WANT TO DISCOVER MORE?

he electrification of mobility in China, strongly supported by the state, is playing right into the hands of Chinese car suppliers.

A handful of Chinese companies are currently among the global Top 100 automotive suppliers. Among others, Weichai Power and Yanfeng Automotive Interiors, suppliers of diesel engines and interior systems respectively, are ranked as “pure” Chinese companies. Pirelli and Nexteer meanwhile, have Chinese majority shareholders or are under Chinese ownership. Outside the Top 100, many medium-sized suppliers are also under Chinese ownership, for example Kiekert and Hilite.

Weichai Power, currently ranked no. 17 in the list, had a total turnover of €11.9 billion in 2017. Alongside engine production, the company has consistently expanded its product portfolio, which now includes gears, axles, control units and other components, such as for forklifts and commercial vehicles. Acquisitions outside China including Kion (2013) or Linde Hydraulics (2012) have contributed significantly to the growth of Weichai Power.

Yanfeng Automotive Interiors is currently the world’s largest supplier of vehicle interiors. The company, the result of a joint venture with Johnson Controls, supplies OEMs with comprehensive interior solutions and achieved a turnover of €7.1 billion in 2017. Through its relationship with Kostal, the company can also offer human machine interface (HMI) solutions. Yanfeng also supports some joint ventures, for example with KSS (safety systems such as airbags, safety belts and steering wheels), Plastic Omnium (exterior parts such as bumpers and radiator grilles) and Adient (seats and seat components).

The success stories of both these companies indicate that more Chinese companies are going to be moving into the Top 100. To this end, various strategies are being pursued. Established suppliers use internationalization, as well as moving component suppliers horizontally and vertically to module/system suppliers in the value creation chain, to achieve turnover growth. A whole range of new suppliers are using the rapid development of e-mobility in China to drive their growth.

International expansion, along with technology development and extension of know-how, is typically accelerated by acquisitions abroad. Examples of this are Nexteer, Kiekert and the starter and generator maker Sparte (SG) by Bosch, which was taken over in 2017 by the Zhengzhou Coal Mining Machinery Group (ZMJ). Because ZMJ was mainly active in the Asian region before the takeover, the takeover gives the company not only immediate access to the European market, but also to supply premium European and American OEM customers in Asia. Ningbo Joyson (ranked no. 75) has also been able to achieve enormous turnover growth through takeovers abroad. In Germany these include the takeovers of Preh (2011), Quin (2015) and TechniSat Automotive (2016), as well as the takeover last year of the troubled Japanese supplier Takato by the Ningbo Joyson subsidiary, KSS.

Horizontal movement – i.e. the expansion of the product portfolio – and evolving from a component into a system supplier are also typical growth strategies used by Chinese suppliers. One good example of this is the largest supplier conglomerate in China: the Wanxiang Group (turnover €xxx billionin 2017). The company started in the late 1970s, producing universal joints for cardan shafts. Since then Xanxiang has not only constantly expanded its portfolio, but has also consistantly evolved into a module/system supplier through targeted acquisitions. The current portfolio includes steering columns, axle shafts, water pumps, silencers, brake calipers, front axis modules and small power units. Battery producer A123 has been a part of this conglomerate since 2013 and Fisker Automotives since 2016.

Another example of typical Chinese company growth is the Minth Group (turnover €xxx billion in 2017), which offers interior and exterior components (radiator grilles, roof racks, door sills etc.). The company has massively expanded its portfolio by producing structural components, control units and seat components. Since 2016 Minth has also been the first company from the supply industry to hold a license to build BEVs. Fulin Precision Machining and Shengrui Transmission are also companies following a similar growth path to Wanxiang and Minth.

The internationalization and in particular the verticalization of their portfolio present the companies with new challenges. Although process chain management of the production of parts and components is still comparatively easy, the integration of components and modules into complete systems requires comprehensive system knowledge.

While autonomous driving and connectivity in China are dominated by the internet giants Ali, Baidu and Tencent, e-mobility does offer opportunities for new suppliers. As the largest single market for BEVs (known in China as NEVs – new energy vehicles), battery producers of Chinese origin (e.g. CATL, BYD, Guoxuan, Lishan, BAK, and CALB) already had around 35 percent of global market share for installed battery capacity in 2016. This share is expected to increase to 45 percent by 2025.

