NO TIME TO READ THIS WEBSITE?

WANT TO DISCOVER MORE?

SEARCH

he shift from conventional engines to battery electric vehicles (BEVs) is revolutionizing the auto industry. However, until battery performance and cost improve, BEVs will continue to struggle to take over from gasoline-powered vehicles as the mainstream choice for drivers.

Widespread adoption of BEVs is essential to meet emissions reduction targets and for OEMs and suppliers to see a return on their huge investments in the engine technology. Achieving it hinges, in part, on critical advancements in battery technology.

Undoubtedly, the BEVs available now offer a number of benefits, including lower emissions and less engine noise. However, limitations on range, long charging times, high cost and safety concerns are dampening consumer enthusiasm for the electric vehicle transition. Improvements in battery technology hold the key to solving these critical issues, particularly advancements in energy density, charging speed and safety. In this article, we assess the changes in battery technology that could unlock the full potential of BEVs, focusing on solid-state batteries, long held out as the solution to longer battery life.

The success BEVs have had to date only became possible through advancements in lithium-ion (Li-ion) battery technology. Li-ion batteries offer medium-to-high energy density, storing a significant amount of energy per unit weight compared to other battery technologies, giving them a longer driving range. Li-ion batteries also have a comparatively long life cycle, meaning they can be recharged and used hundreds to thousands of times before capacity and performance starts to diminish. This translates into a longer lifespan for the battery pack in BEVs, reducing replacement costs, decreasing maintenance needs, and minimizing the environmental impact of battery production and disposal.

Compared to newer technologies still under development, Li-ion battery production is also well-understood and efficient. An established manufacturing process has resulted in greater cost-effectiveness, driving down the overall cost of BEVs and making them more accessible to a wider range of consumers.

However, charging a Li-ion battery still takes significantly longer than refilling a car’s gas tank, even using a fast charger. The average refueling time for a vehicle with an internal combustion engine is less than 5 minutes, while charging time for a BEV with a 65 kWh battery using an ultra-fast 150 kW charger is around 20 minutes. This can be inconvenient for drivers, especially on long trips, and doesn’t suit driving habits that have come to rely on making quick stops to refuel. Faster charging is crucial for improving the overall driver experience with BEVs.

Another key downside is in the supply chain. Production of Li-ion batteries relies heavily on the key components of lithium, nickel and cobalt, which are only produced in large quantities in a limited number of places around the world, creating supply chain vulnerabilities and raising ethical concerns regarding sourcing practices in certain regions. Finding alternative materials or more sustainable sourcing methods is essential for the long-term viability of BEV technology.

