suppliers are ranked among the best 10 by this measure.

If we look at the other European suppliers we see a similarly positive picture, with one exception: IAC (International Automotive Components), an interior components specialist with American roots and its headquarters in Luxembourg. The company belongs to the US financial investor Wilbur Ross, and in 2017 it fell 21 places to rank at number 66. IAC had to absorb a sales collapse of 35.5 percent. Despite this, the company was able to announce the completion of a new round of financing in April 2018 and win over a new minority shareholder, Gamut Capital Management. According to its own reports, it had bottomed out at that point. GM also named IAC “Supplier of the Year” in 2017, but this was likely not much of a comfort.

The company Grupo Antolin (ranked 52) also recorded a slight sales decline, following a significant rise the previous year. The 2016 numbers were skewed by the takeover of Magna Interiors that year.

So up until now, the traditional car industry has generated good to very good sales. The so-called tipping point for combustion engines has not actually been reached: globally, components for conventional drive systems are still in high demand. We can assume that this situation is not going to change overnight. Even if the odd established brand such as DS, Smart or Volvo turn to electric drivetrains alongside newcomers like Byton, in 2025 the majority of new cars will still be rolling off the production lines with internal combustion engines (ICEs). The development plans of the Volkswagen Group are an important indicator for this. The company plans to sell 13 million cars globally in 2025, and up to 30 percent will be electric. So around 10 million models with petrol, diesel or gas engines will still be being produced. This forecast may apply to the other mass car producers, too.

However, suppliers are increasingly adapting to the electrification of mobility. One way the major suppliers are managing to do this is by demerging whole business areas which do not belong in the portfolio in the long term, and buying where there are gaps to be closed in future production. One example is Continental’s joint venture with Osram, which is meant to work on innovative light and laser technology for autonomous vehicles. Their goal is the development of intelligent light and sensor systems for the mobility of the future. These are meant to secure the communication of robo-cars (C2C) with each other, but also with other road users (C2X).

The recent takeover of the Austrian lighting specialist ZKW by the electronics giant LG for €1.1 billion shows the future significance of light – the most important driving assistance system of all. This was the Korean group’s biggest takeover deal and more than 9,000 employees were affected worldwide.

Interestingly, companies making conventional products that do not fall within the CASE (connected autonomous, shared and electric vehicles) boom and whose importance will decline in line with the combustion engine, are still able to find buyers. Bosch had no problem finding a buyer for its starter-generators business, or for the Bosch Mahle turbo systems area. These divisions were bought by Chinese investors or suppliers.

Chinese suppliers are gaining in importance, not least through transactions like these. Their number in the Top 100 has increased to four companies. Two of them have been on the list for years: Weichai Power (ranked 17, a producer of diesel engines among other things, shareholder with KION in Linde Hydraulics) and Yanfeng Automotive Interiors (ranked 33, formerly the interiors business of Johnson Controls and a producer of interior components). These two are joined by Citic Dicastal (ranked 74, producer of aluminum die-casting components and alloy rims) and Ningbo Joyson Electronics (ranked 75).

Chinese suppliers recorded huge growth rates in the past year: Weichai increased by 68 percent and Ningbo can look back on an increase of nearly 31 percent. Both are blue-chip companies, well fueled by state programs in China.

However, behind the rise of Ningbo lies the fall of Takata. In 2016, the passenger systems specialist had a solid middle ranking at number 51 – then faulty airbags resulted in the biggest product recall of all time and insolvency for the company. So the Japanese manufacturer disappeared from the survey and Ningbo Joyson took the stage. The Chinese company, only founded in 2004, has owned the US supplier Key Safety Systems (KSS) since 2016, which then took over Takata. Joyson itself produces electronic components such as control units for air-conditioning but also charging controllers for electric cars and steering wheels; the German premium manufacturers are among its customers.

An analysis by Berylls Strategy Advisors suggests that there could be significantly more Chinese companies in the Top 100 soon. The analysis examines the Chinese supplier market, where, perhaps unnoticed, new champions are developing. Especially promising are the Wanxiang-Conglomerate (suppliers of products including steering columns, drive shafts and front axle modules), but also the Minth Group, which is already producing interior and exterior vehicle components for international customers. The rechargeable battery producers CATL and BYD are also making their way up onto the list of the world’s 100 biggest suppliers.

To join this club, companies had to achieve a minimum turnover of €2.6 billion in 2017; the threshold was only 100 million and not far above the 2016 ranking. But a company needed to have had a strong year to join the Top 100 again and Japanese suppliers did manage to achieve this feat. With 27 representatives, they are again the biggest group in the Top 100: five companies even made it to the Top 20. The profitability of the Japanese is at the same level as in the previous year, even if the group is making a considerably worse impression in the rankings. The Yen carries the main responsibility for this, as it fell by 9 percent against the euro. If we disregard any exchange rate effects, only two companies (Yasaki, ranked 19, and Calsonic, ranked 32) recorded a decline in sales.

In South Korea, the situation looked quite different in 2017. It was a difficult year for the country’s suppliers, and in the end six out of seven companies reported falling profitability. Hankook Tyres (ranked 50) and Hyundai Mobis (ranked 7) were particularly hard hit, but Hankook was able to increase turnover slightly and even improve its overall ranking by two places.

Profitability was overwhelmingly in decline for the tire producers represented in the ranking, although if turnover is drawn up in local currency, tire producers are in the black.

The US dollar, considerably weaker against the euro, masked the success of American suppliers in the past year. There were even a few cases of sales growth far exceeding the average. The past year was particularly positive for American Axle, with an increase of 59 percent and a jump in the rankings from 65 to 51. The background for this is the company’s takeover of Metaldyne (supplier of silencers, exhaust parts and drive components), with 4,000 employees.

Much of the movement among US suppliers is due to continuing portfolio adaptions to future challenges. One example of this is the splitting up of Delphi into Delphi Technologies (focused on the production of components for traditional powertrains) and Aptiv (focused on components for new mobility solutions and connectivity). So Delphi drops out of the Top 20, but the spin-off Aptiv is ranked at 21 and even the smaller offshoot, Delphi Technologies, is at 62 with a turnover of €4 billion.

The wheel of takeovers and spin-offs has again been turning more quickly in 2017 than in the previous year and there is strong evidence that this will continue in 2018. The big players’ well-filled coffers and the general push to get even more involved in the digitalization of the automobile world indicate that 2018 will also be marked by quite major spin-offs and takeovers.

Creative start-ups wanting to join in with, and make their mark on, future mobility are also growing in importance. Their turnover in euros may be far below the Top 100 threshold of €2.6 billion, but their influence in the supplier industry is increasing in leaps and bounds. The Top 10 among the Silicon Valley start-ups (including Smartdrive, Greenroad, lytx, inthinc, nuTonomy, CRUISE) specializing in camera-based systems, driver attention and autonomous driving have raised €800 million to date, according to a recent M&A survey by Berylls Strategy Advisors. The Top 15 start-ups for car sharing have raised around €700 million (source: Berylls M&A Survey).

Financial backers increasingly include Tier 1 suppliers, who used to be more reserved about participating, as well as venture capital companies. But times are changing: the well-known car suppliers are now firmly on their way toward helping to develop the car of the future. That is because they have realized that, along with the tech titans from Silicon Valley, more and more of their Chinese rivals have joined the race.