CATL and BYD are currently among the obvious market leaders. In 2017 CATL achieved a turnover of around €2.6 billion (34 percent higher than the previous year) and a considerably improved profit margin of around 20 percent compared with 2016. CATL acts both as a cell pack supplier and as a rechargeable power pack supplier, and supplies numerous Chinese OEMs such as Geely and FAW, Chinese NEV start-ups such as NIO and WM, and the local joint ventures of BMW and Volkswagen. CATL has now reached a market share of 29 percent on the domestic market.

A supplier landscape has also developed in the e-mobility ecosystem around vehicle charging. This includes companies whose products range from hardware production to installation of charging stations, operation and back-end solutions. SAIC Anyo, Starcharge, Wanma and Zhida are some of the more important companies in this segment, however their business operations are still very much limited to the Chinese region.

With the continuing growth in global car production and the sustained high domestic demand in China, it can be assumed that five more Chinese suppliers will join the Top 100 club within the next three years. International competition and cross-border consolidation look set to gain considerable momentum once again.

Dr. Jan Dannenberg (1962) has been a consultant for the automotive industry since 1990 and became a founding partner of Berylls Strategy Advisors in May 2011. Until spring 2011, he worked with Mercer Management Consulting and Oliver Wyman in Munich, Germany, on international projects – for five years as Associate Partner, and another three years as Partner. He is a recognized specialist in innovation and brand management in the automotive industry, and primarily advises suppliers and investors on strategy, M&A and performance improvement. In addition he is Managing Director at Berylls Equity Partners, an investment company that specializes on mobility enterprises.

Bachelor of Arts in economics at Stanford University, USA; business administration and doctorate degree at the University of Bamberg, Germany.

ithin the past 20 years, the balance of power in capital markets has shifted enormously. If firms like Coca-Cola, General Electric, Ford, Disney, McDonald’s or Nokia were the most valuable companies worldwide in the 1990s, today it is Amazon, Facebook, Microsoft, Alibaba, Alphabet and Apple in the Top 10.

The intangible is taking over from the tangible. Apps, algorithms and artificial intelligence are ousting coal and steel. The market capitalization of the 10 largest car companies (including Tesla) is around €670 billion (as of the end of 2017), which corresponds to the market capitalization of Microsoft alone.

Software and data are what is making the difference to market valuations – and increasingly so in the car industry. Software value amounts to around 2 percent, or €240 per vehicle. That corresponds to 8 percent of the whole electric and electronics share that itself averages €3,020 per car.

Meanwhile, the renewable energy share for an average vehicle amounts to a good 24 percent of the production costs. However, the differences between individual vehicle classes are huge; in the premium segment the renewable energy share rises to 37 percent, around €14,500 per vehicle.

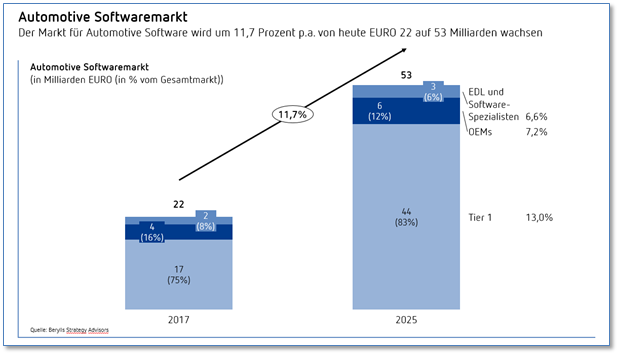

A forecast by Berylls Strategy Advisors shows that the market for automobile software will more than double by 2025. Whereas last year, the market size was €22 billion, Berylls’ forecasts are predicting a rise in market volume to €53 billion by 2025. By that time, every car will contain an average of €520-worth of software.

The reasons for this development are obvious: innovative features from the luxury class with a high share of software have increasingly been introduced in the volume segment. The best example of this is the MBUX multimedia system by Mercedes-Benz, which was first introduced in the compact segment (A Class) and has a greater range of functions than systems in significantly higher-cost vehicle segments.

