WANT TO DISCOVER MORE?

SEARCH

he year 2023 was characterized by changes in the automotive industry.

While numerous new suppliers and OEMs are trying to gain a foothold, the established OEMs are fighting for their position and strug- gling with their strategic realignment.

A high interest rate environment and low consumer spending due to the high inflation period suggest that 2024 will be another subdued year. Geopolitical tensions and disruptions in supply chains continue to prevent a sigh of relief.

Download the full insight now!

Dr. Jan Burgard

Dr. Jan Burgard (1973) is CEO of Berylls Group, an international group of companies providing professional services to the automotive industry.

His responsibilities include accelerating the transformation of luxury and premium OEMs, with a particular focus on digitalization, big data, connectivity and artificial intelligence. Dr. Jan Burgard is also responsible for the implementation of digital products at Berylls and is a proven expert for the Chinese market.

Dr. Jan Burgard started his career at the investment bank MAN GROUP in New York. He developed a passion for the automotive industry during stopovers at an American consultancy and as manager at a German premium manufacturer. In October 2011, he became a founding partner of Berylls Strategy Advisors. The top management consultancy was the origin of today’s Group and continues to be the professional nucleus of the Group.

After studying business administration and economics, he earned his doctorate with a thesis on virtual product development in the automotive industry.

Malte Broxtermann

Malte is an expert in the development and implementation of automotive digitization strategies.

He focuses on helping clients scale (generative) artificial intelligence to improve their bottom line across the entire automotive value chain. His primary customers are automotive manufacturers and their suppliers, especially those active in the Software-Defined-Vehicle space.

Before his time at Berylls by AlixPartners (formerly Berylls Strategy Advisors), he advised leading North American utility companies. Prior to that, he saved lives as emergency medical technician. Malte holds master’s degrees in economics from Maastricht University and Queen’s University in Canada.

he automotive industry is in the midst of immense transformation, affecting all departments and established industry mechanisms.

As part of that, sales and marketing functions are undergoing a huge shift toward a direct retail sales model.

Download the full insight now.

Jonas Wagner

Jonas Wagner, born in 1978, is a Partner and Managing Director of Berylls by AlixPartners (formerly Berylls Mad Media). With around 20 years of consulting experience in the automotive industry, Jonas is a trusted advisor for top management, specializing in strategy, organizational development and large transformation programs for leading, global automotive manufacturers.

Jonas excels in guiding automotive companies through the transformation of their sales and marketing functions. He has a proven track record in digitalizing customer interfaces to enhance customer experience, sales conversion and loyalty. His expertise includes introducing and implementing new sales and business models tailored to the evolving market landscape and developing data-driven sales and marketing organizations to optimize performance and efficiency. His expertise includes all on- and offline touchpoints as well as business segments, ranging from sales, after-sales, financial services to new business models.

Before joining Berylls, Jonas was a leading consultant within the Automotive Practise of Oliver Wyman, where he worked with global automotive manufacturers, enhancing their strategic initiatives and operations.

Jonas holds a degree in Business Administration from the Aarhus School of Business and the University of Mannheim, with a focus on International Management, Marketing, and Controlling. Combining deep industry knowledge with strategic acumen, Jonas Wagner is a valuable partner for automotive leaders navigating complex transformations.

Theresa Stütz

Theresa Stütz (1991) joined Berylls Strategy Advisors in December 2017. Meanwhile she is associate partner and automotive downstream expert.

She has been advising automotive manufacturers in a global context both in the luxury and premium segment. She has in-depth expert knowledge in the areas of sales and marketing, particularly in the context of customer experience strategies. Other areas of expertise include strategy development processes, Go-to-market strategies and transformation management.

Theresa received both Bachelor and Master of Science in Management and Technology (Mechanical Engineering) at Technical University of Munich.

ow OEMs successfully navigate an insecure environment with volatile incentives and reluctant customers as well as retailers.

In 2024, the automotive industry is supposed to be at the tipping point of the transformation to the battery electric vehicle (BEV). This paradigm shift is exemplified by the imminent launch of over 50 new battery electric vehicle models in Germany alone, coupled with more than 15 Chinese brands operating in the fiercely competitive European market.

But will the shift happen, or will it be dismissed? The dramatic drop of BEV sales in December 2023 (compared with 2022), shows clear signals of a weakening commitment and volatile demand. So how do you navigate through this difficult time without wasting effort and budget?

Download the full insight now!

Jonas Wagner

Jonas Wagner, born in 1978, is a Partner and Managing Director of Berylls by AlixPartners (formerly Berylls Mad Media). With around 20 years of consulting experience in the automotive industry, Jonas is a trusted advisor for top management, specializing in strategy, organizational development and large transformation programs for leading, global automotive manufacturers.

Jonas excels in guiding automotive companies through the transformation of their sales and marketing functions. He has a proven track record in digitalizing customer interfaces to enhance customer experience, sales conversion and loyalty. His expertise includes introducing and implementing new sales and business models tailored to the evolving market landscape and developing data-driven sales and marketing organizations to optimize performance and efficiency. His expertise includes all on- and offline touchpoints as well as business segments, ranging from sales, after-sales, financial services to new business models.

Before joining Berylls, Jonas was a leading consultant within the Automotive Practise of Oliver Wyman, where he worked with global automotive manufacturers, enhancing their strategic initiatives and operations.

Jonas holds a degree in Business Administration from the Aarhus School of Business and the University of Mannheim, with a focus on International Management, Marketing, and Controlling. Combining deep industry knowledge with strategic acumen, Jonas Wagner is a valuable partner for automotive leaders navigating complex transformations.

Sascha Kurth

Sascha Kurth (1987) is a Partner at Berylls by AlixPartners (formerly Berylls Mad Media), a company specializing in the automotive industry. He is an expert in building, transforming, and restructuring sales and marketing organizations and has experience from more than 30 projects in this context. From his perspective, it is particularly important for sales and marketing organizations to have clear and measurable goals and a clear and comprehensible strategy for achieving them. Subsequently, the focus is on creating an effective, efficient, and self-optimizing organization from the right people, processes, partners, and necessary governance. Technology and data are crucial enablers for leveraging the efficiency and effectiveness of the resources used multiple times. This is essential to be competitive, remain competitive, and develop competitive advantages for the future. However, they are not an end in themselves but always enablers to achieve the goals (better). Sascha Kurth is convinced that building effective and efficient sales and marketing organizations is a crucial long-term competitive advantage for the entire company and that paid advertising (especially increasing the budget) should be one of the last initiatives to achieve strategic goals.

Sascha Kurth has been supporting automotive manufacturers in a global context since 2013. He has extensive expertise in goal-oriented sales and marketing planning, Paid, Earned, Owned- funnel management, data management platforms & customer data platforms, e-commerce platforms, programmatic advertising, customer relation management, smart KPIs, and management dashboards.

Prior to joining Berylls Mad Media, he supported leading OEMs, e-mobility start-ups, telecommunications companies, and fast-moving consumer goods manufacturers in their sales & marketing transformation at various consulting firms.

ncertain demand in a weak economy, a mix of powertrains, skills shortages and the influence of subsidies are making network design more important - and more complex

Automotive suppliers and OEMS are being forced to make hard decisions about their production networks, as they focus on efficiencies and protecting margins in an uncertain economy. Existing footprints are also being challenged by the electric vehicle (EV) transition, sustainability requirements, new skills needs and more political influence in the form of national subsidy programs.

Supplier ZF Friedrichshafen, for example, announced plans in January to close two plants in Germany with the intention of moving production to lower-cost locations in eastern Europe or India, and the future of Audi’s plant in Brussels is in doubt, according to multiple news reports. At the same time, Chinese EV maker BYD is building its first European factory in Hungary, which has a growing car battery industry.

Footprint decisions for suppliers are always complex because of the high costs involved – particularly after the rise in interest rates from years of historic lows – and the social and political impact of closures and job losses. But the range of current considerations, including the impact of generous new EV subsidies in the US under the Inflation Reduction Act, are making the process even more challenging.

Here we look at how suppliers can asses their overall network capacity in light of current and future market demands, to align with their strategic objectives.

Suppliers currently face complex additional footprint considerations, the first of which is undoubtedly politics. Governments are exerting more influence over where OEMs and suppliers locate production than they have done for a number of years, as national subsidy programs linked to the EV transition significantly affect the business case for factory locations.

The biggest is the US Inflation Reduction Act (IRA), signed into law by President Joe Biden in 2022. The IRA promises $433 billion of investments in the US economy, of which $369 billion are for energy security and climate change. The measures that directly affect the auto industry include tax incentives for consumers to buy EVs and grants to retrofit factories for low-emissions vehicle production. However, the subsidies only apply to EVs that are made with a proportion of materials that are sourced in the US or countries with US free trade agreements, such as Japan. The proportion was 30% in 2023, rising to 80% by 2027.

The earlier Bipartisan Infratsructure Law, signed in 2021, also awarded $6 billion of grants for companies investing in battery manufacturing and components.

The intention of the legislation is to build up the US’s domestic battery and EV production and reduce reliance on Chinese components, and the result is that OEMs and suppliers will have to move production to the US in order to sell EVs and components there.

We believe the effect on the automototive labor market will go beyond job losses in Europe and Asia if new factories are located or older ones re-located to the US. Tech talent is also likely to move to the US, because subsidies are focused on future clean technologies, and innovation will go with them. This will cause Europe to lose further ground against the US.

This is not to say Europe is stepping back from the race to build up its EV and battery production capacity. EU member states made €6.1bn available to support battery innovation and production through two Important Projects of Common European Interest (IPCEI) agreed in 2019 and 2021. There are no restrictions on the origin of the raw materials for batteries, in order to build up production of EVs and battery cells in the region.

From 2026, the European Union’s Carbon Border Adjustment Mechanism (CBAM) means companies will have to pay for certificates to cover the cost of emissions created during the production of goods they import, making low-carbon local production sites more financially attractive.

