VEHICLE-AS-A-SERVICE: FROM VEHICLE SALES TO CUSTOMER AND VEHICLE LIFETIME VALUE MANAGEMENT

Munich, January 2022

VEHICLE-AS-A-SERVICE: FROM VEHICLE SALES TO CUSTOMER AND VEHICLE LIFETIME VALUE MANAGEMENT

Munich, January 2022

T

he automotive industry is going through the greatest period of transformation in its history with two disruptive forces impacting at the same time: Radical product innovation with electric and autonomous vehicles and new customer demands fundamentally changing the sales model.

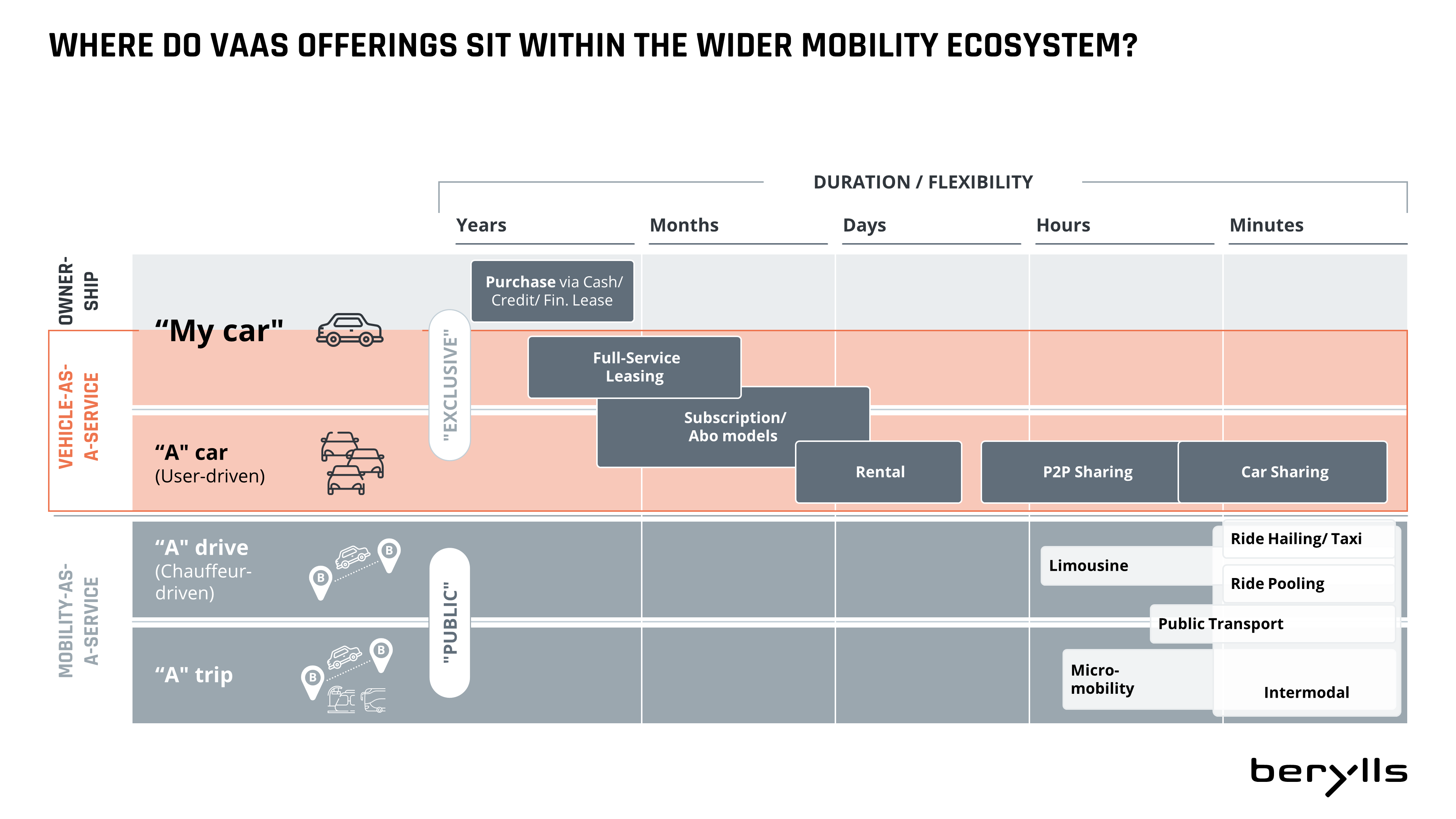

The automotive industry is the last major sector whose underlying business and sales model hasn’t been disrupted by digitization – until now. The Vehicle-as-a-Service (VaaS) model allows customers to use vehicles for a variety of time periods ranging from years to minutes, via products such as vehicle leasing, subscriptions, and short- and mid-term rentals. As a result, VaaS will turn on its head the decades-old model of cars being sold to one owner through a dealership. For this study, we have conducted representative survey of 2,040 private customers in the age group of 16-56 years (GenX – Z) in Germany to understand where, how and why they are going to buy/ order vehicles. The survey sample covers new, used & non-car customers for all brands (premium & volume) and regions (rural vs. metropolitan). The objective is to listen to the voice of the younger generations to analyze the changes in vehicle usage & ownership needs of tomorrow’s automotive customers.