All CASE (connected, autonomous, shared and electric) vehicle technologies take a high share of software value creation. Vehicle upgrades and updates facilitate new business models with great benefits for drivers and manufacturers. The data generated by the vehicle and driver can be passed on profitably to third parties or used for the company’s own benefit. The value added by software is cost-effective: software produced only once can be replicated millions of times. In this way, software is becoming the central interface of new functionalities in the car.

In the car industry, it will first and foremost be the major electronics Tier 1 suppliers who benefit from software growth. The Berylls survey shows that in 2025 around 83 percent, or €44 billion, of complete car software value creation will be allocated to the major supply groups: Bosch, Continental, Denso, Lear, Aptiv (previously Delphi), Harman (Samsung), Valeo and Panasonic.

Nearly 12 percent of value creation (€6.3 billion) will be achieved by the OEMs themselves. But for the most part this is not about the actual development of code. More than that, software needs to be managed properly, for example to avoid the “incorrect” flashing of software to regulate emissions reduction. OTA (over-the-air) solutions to update software or improve and extend vehicle functionality will increase significantly.

There is also a group of specialist renewable energy engineering service providers (ESPs) and pure software players who are concentrating on the development of software solutions. These providers include the large generalists (total turnover between €500 million and €1 billion) such as Bertrandt, Assystem or AKKA/MBtech, as well as many electronics specialists with high-level software expertise: IAV, ESG, in-tech or Elektrobit (with turnovers between €100 and €250 million in the renewable energy area).

Pure software developers in the automobile area offer development tools as well as programming and testing. Examples of these are MathWorks, Vector Informatik, DSpace, ETAS, Green Hills, Luxoft and Mentor Graphics, with turnovers between €250 million and €1 billion. As a rule, the automobile sector is only one part of the business. All renewable energy – EDL and software specialists clear around €1.8 billion euros (8 percent of the total market). By 2025, their share will be around €3 billion euros or 6 percent of the market.

The main reason for the reducing market share of software specialists lies in the extensive M&A activities of major Tier 1 suppliers and ESPs. In the past, firms such as Elektrobit (through Continental), Berner & Mattner, as well as Silver Atena (through Assystem), Gigatronik (through AKKA/MB Tech) or in-tech (Chinese suppliers), were taken over.

These acquisitions are extended by takeovers in CASE technologies. Acquisitions by the three major German suppliers in the past year give an impressive picture of this development:

However, the potential for new start-ups seems inexhaustible: the Berylls M&A survey of the car industry in 2017 shows 1,000 start-ups in the mobility sector. So this should keep supplies coming for company takeovers and highly innovative software players, as long as a considerable fly in the ointment can be removed: the lack of qualified software developers on the jobs market, which is currently preventing even stronger growth.

Dr. Matthias Kempf (1974) was one of the founding partners of Berylls Strategy Advisors in August 2011. He began his career with Mercer Management Consulting in Munich, Germany, in 2000. After earning his doctorate degree and further consulting work at Oliver Wyman (formerly Mercer Management Consulting), he joined the management of Hilti Germany in 2008. At Berylls, his area of expertise is new mobility services and traffic concepts. In addition, he is an expert in developing and implementing new digital business models, and in the digitalization of sales and after sales.

Industrial engineering and management studies at the University of Karlsruhe, Germany, doctorate degree at Ludwig Maximilian University, Munich, Germany.

ardly a day goes by when we are not confronted with the concept of “digital transformation” and the car industry is no exception. Structural change is taking place with ever-increasing speed. Manufacturers and suppliers are now faced with changes such as vehicle networking, highly automated or even autonomous vehicles, new mobility products, Big Data, and alternative drive systems. As a result, they are having to reorganize the business model they have had in place for decades.

Digitalization has the potential to shake up value chains and distribution, with a considerable impact. However, companies can improve their existing positioning, and develop new business models, by introducing product and process innovations:

The multifaceted drivers of digitalization in industrial manufacturing, including the Internet of Things, Industry 4.0, mobile devices and Big Data, affect companies in the supplier industry with varying degrees of relevance and urgency. This means that an in-depth discussion about the importance of digital transformation becomes necessary in every company, in order to make use of opportunities and identify risks as early as possible and be able to take the relevant countermeasures.

