ithin the past 20 years, the balance of power in capital markets has shifted enormously. If firms like Coca-Cola, General Electric, Ford, Disney, McDonald’s or Nokia were the most valuable companies worldwide in the 1990s, today it is Amazon, Facebook, Microsoft, Alibaba, Alphabet and Apple in the Top 10.

The intangible is taking over from the tangible. Apps, algorithms and artificial intelligence are ousting coal and steel. The market capitalization of the 10 largest car companies (including Tesla) is around €670 billion (as of the end of 2017), which corresponds to the market capitalization of Microsoft alone.

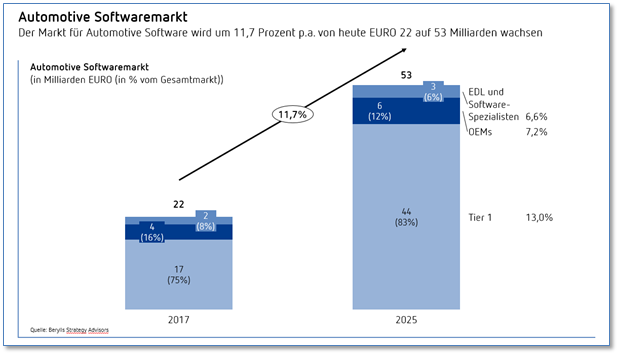

11.7 percent annual growth in automobile software

Software and data are what is making the difference to market valuations – and increasingly so in the car industry. Software value amounts to around 2 percent, or €240 per vehicle. That corresponds to 8 percent of the whole electric and electronics share that itself averages €3,020 per car.

Meanwhile, the renewable energy share for an average vehicle amounts to a good 24 percent of the production costs. However, the differences between individual vehicle classes are huge; in the premium segment the renewable energy share rises to 37 percent, around €14,500 per vehicle.

A forecast by Berylls Strategy Advisors shows that the market for automobile software will more than double by 2025. Whereas last year, the market size was €22 billion, Berylls’ forecasts are predicting a rise in market volume to €53 billion by 2025. By that time, every car will contain an average of €520-worth of software.

The reasons for this development are obvious: innovative features from the luxury class with a high share of software have increasingly been introduced in the volume segment. The best example of this is the MBUX multimedia system by Mercedes-Benz, which was first introduced in the compact segment (A Class) and has a greater range of functions than systems in significantly higher-cost vehicle segments.

All CASE (connected, autonomous, shared and electric) vehicle technologies take a high share of software value creation. Vehicle upgrades and updates facilitate new business models with great benefits for drivers and manufacturers. The data generated by the vehicle and driver can be passed on profitably to third parties or used for the company’s own benefit. The value added by software is cost-effective: software produced only once can be replicated millions of times. In this way, software is becoming the central interface of new functionalities in the car.

Electronics Tier 1s – the biggest beneficiaries of the software boom

In the car industry, it will first and foremost be the major electronics Tier 1 suppliers who benefit from software growth. The Berylls survey shows that in 2025 around 83 percent, or €44 billion, of complete car software value creation will be allocated to the major supply groups: Bosch, Continental, Denso, Lear, Aptiv (previously Delphi), Harman (Samsung), Valeo and Panasonic.

Nearly 12 percent of value creation (€6.3 billion) will be achieved by the OEMs themselves. But for the most part this is not about the actual development of code. More than that, software needs to be managed properly, for example to avoid the “incorrect” flashing of software to regulate emissions reduction. OTA (over-the-air) solutions to update software or improve and extend vehicle functionality will increase significantly.

There is also a group of specialist renewable energy engineering service providers (ESPs) and pure software players who are concentrating on the development of software solutions. These providers include the large generalists (total turnover between €500 million and €1 billion) such as Bertrandt, Assystem or AKKA/MBtech, as well as many electronics specialists with high-level software expertise: IAV, ESG, in-tech or Elektrobit (with turnovers between €100 and €250 million in the renewable energy area).

Pure software developers in the automobile area offer development tools as well as programming and testing. Examples of these are MathWorks, Vector Informatik, DSpace, ETAS, Green Hills, Luxoft and Mentor Graphics, with turnovers between €250 million and €1 billion. As a rule, the automobile sector is only one part of the business. All renewable energy – EDL and software specialists clear around €1.8 billion euros (8 percent of the total market). By 2025, their share will be around €3 billion euros or 6 percent of the market.

Small software and electronics specialists on the shopping lists of major suppliers and ESPs

The main reason for the reducing market share of software specialists lies in the extensive M&A activities of major Tier 1 suppliers and ESPs. In the past, firms such as Elektrobit (through Continental), Berner & Mattner, as well as Silver Atena (through Assystem), Gigatronik (through AKKA/MB Tech) or in-tech (Chinese suppliers), were taken over.

These acquisitions are extended by takeovers in CASE technologies. Acquisitions by the three major German suppliers in the past year give an impressive picture of this development:

However, the potential for new start-ups seems inexhaustible: the Berylls M&A survey of the car industry in 2017 shows 1,000 start-ups in the mobility sector. So this should keep supplies coming for company takeovers and highly innovative software players, as long as a considerable fly in the ointment can be removed: the lack of qualified software developers on the jobs market, which is currently preventing even stronger growth.

Authors

Dr. Matthias Kempf

Partner

matthias.kempf@berylls,com

Tobias Keil

Principal

About the author

Dr. Matthias Kempf (1974) was one of the founding partners of Berylls Strategy Advisors in August 2011. He began his career with Mercer Management Consulting in Munich, Germany, in 2000. After earning his doctorate degree and further consulting work at Oliver Wyman (formerly Mercer Management Consulting), he joined the management of Hilti Germany in 2008. At Berylls, his area of expertise is new mobility services and traffic concepts. In addition, he is an expert in developing and implementing new digital business models, and in the digitalization of sales and after sales.

Industrial engineering and management studies at the University of Karlsruhe, Germany, doctorate degree at Ludwig Maximilian University, Munich, Germany.