There are also EU subsidies available to build up manufacturing in less wealthy parts of the bloc such as eastern Europe. Building new plants with the latest automation and digital production tools will increase efficiency and likely will cost less than modernizing an existing production site. The cost advantage will be a strong factor in suppliers’ footprint decisions.

Beyond politics, new types of workforce considerations are also now affecting footprint decisions. The first issue is the availability of people with the right skills: new, highly digitalized and automated factories need workers with a broad range of technology skills, including engineering, computer science, robotics and experience with artificial intelligence (AI). Creative problem-solving by humans will become increasingly important as routine production tasks are taken over by machines, and we see a growing need for hybrid experts, who combine technical skills with creativity.

We expect a significant impact on traditional factory job profiles as a result of increased digitization and automation, especially at the operational level in factories making lower-cost, mass-produced models (we define these as volume or variant champions here). We see the number of shopfloor logistics roles declining by 63% in volume champion sites and 56% at variant champions’ plants by 2035 while the number of factory operator roles will shrink by 53% and 40% respectively, and the number of line managers by 24% in both types of factories.

In their place, we see high demand for new job profiles as the use of smart machines increases, and databases and data flow become more important. The number of data engineer roles is expected to increase by 78% in volume champion factories and 98% in variant champions’ sites, for example.

For employers, recruiting people to fill these roles will be highly competitive because their skills are in short supply across all manufacturing sectors. Suppliers will need to adjust wages accordingly and offer additional benefits to attract skilled staff to their production sites. The location of plants will become increasingly important – factories close to existing tech or automotive hubs, for example, may find it easier to hire the talent they need.

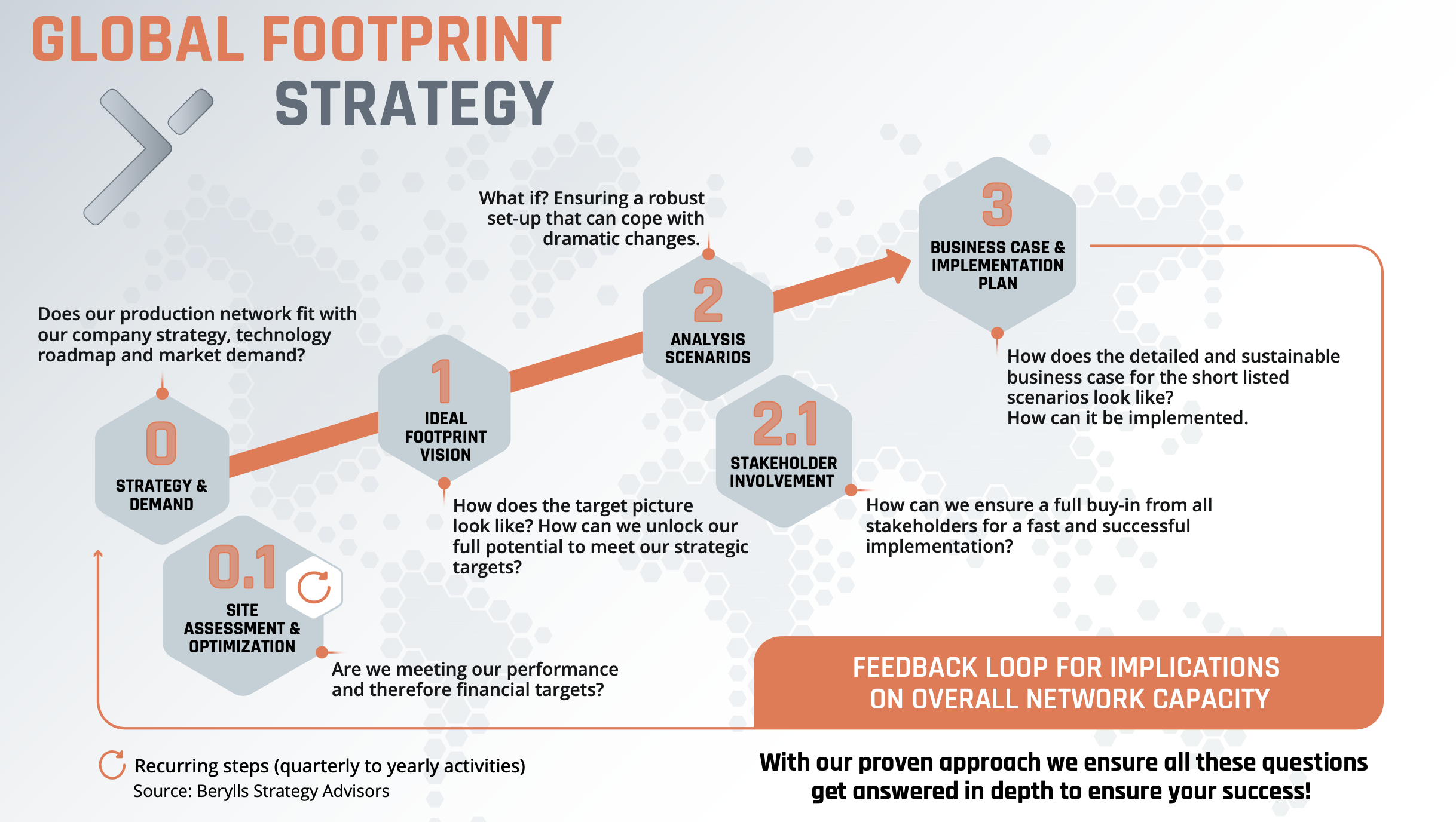

Figure 1: Global Footprint Strategy

Source: Berylls Strategy Advisors

Looking in detail now at a typical supplier’s footprint decision process (see chart above), the first step has not changed despite the complex new challenges described above. Footprint decisions need to be aligned with the company’s strategic objectives, and whether the current network meets them. How is demand expected to develop in different markets and can production sites adapt?

The next step is 360-degree site assessments of performance, cost structure and capacity, to give transparency over each production site’s future potential and improvement opportunities.

Suppliers can then shape the ideal future footprint, defining the plant archetypes and logistics networks they will need. These become the guiding concepts for scenario analysis, that will cover each of the major areas that would be impacted by a change in footprint: cost; the potential effect of subsidies and other government initiatives; the supply chain and logistics network; regulatory compliance; environmental impact; technology and innovation; human resources, and risk assessment.

The evaluated scenarios are narrowed down to a shortlist for evaluation by a wider group of stakeholders, and the final stage is a business case calulation on the short-listed network options, before moving into implementation planning and final decision-making.

Footprint decisions are among the most crucial that any auto supplier will make. The right production network is a critical part of the long-term financial and non-financial success of the company: new production facilities are very expensive, but so is keeping under-used or inefficient sites open. The impact of the investment decision, good or bad, will be felt by the company for years.

Cost efficiency is still a top priority for any footprint decision, but after a period of time in which the auto industry has been hit with one crisis after another, resilience is now ranked just as highly. Important production network considerations to reduce complexity and increase flexibility can include building factories close to customers to reduce the chance of supply chain disruption, and ensuring sites are located in places where there are enough skilled staff, or that are attractive to new hires.

Sustainability throughout the supply chain is also a key consideration for OEMs, and suppliers must be able to ensure their production locations meet customer and regulatory ESG requirements.

And as described above, the auto industry has become a key part of many governments’ industrial policy as they seek to meet commitments to transform their economies. Striking the balance between the short-term benefits of subsidies and the long-term results of choosing a particular location is now an important part of the footprint decision-making process. Some uncertainty is inevitable, as for example in the US where the outcome of the presidential election in November may change the position on EV subsidies.

However, what suppliers can do is make a thorough assessment of their product portfolio and expected future market demands, and consider the results alongside subsidy benefits, to see whether government support makes entering a new market worthwhile. They should also consider how reliant their product portfolio is on subsidies, and how that impacts their production network flexibility.

All these factors – cost, resilience, sustainability and subsidies – deserve thorough consideration in footprint decision-making, to reduce the risk inherent to such large and long-lasting decisions.

At Berylls, we have worked with clients on production network strategy and supply chain design for years, building up deep expertise in defining the right criteria and evaluations for your company’s footprint decisions. We would be delighted to discuss this or any other aspect of manufacturing footprint with you.

Christian Grimmelt

Christian Grimmelt has been an integral member of the Berylls by AlixPartners (formerly Berylls Strategy Advisors) team since February 2021. Previously, he gained extensive professional experience in top management consultancies and in the automotive supplier industry.

During his time at the world’s largest automotive supplier, he drove the establishment of a central unit to optimize the company’s global logistics and production network.

Christian Grimmelt’s consulting focus is logistics and production network optimization, purchasing and (digital) operations including launch and turnaround management for OEMs and especially suppliers.

Christian Grimmelt holds a university diploma in industrial engineering from the Karlsruhe Institute of Technology.

ometimes, the automotive industry tends to use military terminology. Understandably, this is typically the case when the stakes are high and time is running out. Task forces are a prime example of this phenomenon.

Usually, they are formed when there is a risk of a production shutdown with high follow-up costs or when development and industrialization projects fail to reach their milestones. Mechanisms are then set in motion that are common practice and pathbreaking to achieve the desired results. How do these mechanisms work? Where in the company can they still be deployed with success and what are their restrictions? And why are they unavoidable, despite every effort?

A task force is formed when a specific problem needs to be resolved within a very short time and a great deal of money is at stake. On the one hand, there are requirements and performance indicators regarding deadlines, costs, and quality to be considered and, on the other hand, a team of experts that has been put together on a temporary basis. The attentive reader might possibly recognize that this description comes very close to the definition of a “project.”

HOWEVER, THERE ARE SEVERAL SIGNIFICANT DIFFERENCES TO A NORMAL PROJECT:

Basically, it’s already too late for the solution

A lot of time and money has already been squandered. Preventive measures have failed, and the effort is mainly about damage limitation. The goal seems unattainable – and yet it must be pursued by all means

Every day costs money

When it comes to delivery bottlenecks, for example, every minute of lost time can be measured directly in lost profitability per component and ultimately per vehicle. The pressure on the people involved can become unbearable.