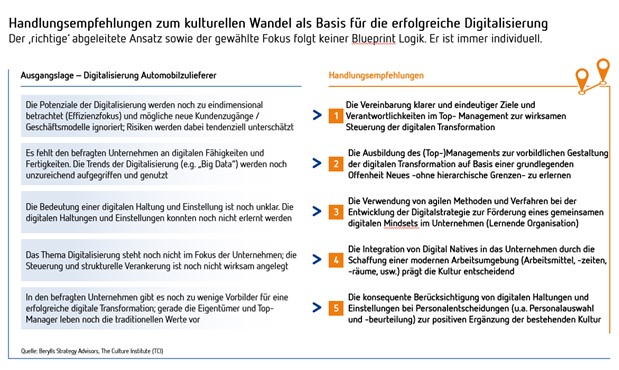

In this context, organizations are increasingly asking themselves to what degree the existing company culture allows for managing high-complexity digitalization. Small and medium-sized suppliers are on the verge of missing the boat here. Company culture is often still organized along traditional lines and can work against the need for agility, flat hierarchies and self-managed teams in digital transformation projects. Even “trial and error” methods and short development cycles with the close involvement of external partners are often difficult to carry out within a long-established culture.

Although the relevance and urgency of digitalization is accepted, hardly any companies have a real masterplan for carrying it out. It is not immediately apparent what the future direction of the business should be and to what extent digitalization is going to change the company. The question that often remains is whether the company can continue to exist as a component or system supplier or whether an entirely new business model must be developed. For many companies it is simply not possible to identify and use the opportunities that are arising, for example from the application of Big Data. For this reason many medium-sized companies focus primarily on process and cost optimization instead. The fact that digitalization can offer direct customer access is often overlooked.

As a result, there is a lack of understanding about the opportunities created by new products, services or digital business models, and the existing potential for new sources of revenue is more or less ignored. Many suppliers’ financial resources are also insufficient to meet the cost of digital transformation and there is a shortage of people with the right digital skills.

Despite these factors, existing company culture is often cited as the most frequent reason for a non-existent masterplan and a lack of comprehensive discussion about digitalization.

Berylls’ Company Culture 4.0 survey shows company culture to be a significant success factor and many suppliers are indeed working intensively on that: management teams discuss and reflect on their perceptions of culture, describe values, norms and basic beliefs about leadership and co-operation, and in many cases train their staff in how to deal with these. So why is commitment not leading to a comprehensive discussion about digitalization?

Berylls believes the following factors are behind the lack of progress:

To achieve success, the necessary culture patterns of digital transformation need to be identified to define the right measures to be taken for organizational development. Is the existing company culture a help or a hindrance when it comes to the complex demands of digitalization? The company cultures of many organizations show a lack courage to take new pathways, are closed to innovative ideas, favor a culture of debate rather than a pursuit of harmony, and lack the strength to implement change in the face of resistance. Courage as a quality is often dismissed as recklessness and determination as obstinacy. But both of these are attributes without which a fundamental change cannot be tackled.

This is why Berylls Strategy Advisors has established a set of recommendations for adapting company culture to meet the needs of digitalization – for medium-sized companies in particular – without losing the elements that make them successful right now. Our recommendations are continually being redeveloped, with the help of company culture experts and collaboration partners:

Peter Eltze (1964) joined Berylls Strategy Advisors as a Partner in November 2015. He began his career in the medical technology division of an integrated technology corporation, and became a project manager at Malik Management Zentrum St. Gallen in 1996 before being appointed Partner in 2001. From 2003, in his role as member of the executive board, he was in charge of Management Education & Development. Since the end of the 1990s, Peter Eltze has advised companies in the automotive and mechanical engineering industries. At Berylls, his consulting activities focus on integrated organizational development (strategy, structure, culture), transformation management, and executive development.

Education in wholesale and international trade; administrative sciences at the University of Constance, Germany.

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Vimeo. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from hCaptcha to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from Turnstile to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from hCaptcha to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information