he death knell has been sounding louder and louder for the classic (German) automotive industry in the last few years. The reason behind this? Outdated product ranges, as well as mobility solutions which by-passed customer needs, a complete lack of sustainability in its business model, and slow, inflexible company structures and procedures. No feature of a failing industry was missing in the state of Germany’s most important industry. However, the reality is turning out to be completely different.

Insight download and author information

Author

Dr. Jan Dannenberg

Partner

jan.dannenberg@berylls.com

The majority of OEMs and suppliers have been successful in riding out the economic consequences of Covid-19.The predicted wave of bankruptcies has (so far) not materialized. Lessons have been learned from the finance crisis of 2009, in which more than 120 prominent suppliers went bankrupt. Even if supply chains are not yet running smoothly, automotive companies were able to come up with peak values in turnover and profits in the final quarter of 2020.

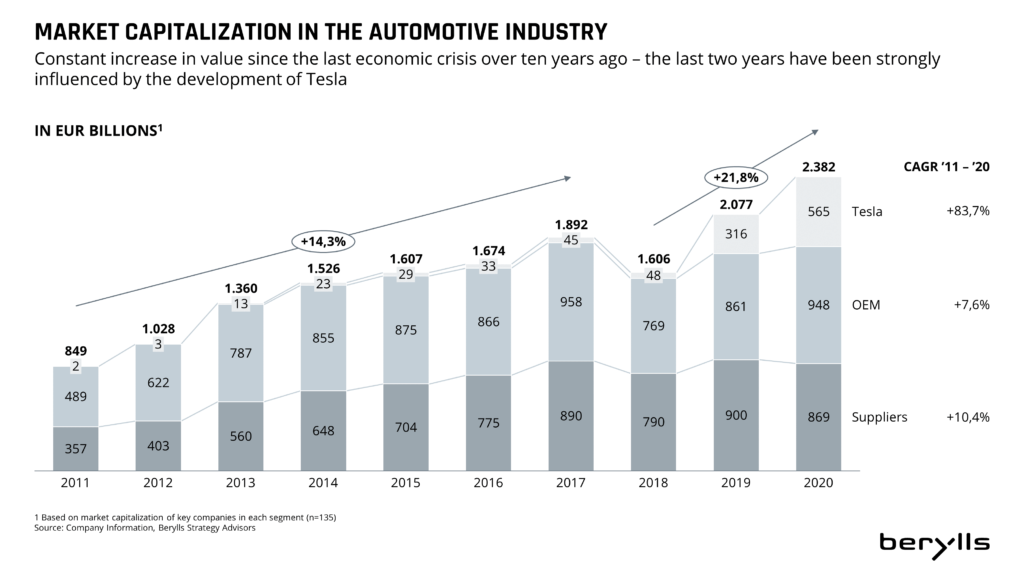

Even the field of electromobility is far from a lost cause. It is true that the present stock market capitalization of the electro pioneer Tesla stands at a good 500 billion euros, just about double that of the three German OEMs BMW, Daimler and Volkswagen. However, Tesla is launching a mere five new models/derivatives onto the market in 2020/21, whereas the German OEMs are producing a veritable flood of models: 88 new vehicles with electric drive (BEV and hybrid). And the Mercedes Benz EQS sets the standard for battery-powered electric cars. Audi has become the first German brand to announce a complete phasing-out of combustion engines. Competitors are racing to catch up.

German OEMs and suppliers are playing an active role in transforming the automotive industry as a whole. One third of worldwide research and development expenditure by automotive manufacturers comes from Wolfsburg, Munich and Stuttgart; in the next 10 years more than 300 billion euros will be spent on innovation. Most of the funds are being directed towards building up software skills, automatic driving, emission-free (electric) drive and connectivity, in order to guarantee attractive car travel in future. Currently, increasingly strict emissions standards can be met: in 2020 the European fleet of new cars just met the limit of 96 grams per vehicle, with 97 grams of CO2 per kilometer. And even the new EU7 regulations will be met thanks to electro-offensives and improved combustion technologies.

Even challenges from the “big tech players”: Google, Apple, Microsoft, Huawei or Samsung, are being confronted and not left to chance. The “software-defined car” has arrived in the higher echelons of suppliers and OEMs. Volkswagen, Bosch, Conti and co. are already employing hundreds of thousands of software developers. And in line with the motto “If you can’t beat them, join them”, new partnerships with big tech companies are continually being established.

The transformation of the automotive industry is by no means complete. German automotive suppliers and manufacturers are, however, doing their homework step by step, and they will be standing among the winners.

Berylls Strategy Advisors would be happy to support you in this key decision process.

Arthur Kipferler complements the expertise of the Berylls partner team in the fields of market & customer, technologies, sales, and digitalization, as well as in the development and implementation of corporate, product, and regional strategies.