The problem is incredibly complex

Open heart surgery is required. Every change to the strained system can cause effects that need to be considered in advance and no single process can simply be changed separately. Every measure needs to be scrutinized in terms of success, failure, and unintended side effects. Often a few simple, clearly communicated, aligned (de-escalation) targets are needed to help resolve the situation.

A task force has a prior history of escalation

The nerves of those involved are frayed, several attempts have already been made to solve the problem, personal careers are at stake, and trust has been undermined. On the one hand, a speedy and structured problem-solving is often hampered by the personal and political tactics employed by those involved, while on the other hand, the process tends to be fraught with nervousness and hectic activities. Calm, fact-based communication and effective leadership are often simply disregarded.

The markets are unforgiving

A delayed product launch goes hand in hand with the scheduling of new model series and always involves a considerable loss of profit and reputational damage. As a result, sales, controlling, and marketing teams understandably have limited patience for those in development, production, and the supply chain who are constantly striving to catch up on milestones and performance indicators. The pressure, therefore, is sizzling, demanding tangible signs of progress each day. These factors alone are a clear indication that a task force needs to operate with a variety of specific project management tools.

Task forces are like agile project management on steroids

The timing is very tight. The daily schedule starts in the early morning for the team with the daily check-in and ends with the daily check-out. In between, the agreed measures need to be rigorously implemented – independently and without lengthy committee meetings. Success, therefore, greatly depends on nominating the right team members. The right experts need to be integrated and the team spirit must be sound, regardless of the organization and job title, whether OEM, supplier, or consultant. In the end, the integrated efforts of those involved make all the difference.

Discipline and a keen focus on suction are basic requirements

It sounds so simple but is unfortunately not always given that scheduled agreements are adhered to. Unforeseen obstacles must be communicated and resolved immediately as they arise and not only when someone fails to provide the agreed result.

The structure of a task force covers the entire range of solutions and usually consists of several work packages. When setting up the work packages, it is important not only to address the obvious topics (e.g. “OEE increase”), but also to work on the underlying causes (e.g. “strategic resource management”). When forming the team, it should be borne in mind that everyone involved must actively collaborate and be aligned with the overarching goal as defined and guided by the higher management. It is key to manage interdependencies between work packages within the Task Force Team on a regular basis and with mutual support. This combination is the only way to solve acute problems and at the same time create a robust system.

Each measure must have verifiable objectives

In addition to precisely documenting each defined measure, it goes without saying that feedback on completion is provided at the agreed due date. Another decisive factor for ensuring success is the prior linking of the measures with the expected impact on a targeted key performance indicator. This requires some effort and practice but leads to two elementary effects: a) A measure without a defined outcome will simply not be implemented, as it would be wasteful. b) A measure with a defined outcome is then not only reviewed regarding implementation, but also for the fulfillment of the expected outcome.

Task forces align with and follow higher management

There is no time for committee meetings and long decision-making processes. In a task force, serious decisions sometimes need to be made several times a day. Depending on the size of the company, the uppermost hierarchical levels need to be either directly involved on a daily basis or at least accessible. If they are not directly involved, decisions must be prepared precisely with the necessary information and clearly communicated. The required effort should not be underestimated and must be prepared in parallel to the technical work. However, the power of facts is there to override political controversies.

Empathy and emotional intelligence are critical success factors

This point may sound surprising, given that task force situations are connected to a military style of communication. Ultimately, the personalities involved need to be understood and positively motivated. This requires an excellent understanding of the respective situation and motives for action by the task force leadership and the consultants involved.

However, a sustainable improvement of the situation can only be achieved if people act intrinsically different afterwards, a fact that also highlights the limitations of task forces in general, as they only work effectively within a clearly defined timeline and organizational framework. The preceding paragraphs clearly illustrate the significant pressure on the people involved, leading to long-term sustainability concerns. The usual organizational and operational structures are also temporarily insignificant. Sooner or later, the situation must be transitioned back to a robust and efficient disciplinary line management system.

For this reason, every good task force needs to prepare its own end from scratch

Criteria for de-escalation must be clearly and transparently defined. Embedded in an overarching schedule, they must be regularly communicated and not subject to change. Once the targets have been achieved, the task force is no longer required. The criteria therefore need to be defined so that a return to normal working mode within robust processes is subsequently possible. The combination of deliberately defined work packages and criteria for their de-escalation therefore determines the subsequent sustainability of the success right from the start.

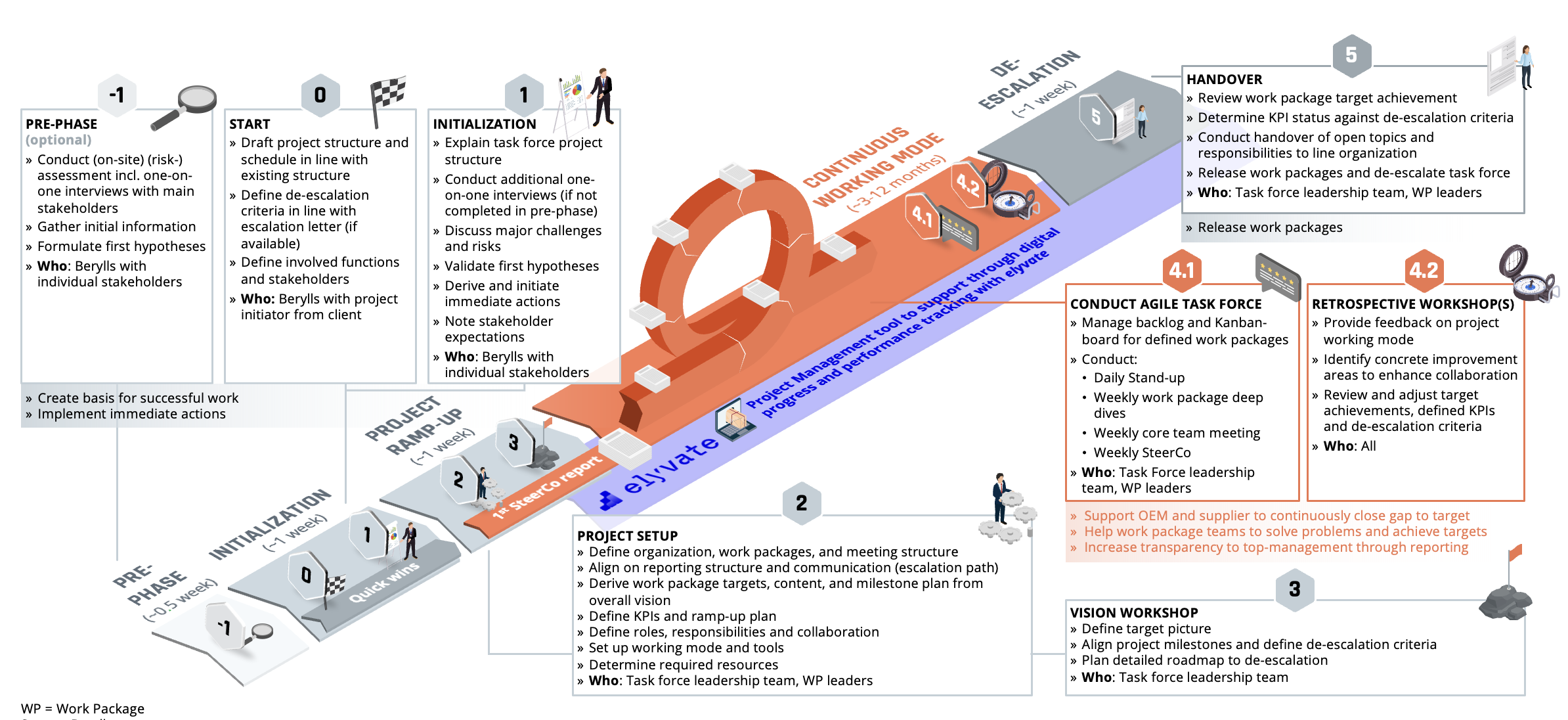

We at Berylls have spent decades honing our expertise in mastering task forces within the operations environment. The focus in terms of content has increasingly shifted towards e-mobility components but is not limited to this field alone. The task force life cycle we have developed as a result is a unique approach that incorporates all the success factors mentioned above:

Figure 1: The Berylls task force life cycle

Source: Berylls

Pronounced for us was the successful transfer of experience from more than 100 successful de-escalated task force projects to enable early escalation preventive programs in future development and production planning. This is where our tried and tested Safe Launch System Certificate comes into play, which certifies that suppliers and OEMs have their development, industrialization and launch management processes under control.

But we wouldn’t be “but dyfferent” if we didn’t go one step further with our clients. When it comes to monitoring and controlling a task force, we offer our tool called “elyvate”. Our colleague Christian Kaiser has already described the additional use of IT tools and artificial intelligence for efficient support here.

In our following articles, we will also look at how task forces can lead to success, even in a well-oiled marketing machine or a dynamic sales environment. The instruments simply need to be adapted to the respective circumstances. Nevertheless, based on our experience, we strongly advise our clients to have a standardized task force approach as well as management mechanism for early problem identification at hand so that it can be swiftly utilized as and when needed.

Fritz Metzger

Fritz Metzger (1986) joined Berylls by AlixPartners (formerly Berylls Strategy Advisors), an international strategy consultancy specializing in the automotive industry, in February 2021. He is an expert on automotive operations.

Since 2011, his focus has been on strategic alignment and operational efficiency improvement of automotive manufacturers and suppliers. He also advises top management in critical situations, including R&D and industrialization task forces and relocation and restructuring initiatives of plants and complete suppliers. The challenges of e-mobility are always in focus.

Before joining Berylls, he was a director at international strategy consultants PwC Strategy&, as well as a sales and project manager at a medium-sized supplier and mechanical engineering company.

Fritz Metzger is a trained industrial engineer with a degree from ESB Business School Reutlingen. He also holds an MBA from the University of Salzburg.

Heiko Weber

Heiko Weber (1972), Partner at Berylls by AlixPartners (formerly Berylls Strategy Advisors), is an automotive expert in operations.