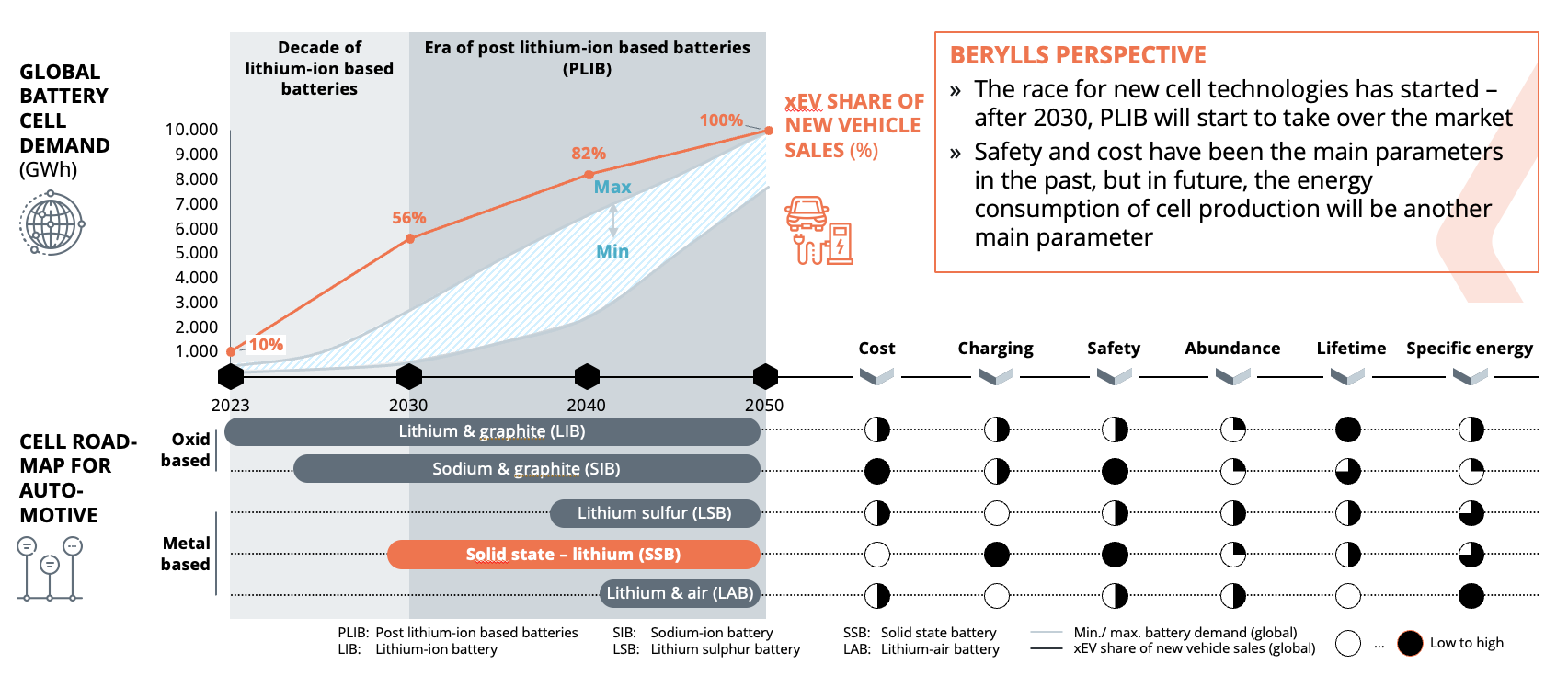

Several new battery technologies aim to solve the shortcomings of Li-ion. Sodium-ion-graphite batteries, for example, have been in development over the past few years but have not yet progressed to commercialization due to their current high cost and lower energy density. Lithium-sulfur batteries are in the early stages of research and development so less is known about their potential, but they cost roughly the same as Li-ion batteries and have a higher energy density. Lithium-sulfur batteries have relatively low performance in charging speed, safety, and battery lifetime, but will likely progress with further development.

Source: Berylls by AlixPartners, FFB Münster

One of the main focuses in current battery R&D is solid-state batteries (SSBs). Unlike traditional lithium-ion batteries that rely on liquid electrolytes, SSBs use solid electrolytes. These come in different forms, including oxide, sulfide and polymer. One of the most exciting aspects of SSBs is their potential for significantly higher energy density compared to the Li-ion batteries being made today. This means longer driving ranges and faster charging times for BEVs, which could eliminate range anxiety, one of the major barriers to widespread BEV adoption.

SSBs also have a significant safety advantage over lithium-ion batteries. The absence of flammable liquids or gases in the solid electrolyte minimizes the risk of explosion or fire compared with traditional lithium-ion batteries, which could be a major selling point for consumers hesitant about BEVs due to safety concerns

