NO TIME TO READ THIS WEBSITE?

WANT TO DISCOVER MORE?

SEARCH

ecided to implement the agent model? What now?

In our recent publication „Dealer vs. Agent” we have concluded a draw (3:3) between the classic “Dealer Model” and the direct sales “Agency Model”.

Nevertheless, it appears the Agent’s following is growing, not least due to the need to keep track with the cost efficiency of new, direct selling entrants. A desire to reap the benefits of digitalization and to cater to the customers’ expectations when it comes to a premium sales and service experience are other factors.

Together with the evaluation of direct sales via agents as a new go-to-market model you must immediately ask “How can we make this transformation work?” To help we want to draw a potential path for a successful sales model transformation in this article.

Structure helps, so here is our three-step approach:

Direct sales can beat a dealer-based wholesale model on four dimensions – but you will have to pick your battles, not all of them can be at the same time:

Like for every successful journey, finding the best route comes right after setting the destination. Nobody can realistically switch over a decade-old global go-to-market structure in one go – identifying the right steps and the best way to scale up is a key success factor. And there are a number of building blocks for this roadmap:

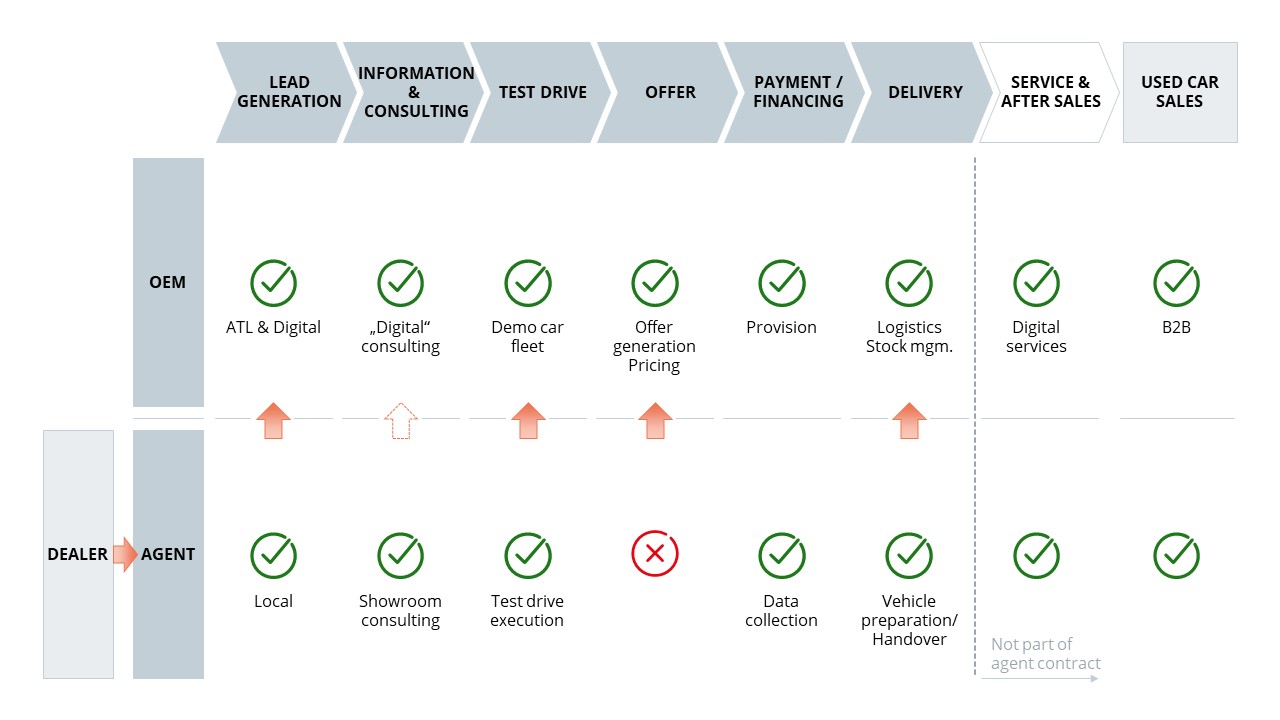

Implementing any direct sales model inevitably leads to a shift of tasks from the former dealer to the OEM across the whole customer journey, as shown in Figure 1. OEMs have to take on new and complex tasks, such as pricing or inventory planning – with on the retail level have much higher frequency and granularity that what NSC and regional staff are used to from their matching wholesale tasks. Process performance and integration with the agents must be excellent from the switch-over date to achieve a seamless customer journey.

Financing and Digital Services remain largely unchanged, since they are widely in OEM hands already today. The Used Car Business will largely remain under control of the agents.

Of course, in addition to the tasks along the customer journey, there are also new or changed tasks for the OEM around agent steering, interaction management, data management, etc. which require careful setup before the switch-over – from the organisation design along the steering, process, and structural dimension to the design and creation of the supporting IT systems and not ending at recruiting and onboarding the additional staff.

It all starts with the objectives – it is crucial to make the transition for the right reasons. Ensure alignment across your whole organisation, once on the way it will be really difficult to shift priorities. Strictly guard your target hierarchy also in interim stages – an improved customer experience cannot be expected if different sales models have to co-exist under the same retail rooftop. Be more than aware of the additional tasks for the wholesale level – it will in essence also become your retail level. And expecting immediate cost reduction effects in a transition phase with increasing structural costs can only lead to disappointment.

Most importantly, keep putting yourself in your customers’ shoes: you need to deliver a customer experience where OEM and agent work hand in hand, where online and offline touch-points are well-connected. In an agent model it will always be the OEM that is in the driver seat, using the agents as extended arms into the local markets. This orchestration across the omnichannel system requires clear governance and effective steering since – unfortunately – objectives between agents and OEMs are not always aligned.

Keep all this in mind when you are designing the details of your future agent system – it is not just a new dealer contract you are about to implement.

Arthur Kipferler (1963) started his career in 1989 at the Boston Consulting Group, where he consulted for 13 years in the automotive industry. After consulting, Arthur Kipferler held senior management positions at Toyota in Europe and the U.S. From 2013 to 2014, he was global head of the BMW Group’s Future Retail program. Subsequently, he had leading roles in strategy, corporate planning and transformation management at Jaguar Land Rover in Coventry, UK. Arthur Kipferler complements the expertise of the Berylls partner team in the fields of market & customer, technologies, sales, and digitalization, as well as in the development and implementation of corporate, product, and regional strategies.

Mechanical engineering, production engineering, at the Technical University of Munich (TUM); MBA in Strategy, Marketing and Organizational Behavior at INSEAD Business School, France.

NO TIME TO READ THIS WEBSITE?