He started his career at the former DaimlerChrysler AG, where he worked for seven years and was most recently responsible for quality assurance and production of an engine line. Since moving to Management Engineers in 2006, he has been contributing his experience and expertise to projects for automotive manufacturers as well as suppliers in development, purchasing, production and supply chain. Heiko Weber has extensive experience in the development of functional strategies in these areas and also possesses the operational management expertise to promptly catch critical situations in the supply chain through task force operations or to prevent them from occurring in the first place.

As a partner of Management Engineers, he accompanied the firm’s integration first into Booz & Co. and later into PwC Strategy&, where he was most recently responsible for the European automotive business until 2020.

Weber holds a degree in industrial engineering from the Technical University of Berlin and completed semesters abroad at Dublin City University in Marketing and Languages.

he digital revolution is transforming automotive sales and marketing at an accelerating pace as economies bounce back from the pandemic.

Amid the upheaval, the winners will be those players that capture the opportunities created by new, data-driven technologies to improve the customer journey.

Berylls Mad Media has developed a direct-to-consumer sales and marketing approach which we call the “Infinity Loop” to give you a head start over the competition. The loop delivers continuous optimization of the customer journey through constant interaction between data-driven end-to-end (E2E) marketing activities and omni-channel sales.

Time is short. The sales and marketing transformation race is a sprint where the winners will emerge at speed. For this reason, Berylls Infinity Loop leverages five key transformation levers to help you cross the finishing line by 2025.

Discover more in our point of view.

Jonas Wagner

Jonas Wagner, born in 1978, is a Partner and Managing Director of Berylls by AlixPartners (formerly Berylls Mad Media). With around 20 years of consulting experience in the automotive industry, Jonas is a trusted advisor for top management, specializing in strategy, organizational development and large transformation programs for leading, global automotive manufacturers.

Jonas excels in guiding automotive companies through the transformation of their sales and marketing functions. He has a proven track record in digitalizing customer interfaces to enhance customer experience, sales conversion and loyalty. His expertise includes introducing and implementing new sales and business models tailored to the evolving market landscape and developing data-driven sales and marketing organizations to optimize performance and efficiency. His expertise includes all on- and offline touchpoints as well as business segments, ranging from sales, after-sales, financial services to new business models.

Before joining Berylls, Jonas was a leading consultant within the Automotive Practise of Oliver Wyman, where he worked with global automotive manufacturers, enhancing their strategic initiatives and operations.

Jonas holds a degree in Business Administration from the Aarhus School of Business and the University of Mannheim, with a focus on International Management, Marketing, and Controlling. Combining deep industry knowledge with strategic acumen, Jonas Wagner is a valuable partner for automotive leaders navigating complex transformations.

Sascha Kurth

Sascha Kurth (1987) is a Partner at Berylls by AlixPartners (formerly Berylls Mad Media), a company specializing in the automotive industry. He is an expert in building, transforming, and restructuring sales and marketing organizations and has experience from more than 30 projects in this context. From his perspective, it is particularly important for sales and marketing organizations to have clear and measurable goals and a clear and comprehensible strategy for achieving them. Subsequently, the focus is on creating an effective, efficient, and self-optimizing organization from the right people, processes, partners, and necessary governance. Technology and data are crucial enablers for leveraging the efficiency and effectiveness of the resources used multiple times. This is essential to be competitive, remain competitive, and develop competitive advantages for the future. However, they are not an end in themselves but always enablers to achieve the goals (better). Sascha Kurth is convinced that building effective and efficient sales and marketing organizations is a crucial long-term competitive advantage for the entire company and that paid advertising (especially increasing the budget) should be one of the last initiatives to achieve strategic goals.

Sascha Kurth has been supporting automotive manufacturers in a global context since 2013. He has extensive expertise in goal-oriented sales and marketing planning, Paid, Earned, Owned- funnel management, data management platforms & customer data platforms, e-commerce platforms, programmatic advertising, customer relation management, smart KPIs, and management dashboards.

Prior to joining Berylls Mad Media, he supported leading OEMs, e-mobility start-ups, telecommunications companies, and fast-moving consumer goods manufacturers in their sales & marketing transformation at various consulting firms.

ffective Pricing Strategies amidst the Global BEV Price War.

Today, the global automotive industry is faced with an unprecedented realm of pricing challenges characterized by ever escalating price wars that threaten both market stability as well as profitability. In our most recent study, we have analyzed the price developments of the BEV used car market in Europe and its impact on the new car market.

This article will delve deeper into the global trend of falling car prices (new and used) with particular emphasis on effective pricing strategies. Our main aim will be to provide a strong framework for OEMs, captives, leasing companies and everyone involved in car (re-)sale to respond effectively against these price wars using a set of proven levers. We recommend promptly setting up a cross-functional task force to develop and swiftly implement customized pricing strategies suited to different vehicle ranges and models to best profit from the given circumstances during price wars.

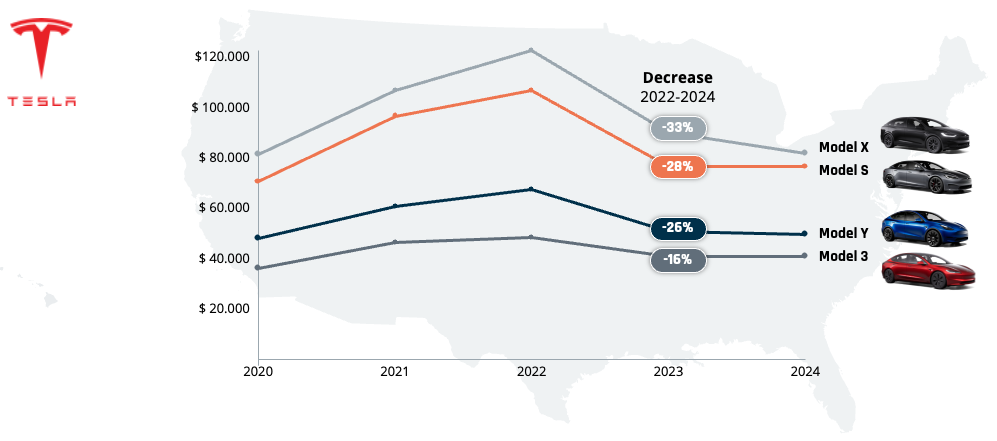

The global automotive industry is at an inflection point where BEV price wars are active across regions. Triggered by the price cuts that Elon Musk does at Tesla and fueled by discontinued subsidies in countries like Germany and France, this price war has reached substantial proportions. Tesla has slashed new car prices for their models between 2022 and today by between 16% (Model 3) and up to 33% (Model X) in the US.

TESLA LIST PRICES SINCE 2020 FOR THE US, IN USD

Source: Berylls Strategy Adivsors, Car and Driver

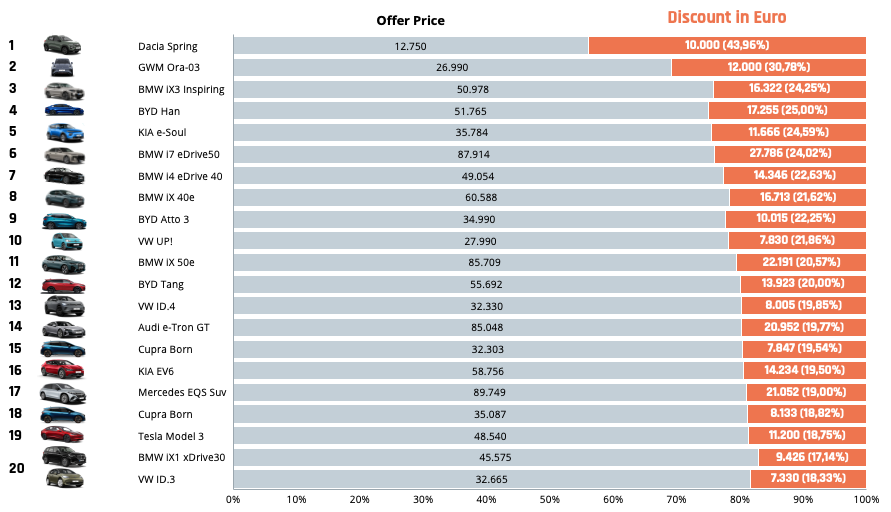

Discounts and price cuts are back! After a longer period of high prices due to demand bottlenecks, BEV discounts are about to become the new normal. This is not affecting single brands or segments but can be observed across the board.