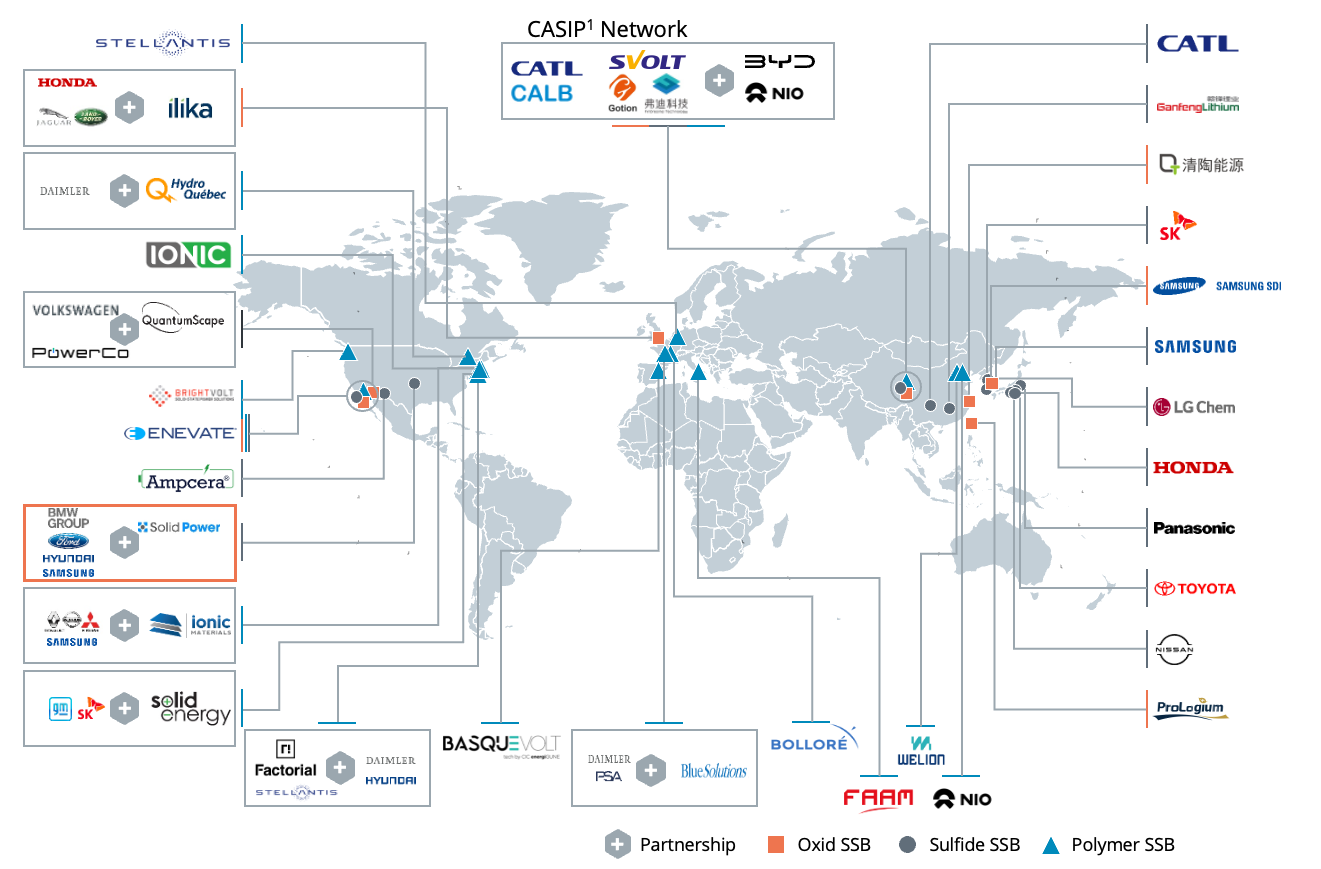

There has been significant global interest in SSB technology from OEMs (including Stellantis, BYD, Toyota and GM), incumbent battery suppliers (CATL, Samsung and LG, among others) and startups (including QuantumScape, Solid Power and Factorial Energy). The major SSB players are primarily in the US, East Asia, and to a smaller degree Europe. OEMs are engaging in partnerships with SSB startups – Volkswagen’s joint venture with QuantumScape for example – to capitalize on the technology’s potential when it becomes available on a commercial scale. New collaboration models like China’s CASIP (China All-Solid-State Battery Collaborative Innovation Platform), a consortium of battery incumbents, startups and OEMs, highlight the technology’s significance and the resource commitment being made by many stakeholders.

As the chart below shows, other cooperation models already underway include silent investment, for example by Toyota and Nissan, and technology “openness”, as seen in Factorial’s technology development partnership with Mercedes-Benz.

Note: CASIP: newly established R&D network named China All-Solid-State Battery Collaborative Innovation Platform

Source: PEM Motion, Berylls by AlixPartners

For all these reasons, SSBs have considerable promise for the auto industry. However, there are two fundamental challenges hindering their widespread adoption at scale: production difficulties and technical hurdles.

Production difficulties: Transitioning from established Li-ion battery production to SSBs requires transformational changes in manufacturing. Producing solid electrolytes involves complex processes that are quite different from the well-established methods used for lithium-ion battery components. Developing and scaling up this technically difficult production process will take significant investment in new manufacturing infrastructure. High costs and quality control issues, particularly for oxide and sulfide-based electrolytes, also pose major challenges to mass production and further contribute to the higher cost of SSB production.

Technical hurdles: Materials are one of the key challenges for solid-state battery technology because the solid electrolyte (separator that allows ions to pass) needs to be both ionically conductive and mechanically robust. This ensures efficient operation and prevents leaks or degradation within the battery. Additionally, interface compatibility between the electrodes (the positive and negative battery terminals) and the electrolyte is crucial. Dendrite formation (needle-like lithium structures) and lithium loss can occur at the interface, leading to a reduced cycle life (the number of times the battery can be charged and discharged) for the SSB.