EXECUTIVE SUMMARY OF OUR FINDINGS

To meet their mobility needs, customers increasingly want to move from vehicle ownership toward use-based models (38% increase in market share by 2025) that offer greater flexibility and access to the latest technology, while minimizing risk.

As a result, these ‘Vehicle-as-a-Service’ (VaaS) products massively gain in importance – and also attract people who don’t have cars today, unlocking an additional potential market of 1.32 million customers (in Germany alone).

VaaS customers are five times more willing to order via new channels (online/ digital) and via a wider range of third-party multi-brand providers, going beyond carmakers and dealerships.

Brand loyalty among VaaS customers is 50% lower compared with traditional customers, posing a risk that incumbent carmakers and dealers will lose market share to new players – while enabling new EV-only brands to enter the market without requiring big budgets to build offline sales networks.

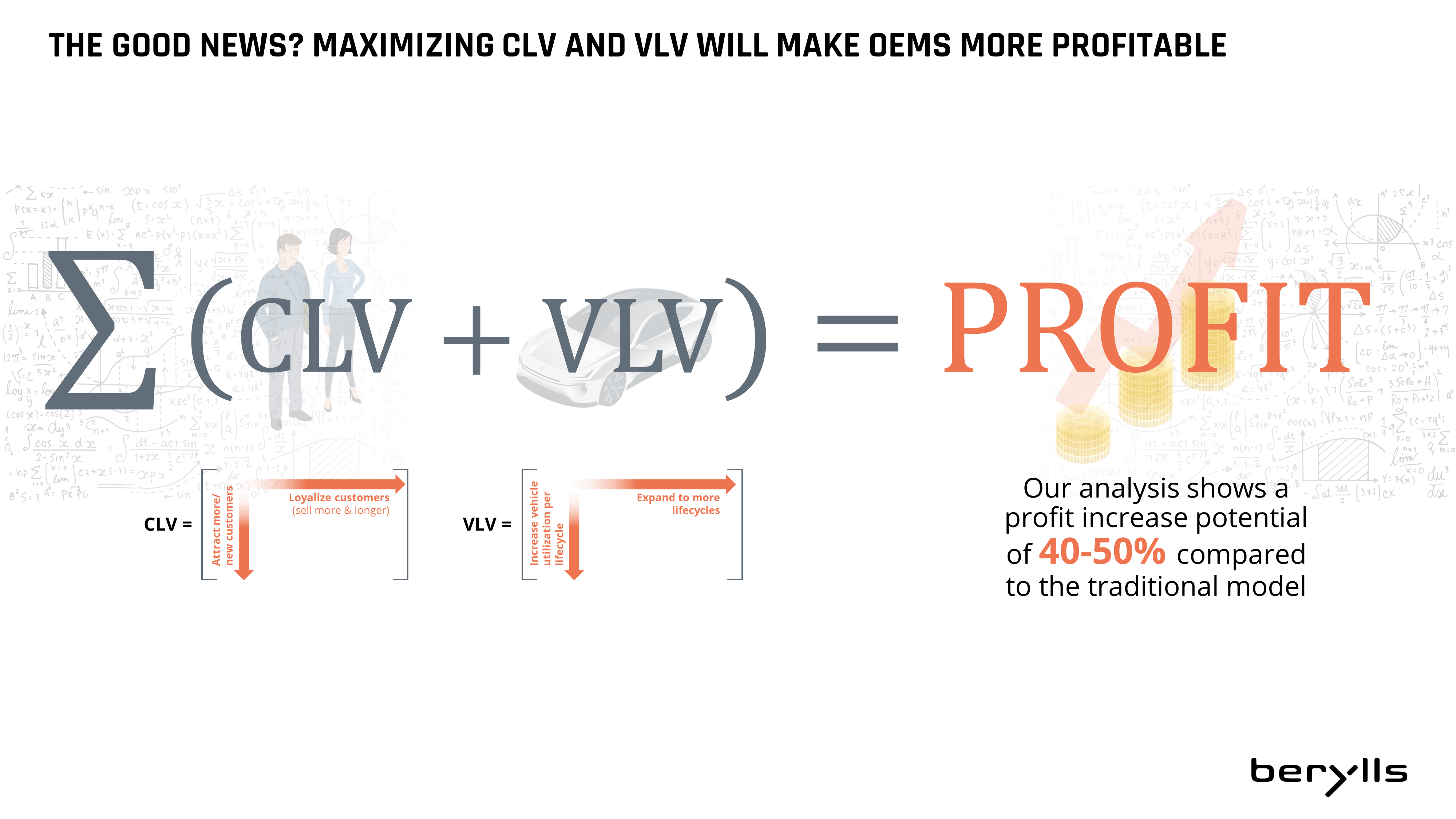

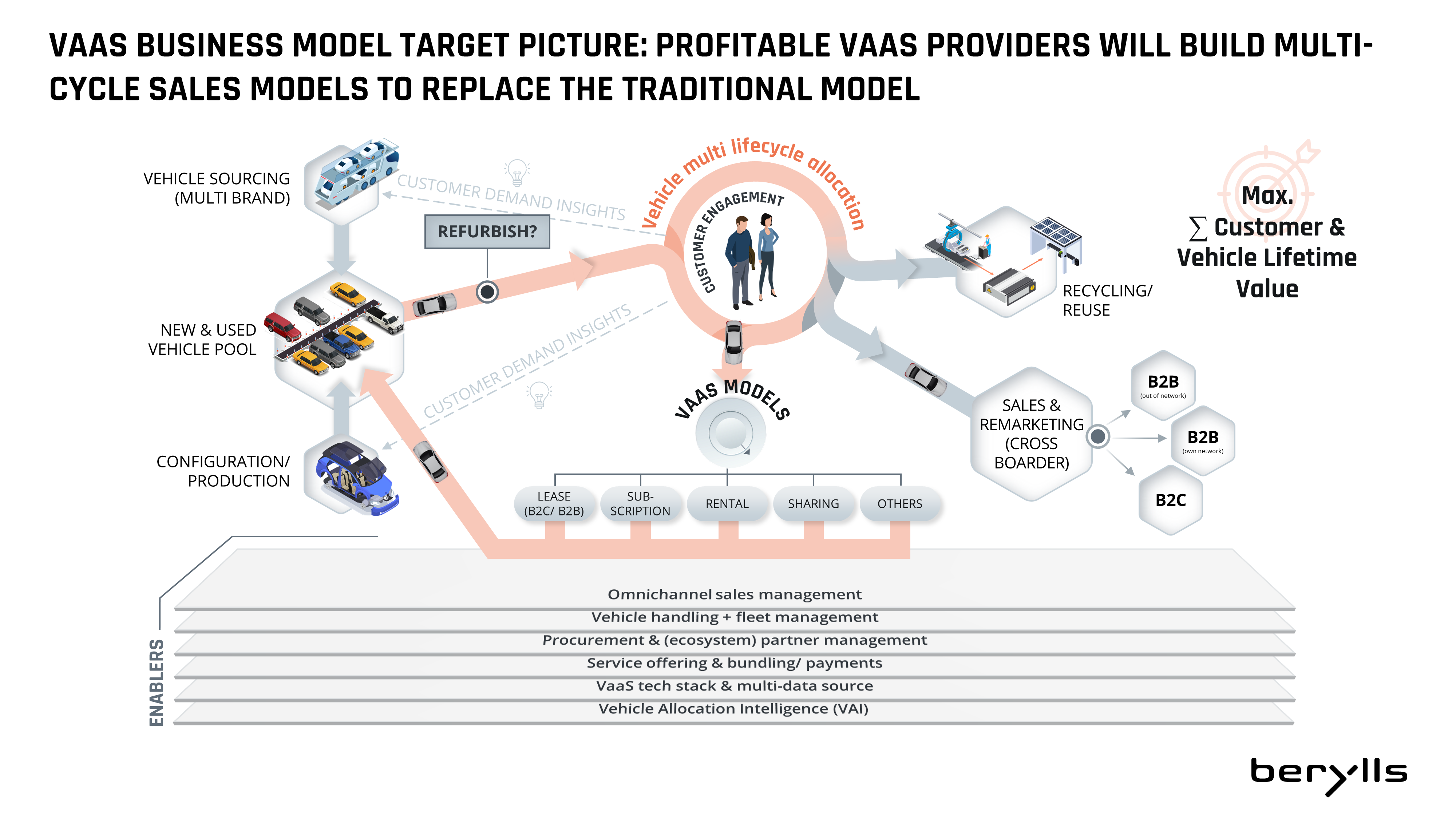

The car industry’s entire sales and business model will change dramatically as vehicles return to providers after shorter cycles. This means more sales events and customer interactions for providers, making operations more complex, but also brings more profit opportunities.

Berylls Insight

VEHICLE-AS-A-SERVICE: FROM VEHICLE SALES TO CUSTOMER AND VEHICLE LIFETIME VALUE MANAGEMENT [24 MB]

Christopher Ley (1984) joined Berylls in October 2021 as Principal. He has over twelve years of top management consulting experience with focus on new business models and market expansions within the automotive & mobility industry. He is an expert around Vehicle-as-a-Service, comprising vehicle finance & leasing, fleet management and mobility services. Christopher Ley is advising OEMs, Captives, Financial Services Companies & Investors, Leasing & Rental Companies, Fleet Managers and Mobility Startups around the transformation from one-time sales towards use-based multi-cycle business models on a global level.

Prior to joining Berylls, Christopher Ley has been working for other international management consulting firms, amongst others Monitor Deloitte and Alvarez & Marsal. He holds a diploma degree in business administration from Johannes Gutenberg-Universität in Mainz and an MBA from Colorado State University.