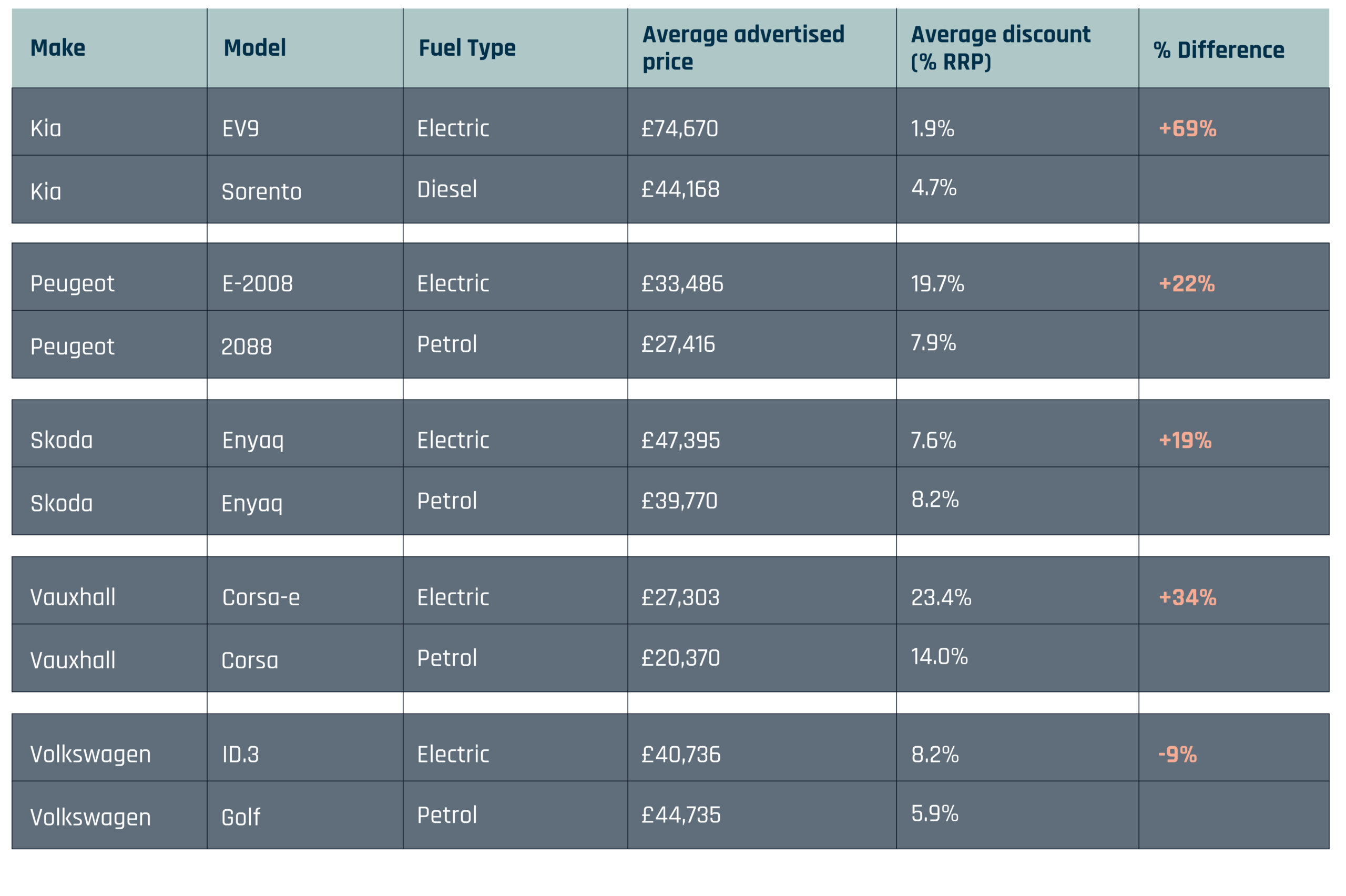

TOP 20 DISCOUNTS BY BRAND AND MODEL

Source: Berylls Strategy Advisors

Once a price war has started, it is obviously difficult to act against or even stop it. The trick is to make the best out of given circumstances short-term and to execute the most effective levers out of the pricing toolbox. By doing so, companies will profit from additional effects on profitability despite the negative effects the price war will have without a doubt.

A price war represents a highly competitive situation in the market. It occurs when a business reduces its prices to attract more customers and increases its market share, leading other competitors to lower their prices as well, to remain competitive.

PRICE WAR – UNDERSTANDING TRAD-OFFS

BEV market is experiencing decreasing prices due to higher sales pressure. The risk of a price war with its vicious cycle is rising. Various opportunities and threats must be traded off precisely by the OEMs.

Source: Berylls Strategy Advisors, Autovista24, part of Autovista Group

Like conflicts among nations, price wars often stem from escalating tensions or significant disparities within the market landscape. The onset of such wars is almost inevitable once these conditions are in place. Price wars do not emerge spontaneously but are the result of various contributing factors and certain triggers:

In industries where a few large corporations dominate, alongside a considerable number of smaller entities, the risk of a price war escalates.

To prevent new competitors from gaining a foothold, existing businesses might reduce their prices, thereby intensifying the competition over pricing.

When consumers frequently switch providers seeking lower prices, companies might engage in fierce price reductions to attract and keep these price-sensitive shoppers.

Overly optimistic growth expectations can prompt managers to compete aggressively for a larger share of the market.

When offerings are seen as similar, there's a higher tendency towards price wars, as with limited options for differentiation, businesses might lean towards cutting prices.

Companies weigh the potential gains from lowering prices against the risk of competitive retaliation. This balance influences whether they decide to lower prices or avoid doing so.

These elements are reliable indicators of the potential for price wars to erupt. In automotive, it is a combination of different triggers, that lead to the current price war. Market concentration is still high, although the number of new OEMs especially from China has considerably lowered it. New entrants are setting new price levels for certain vehicle ranges that are much lower than what was the case before, thereby educating consumers towards low prices. The expectation of high market growth might have influenced the decision of Tesla to lower prices, expecting to gain market share. The same rationale might hold true for especially Chinese manufacturers. Subsidies are being reduced or stopped etc.

Understanding the reasons behind a price war is important as to some extend it influences the possible reactions on the pricing side.

During a price war, businesses often face significant pressure to lower prices to maintain competitiveness, which can lead to a race to the bottom and potentially harm long-term profitability. However, there are several pricing approaches that companies can adopt to navigate through a price war effectively without solely relying on cutting prices.

Choosing the right strategy depends on the company’s market position, product or service offerings, customer base, and overall business goals/ pricing strategy. Before deciding on a set of pricing approaches, the pricing strategy must be clearly defined and the focus on volume vs. margin determined for those products in focus at least.

It’s also crucial to monitor the effectiveness of the chosen strategy and be prepared to adjust as the market conditions change.

Here are the 10 most suitable pricing strategies to use during price wars (of course not only then):

PRICING APPROACHES DURING PRICE WARS

10 most suitable pricing strategies to use during price wars (of course not only then).

Emphasize customer value; justify higher prices for select segments.

Instead of competing on price, focus on the value offered to customers. This involves understanding what aspects of your product or service are valued by your customers and setting prices based on that perceived value. By differentiating your offerings, you can justify maintaining higher prices at least for certain parts of the portfolio and selected customer segments.

Set higher prices for unique features or superior quality.

Maintain a premium pricing strategy for products or services that offer unique features, superior quality, or exclusive benefits not available from competitors. This strategy relies on branding and market positioning to appeal to customers who are willing to pay more for perceived higher value. This can for example be applied to certain accessories or parts of a vehicle range.

Combine products for increased perceived value and sales.

Combine products or services into a package deal at a price lower than the total of each item sold separately. This can increase the perceived value for customers and discourage direct price comparisons with competitors' individual products. Bundling can e.g. be done for cars and service packages (higher margin business).

Temporarily lower prices to gain market share quickly.

Temporarily lowering prices below competitors to gain market share and attract price-sensitive customers. Once a solid customer base is established, prices can be gradually increased. This strategy requires a careful balance to avoid long-term profit erosion. It can make sense in a situation where a bigger cost advantage exists compared to competition.

Price products to cover costs and ensure profit.

Ensure pricing covers costs and includes a margin for profit. This strategy is more about internal cost management than market competition, but it can help avoid selling at a loss during a price war.

Employ tactics to make prices more appealing.

Utilize pricing tactics that make your prices appear more attractive, such as pricing products at $999 instead of $1.000. This can make your offerings seem cheaper without significantly reducing the price. Rounding logics can of course be applied to accessories as well. There are further psychologically driven pricing tactics that can be applied such as “reason discounts”, “prestige prices”, “versioning” etc.

Adjust prices based on real-time market conditions.

Adjust prices in real-time based on market demand, competitor prices, and other external factors. This requires sophisticated pricing algorithms and data analysis but can help you stay competitive without initiating a downward price spiral.

Offer discounted items to attract customers; boost sales of higher-margin products.

Offer one or more products at a loss or very low margin to attract customers into the retail store or onto the platform with the expectation that they will purchase other, higher-margin items.

Retain customers with rewards and incentives.

Implement or use existing programs that reward repeat customers with discounts, exclusive offers, or other perks. This encourages customer retention and can help maintain sales volumes without directly engaging in price cuts.

Lower prices strategically to remain competitive.

Instead of across-the-board price reductions, selectively lower prices on key items that are most sensitive to competition. This can be an effective way to remain competitive on hot-ticket items while maintaining margins on others.

Applying these strategies can be complex as there´s no silver bullet in pricing, but it is rather a combination of different approaches that will lead to success.

Different strategies can be necessary for certain parts of the portfolio as well as for the regions or countries. Products are positioned differently, and the strategy might as well be. The regional focus of pricing strategies as well depends on the targets that should be achieved. Local adaptation of measures such as bundling or psychological pricing must be done because of market and customer habits.

From our many years of experience, there are three main mistakes that companies make during price wars:

1. The “do nothing” mistake: Price wars are an uncomfortable situation for managers. You know that you are losing substantial profit, you cannot really stop the price war, nor do you know when it will end. Quite often the reaction is to try and not make it worse by any actions for which the outcome is unknown. Managers simply sit, observe, and wait until the price war is over.

2. The “we must act not, it is serious” mistake: During price wars, companies start losing profits immediately and the effect is getting bigger every day and week. All reports show negative deviations and pressure will be high for management to act. The pricing function in automotive OEMs, captives, leasing companies etc. is still underdeveloped in many cases. Data and tools are not sufficient, processes rather manual than digital and the like. For price war situations often there´s no toolbox existing, that pricing managers can make use of. The result often is a hectic and not well thought about approach with measures that are more driven by pressure than based on a strategy.

3. The “lone wolf” mistake: Of course, there are people that know what to do or at least believe they do. This sometimes results in isolated measures for e.g. a single product, region, or the like. The problem with this is, that spill-over effects to other products or customer segments are not considered. The complexity of pricing measures is simply underestimated because one is looking at a local optimum. The result can sometimes be the opposite of what you wanted to achieve.

Those mistakes must clearly be avoided and there´s a recipe for how to make sure that price wars are being managed in a positive way.

Pricing task force

In a first step, we recommend businesses to build a pricing task force for the immediate management of counter actions in a price war. Why task force? Because it is necessary to act quickly and involve resources and data from different departments to work systematically and with high pressure to develop and implement solutions. And because a local optimum of one department is often not enough, but a more global optimum is required.