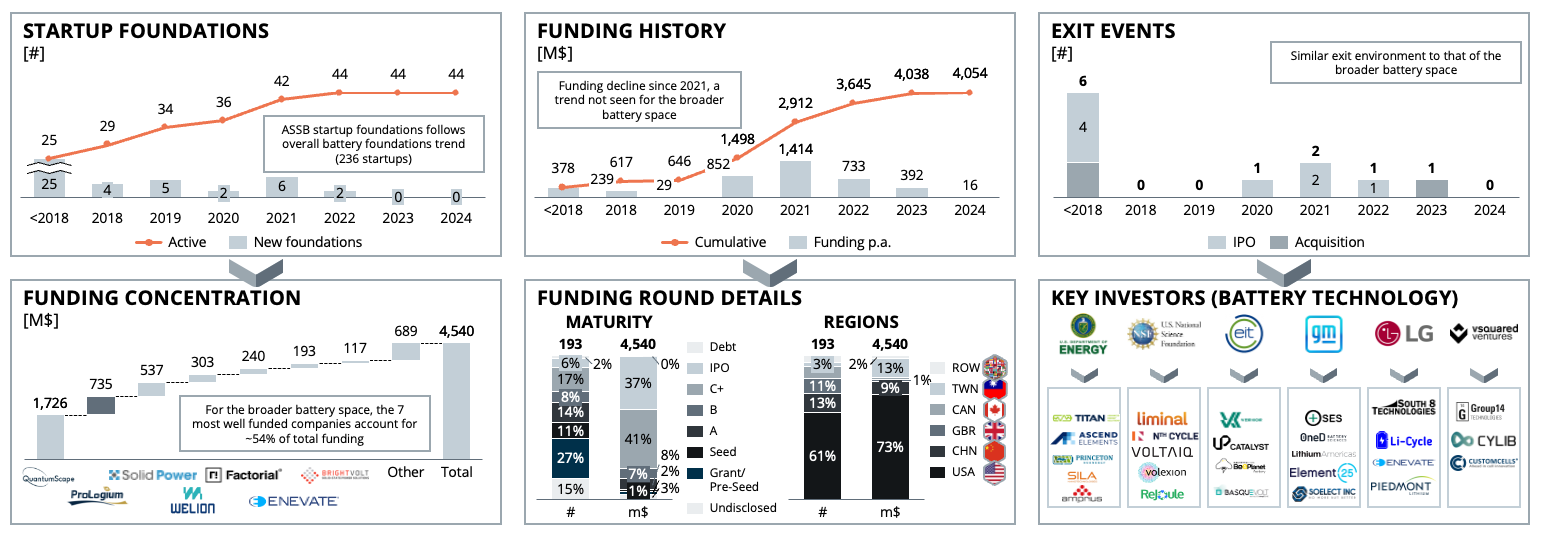

There is an appetite for SSB investment – and startups are benefitting

Overcoming these production and technical challenges is vital in order to manufacture SSB batteries on the scale needed for the auto industry. Fortunately, there is significant investment going into R&D and production capability, and the global market for solid-state batteries is forecast to grow substantially. Optimistic estimates¹ suggest production capacities could reach 420 GWh by 2035, reflecting a potential compound annual growth rate (CAGR) of 21%. Polymer electrolyte-based SSBs are expected to have the highest market share by 2035 (224 GWh, or 53%) followed by sulfide (117 GWh, 28%) and oxide (78 GWh, 19%).

SSB startups have benefitted from the interest in the technology with more than $4bn invested to date. That compares with investment (or planned investment) of >$10bn across the industry including OEMs and incumbent battery manufacturers. Larger startups have seen the bulk of this funding, however, with the top seven receiving around 85% of the investment, leaving 37 companies to compete for the remaining 15%. This is likely to lead to consolidation, so that only the largest players survive the race to develop SSBs at scale. The charts below show where funding has gone to date, and the key investors:

Note: Selected companies based on relevance

Source: Crunchbase, Leap435, PEM Motion, Berylls by AlixPartners

While there is great theoretical potential in SSBs, we believe the industry is still five to 10 years from a commercially viable product. For OEMs considering how, or indeed whether, to invest in the battery technology, Berylls’ solution is to take a three-pronged approach, made up of a 360-degree partnership assessment, tech and competitor benchmarking, and strategy development.

Berylls’ partnership assessment takes a 360-degree view of selected dimensions, including value creation and risk management to quantify performance levels, thus revealing strengths, weaknesses and potential for optimization. The key goal is to identify and make transparent the gaps in partnership and collaboration approach to build the foundation of a sustainable improvement program.

Technology and competitor benchmarking uses Berylls’ comprehensive quantitative and qualitative datasets as the basis for customized and expanded assessments of how peers are performing in specific SSB use cases.Our proprietary database continuously tracks more than 3,000 startups and scaleups across the mobility value chain, including around 250 battery-related companies and around 50 automotive SSB startups and scaleups.These are technology-based profiles, including KPIs for battery energy density and charging cycle efficiency, as well as our proprietary research insights into industry claims.

Our standardized strategy development process then uses the results of the partnership assessment and benchmarking, combined with comprehensive internal and external analysis, to define and implement a data-backed strategy. It takes in future customers, competencies, and strategic direction to set automakers on the best path forward.

To discuss your solid-state battery ambitions with our team, please contact Dr. Alexander Timmer.

¹ Joint study conducted by Berylls by AlixPartners and PEM Motion

NO TIME TO READ THIS WEBSITE?