The task force must identify the most important fields in which measures mustbe implemented first. This can be parts of the portfolio, regions, sales channels,or the like. For each priority field, the situation is analyzed, including competitor activities, purchase behavior of clients etc. Based on this, a pricing strategy is developed, considering volume and profitability aspects. Financial targets must be defined, in a worst-, realistic- and best-case scenario. Based on this, a team of experts from different functional areas such as sales, marketing, pricing, financeetc. will develop measures and evaluate their effect before starting to step-by-step implement. Dedicated reports from the markets in focus will make sure that effects in the market become visible and measures can be adjusted accordingly.

Institutionalize

As a second step (or in parallel, depending on resource availability), the taskforce work must be institutionalized. As part of the existing pricing governance and operating model, the necessary elements for price war situations must be added.

The most important elements are to define committees that will be put in placewith a clear governance and a pricing toolbox for the price war situation as well as a dedicated process.

With these two steps, maneuvering through a price war can be done systematically and with maximum impact.

Nota bene: It is obviously the better option to avoid price wars if possible and to make sure that an existing price war can be ended quickly, for example by sending out appropriate communication into the market.

With all these price wars, the global automotive industry is passing through challenging times with threats to decades’ traditional business models. However, with a systematic and comprehensive approach towards pricing and market positioning OEMs, captives, leasing companies and everyone involved in car (re-)sale can ride the tide in these turbulent times. Formulation of a dedicated task force is thus an important first move to make use of data and pool resources across functions to make better and faster decisions and focus on rigid execution.

Thorsten Lips

Thorsten Lips (1972) is a partner at Berylls by AlixPartners (formerly Berylls Strategy Advisors). He began his career as a management consultant at PricewaterhouseCoopers Düsseldorf in 1998. After spending six years at Malik Management Centre in St. Gallen, Switzerland, he took the cross-industry, global responsibility for Pricing, Sales, Service and Marketing as a partner at Horváth. At Berylls, his area of expertise is Pricing & Revenue Management. This encompasses classical topics like new- and used-car pricing, aftersales pricing and the like. In addition, he is an expert in innovative Pricing and Revenue Management approaches for digital products and services as well as in the field of data-driven Pricing.

Industrial engineering and management studies at the Technical University of Ilmenau and the Technical University of Darmstadt.

V STARTUPS ON THE STOCK MARKET – A JUSTIFIED HYPE?

In the last five years, many new EV players entered the stock market. Companies like NIO, Rivian, Lucid, VinFast, and XPENG are among the firms in the hunt for fresh capital to fund their ambitious endeavors. Initially, investors seemed to be on the edge of their seats, eagerly anticipating who was going to follow in the footsteps of EV pioneer Tesla. When Rivian went public at the Nasdaq stock exchange in November 2021, it resonated like an earthquake in automotive circles. At an initial valuation of USD 66.5 bn, they were valued at a similar level to established players Mercedes-Benz and BMW, only two months after producing their first ever customer-ready car.

However, despite this initial hype around newly emerging EV players, the recent performance of Rivian and its EV-peers on the stock market is quite underwhelming. While the rise of new electric vehicle manufacturers seemed very attractive for investors from the get-go, popular companies like Rivian, Lucid or Fisker are currently valued at less than 20% of their initial valuation. This underperformance of many emerging BEV players on the stock market raises question marks. Was the hype around EV startup stocks justified?

Download the full insight now!

Dr. Jan Burgard

Dr. Jan Burgard (1973) is CEO of Berylls Group, an international group of companies providing professional services to the automotive industry.

His responsibilities include accelerating the transformation of luxury and premium OEMs, with a particular focus on digitalization, big data, connectivity and artificial intelligence. Dr. Jan Burgard is also responsible for the implementation of digital products at Berylls and is a proven expert for the Chinese market.

Dr. Jan Burgard started his career at the investment bank MAN GROUP in New York. He developed a passion for the automotive industry during stopovers at an American consultancy and as manager at a German premium manufacturer. In October 2011, he became a founding partner of Berylls Strategy Advisors. The top management consultancy was the origin of today’s Group and continues to be the professional nucleus of the Group.

After studying business administration and economics, he earned his doctorate with a thesis on virtual product development in the automotive industry.

Arthur Kipferler

Arthur Kipferler (1963) started his career in 1989 at the Boston Consulting Group, where he consulted for 13 years in the automotive industry. After consulting, Arthur Kipferler held senior management positions at Toyota in Europe and the U.S. From 2013 to 2014, he was global head of the BMW Group’s Future Retail program. Subsequently, he had leading roles in strategy, corporate planning and transformation management at Jaguar Land Rover in Coventry, UK. Arthur Kipferler complements the expertise of the Berylls by AlixPartners (formerly Berylls Strategy Advisors) partner team in the fields of market & customer, technologies, sales, and digitalization, as well as in the development and implementation of corporate, product, and regional strategies.

Mechanical engineering, production engineering, at the Technical University of Munich (TUM); MBA in Strategy, Marketing and Organizational Behavior at INSEAD Business School, France.

Malte Broxtermann

Malte is an expert in the development and implementation of automotive digitization strategies.

He focuses on helping clients scale (generative) artificial intelligence to improve their bottom line across the entire automotive value chain. His primary customers are automotive manufacturers and their suppliers, especially those active in the Software-Defined-Vehicle space.

Before his time at Berylls by AlixPartners (formerly Berylls Strategy Advisors), he advised leading North American utility companies. Prior to that, he saved lives as emergency medical technician. Malte holds master’s degrees in economics from Maastricht University and Queen’s University in Canada.

UROPEAN POLICYMAKERS DEFINE ELECTRIC MOBILITY AS THE FUTURE.

Governments in Europe unanimously share the vision that electrifying the vehicle fleet is the best way to achieve a more sustainable future. With its new regulation, which states that from 2035 all new cars and vans registered will have to be zero-emission versions, the European Union is a global front-runner in the adoption of electric vehicles.

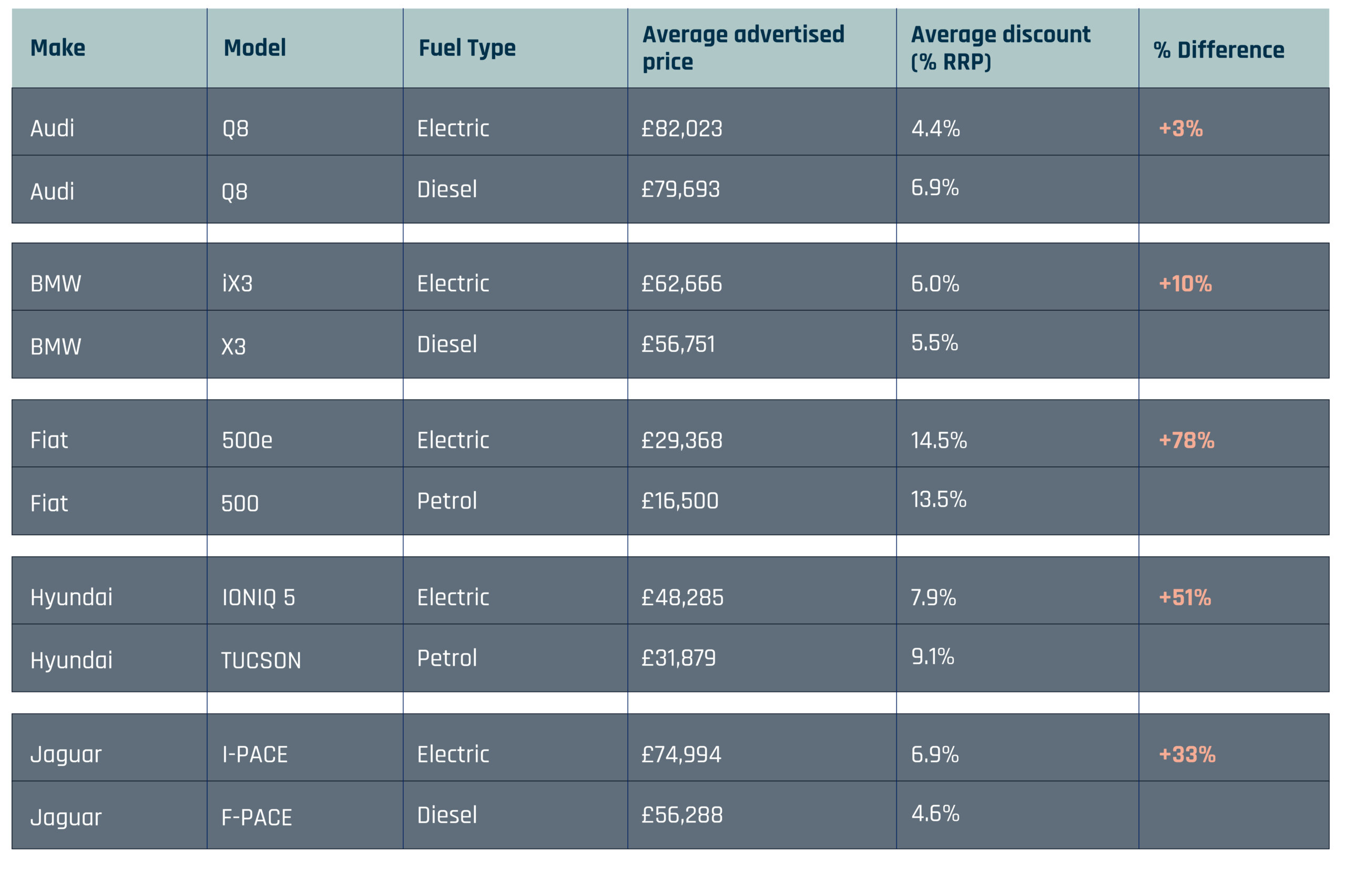

However, this places OEMs under a lot of pressure to update their vehicle portfolio within a relatively short time span. In order to maintain a profitable business case, nearly all OEMs initially focused on producing rather pricy high-end SUVs. Cost parity between comparable new BEV and ICE vehicles has still not been achieved in most cases and, in particular, affordable vehicles in the smaller segments are yet to be launched. For instance, FIAT is offering the electrified version of its 500 with a premium of 78% and even Jaguar’s high-end SUV F-Pace is one third cheaper than its electrified brother (according to UK list prices). This pricing policy limits the overall size of the potential buyer group and prevents the BEV market from moving from early adopters to the mass market.

Source: AutoTrader as of 17.01.2024

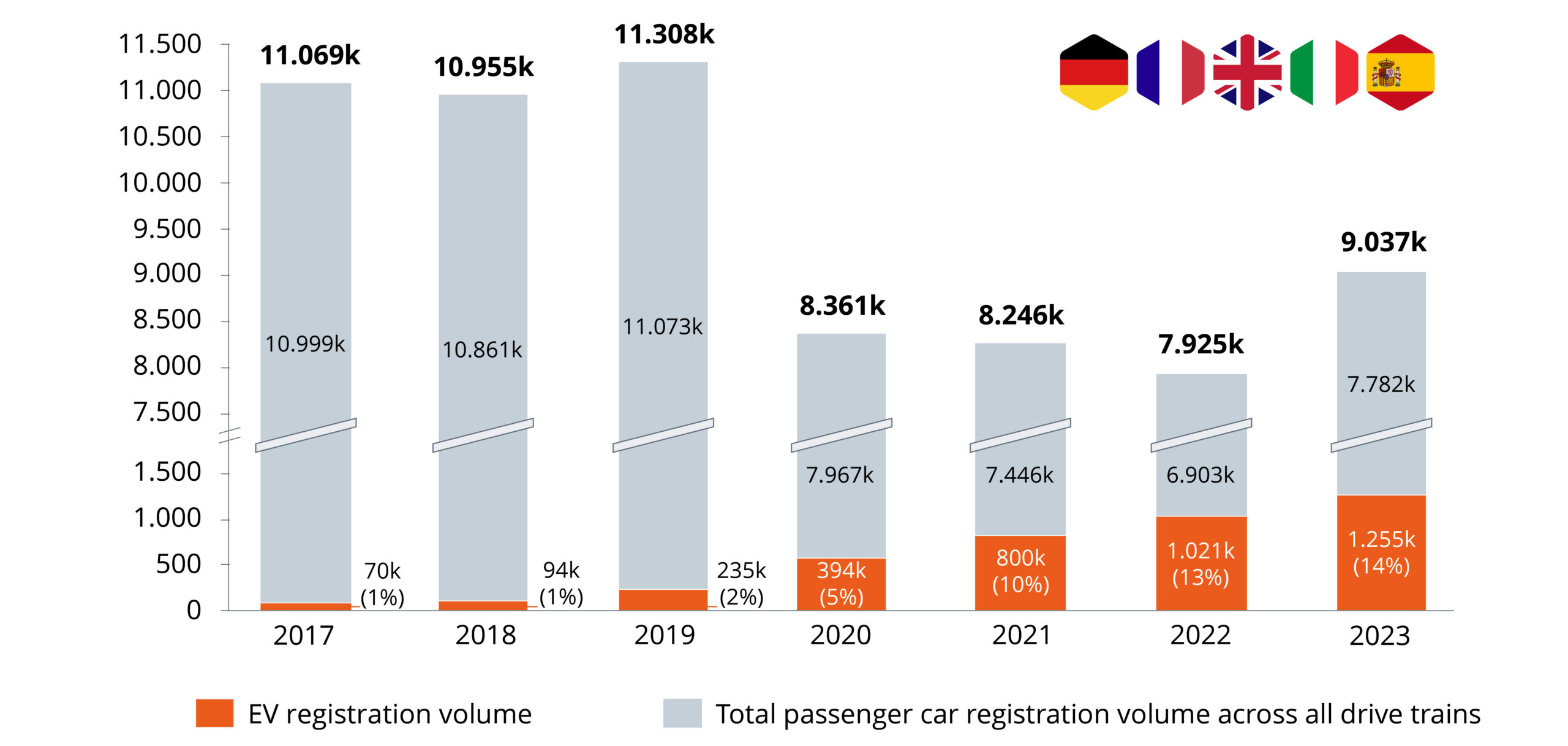

After some initial strong growth – also fueled by high government tax incentive schemes – the relative market share growth of battery electric vehicles (BEVs) is gradually slowing down across Europe.

TOTAL PASSENGER CAR REGISTRATION VOLUME EU5

Increasing relative share of BEV in EU5 registration volume (2017-2023), (registered cars in thousands)

Source: Berylls Strategy Advisors, ACEA

Whilst the share of BEV registrations across all drivetrain types is steadily increasing for the top 5 EU markets (14% in 2023), the momentum of growth is slowing down (+23% in 2023 vs. +103% in 2021 for the top 5 EU markets). BEV customer subsidies are being increasingly reduced in many EU markets (e.g., subsidies for corporate and private cars in Germany were terminated at the end of 2023).

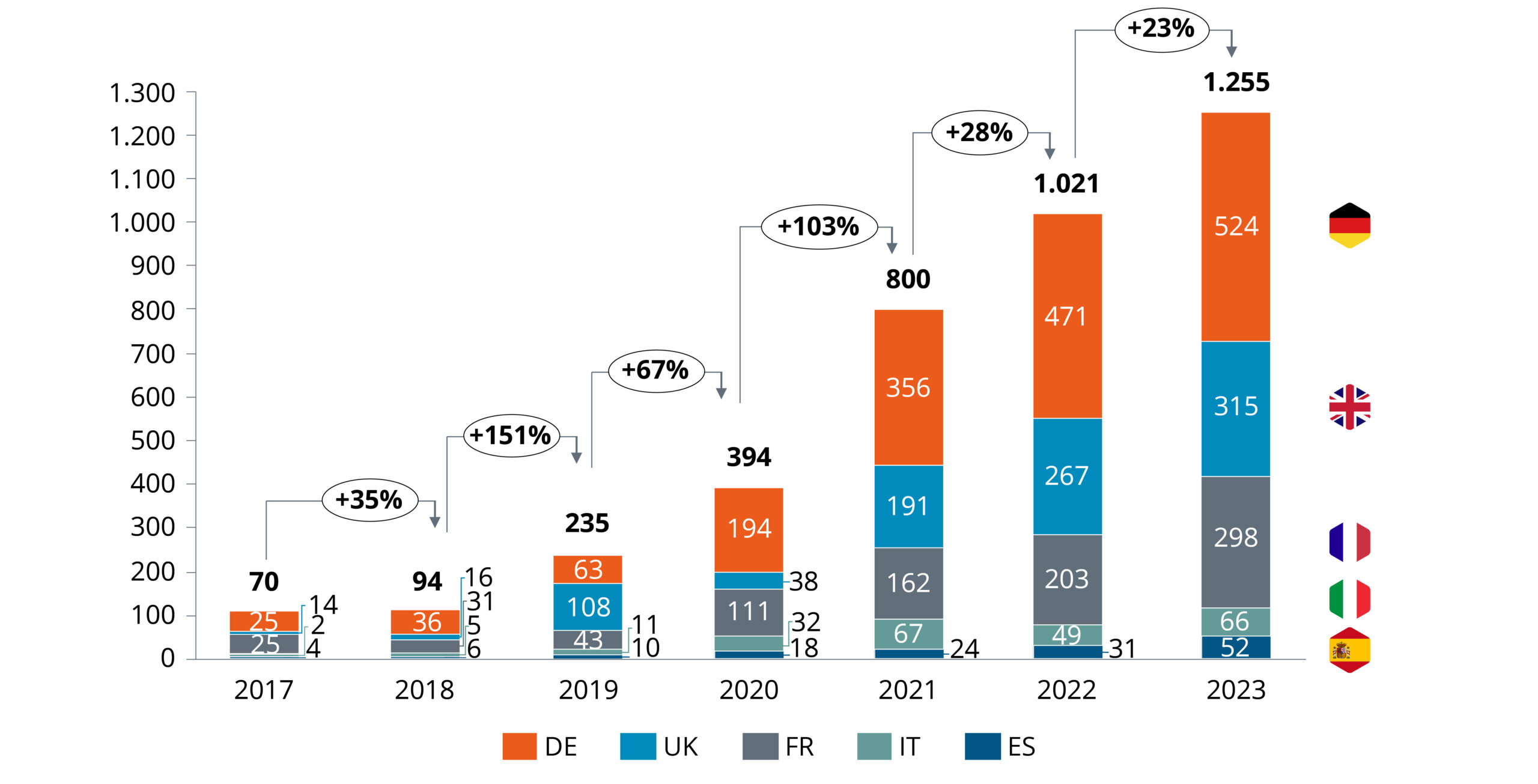

BEV PASSENGER CAR REGISTRATION VOLUME PER EU5 MARKET

Increasing size of registered BEVs in EU5 (2017-2023), (registered cars in thousands)

Source: Berylls Strategy Advisors, ACEA

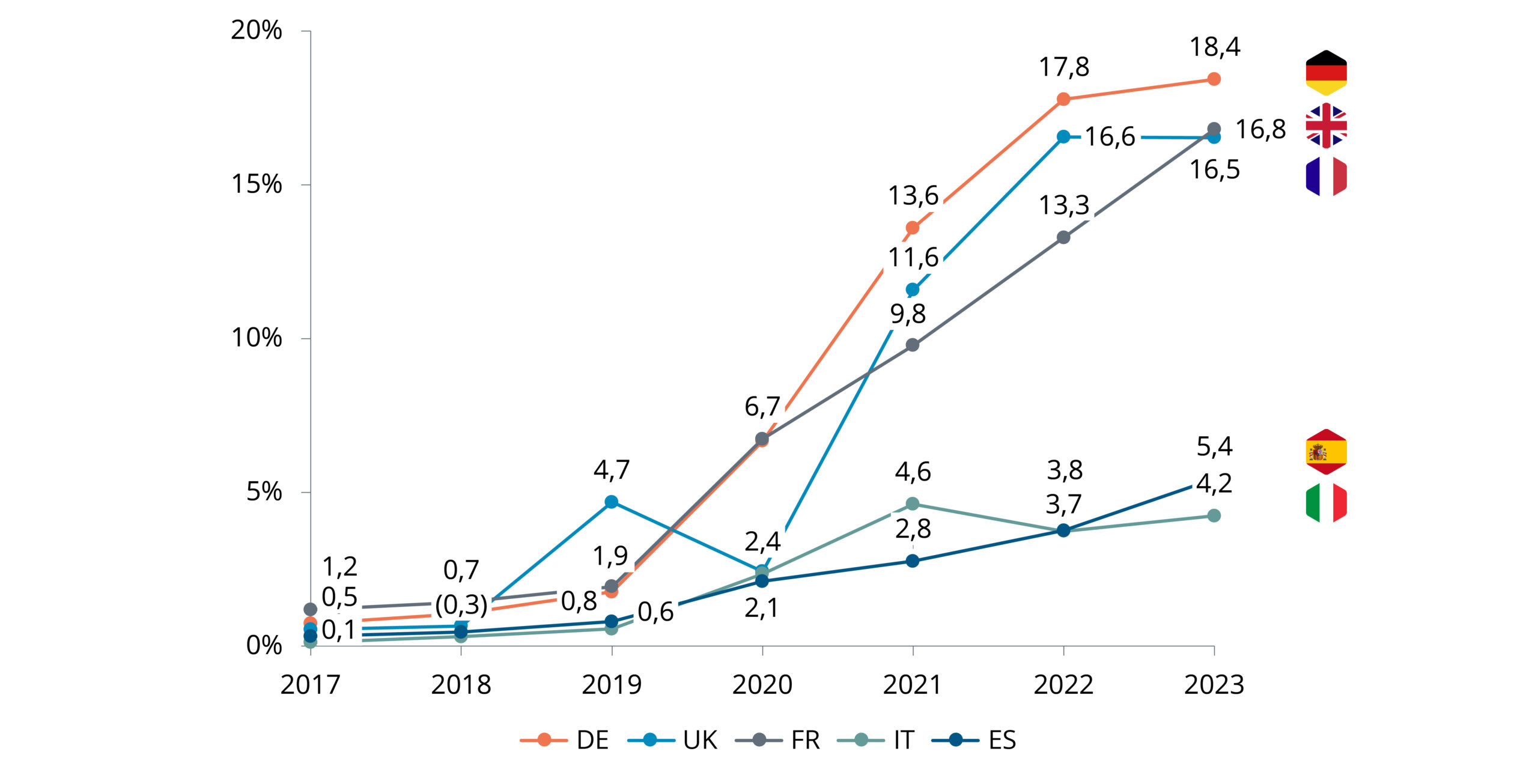

BEV PASSENGER CAR REGISTRATION SHARE PER EU5 MARKET

Increasing relative share of BEVs per EU5 market registration volume (2017-2023), (all figures in %)

Source: Berylls Strategy Advisors, ACEA

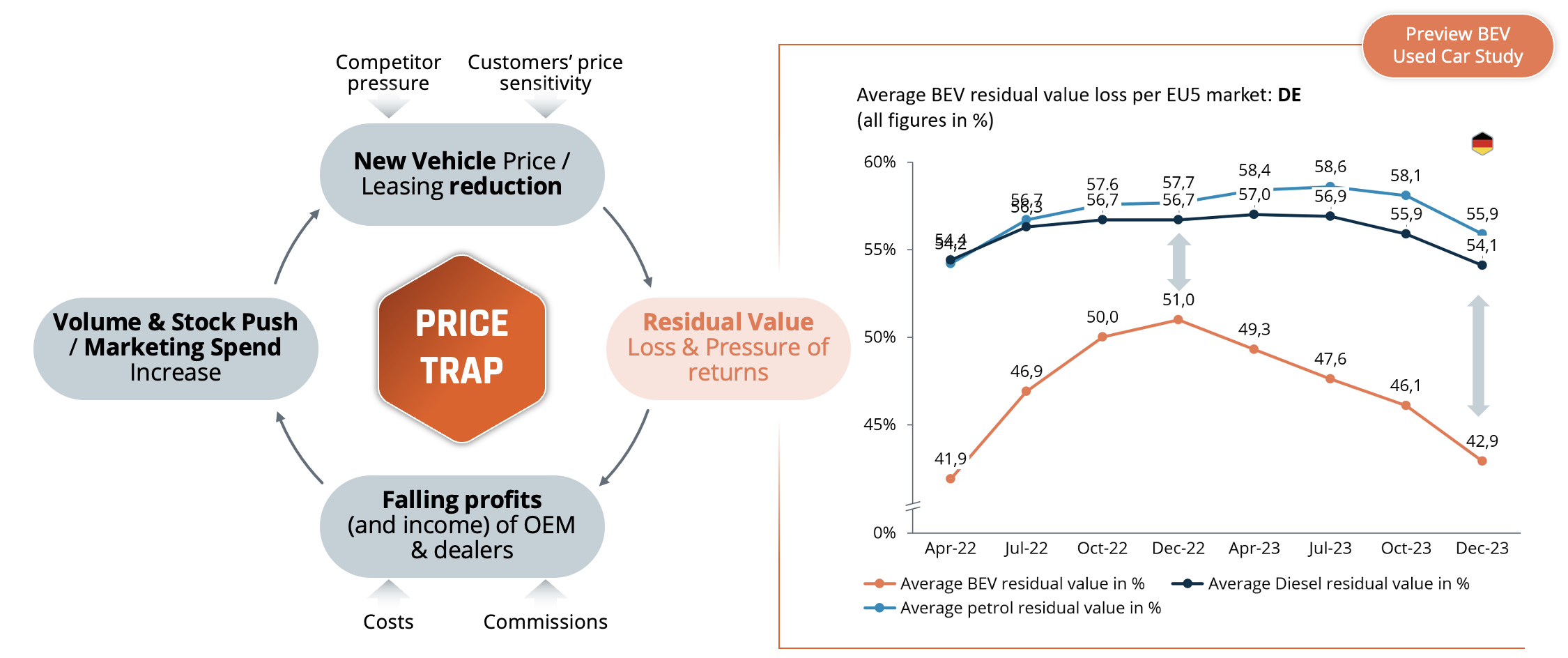

We identify the BEV used car market as one of the key reasons for this slowdown, combined with affordability issues due to challenging economic conditions with high interest rates.

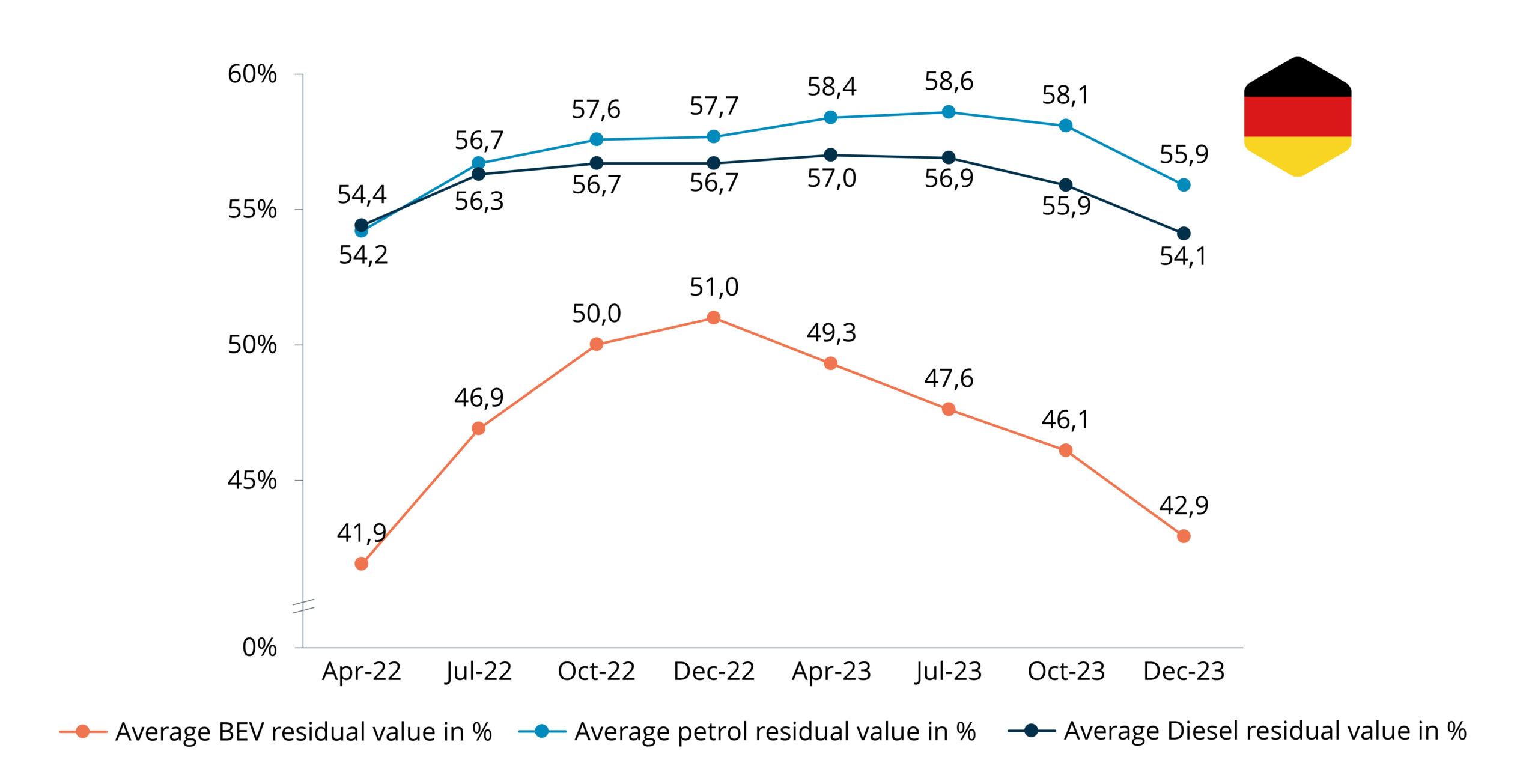

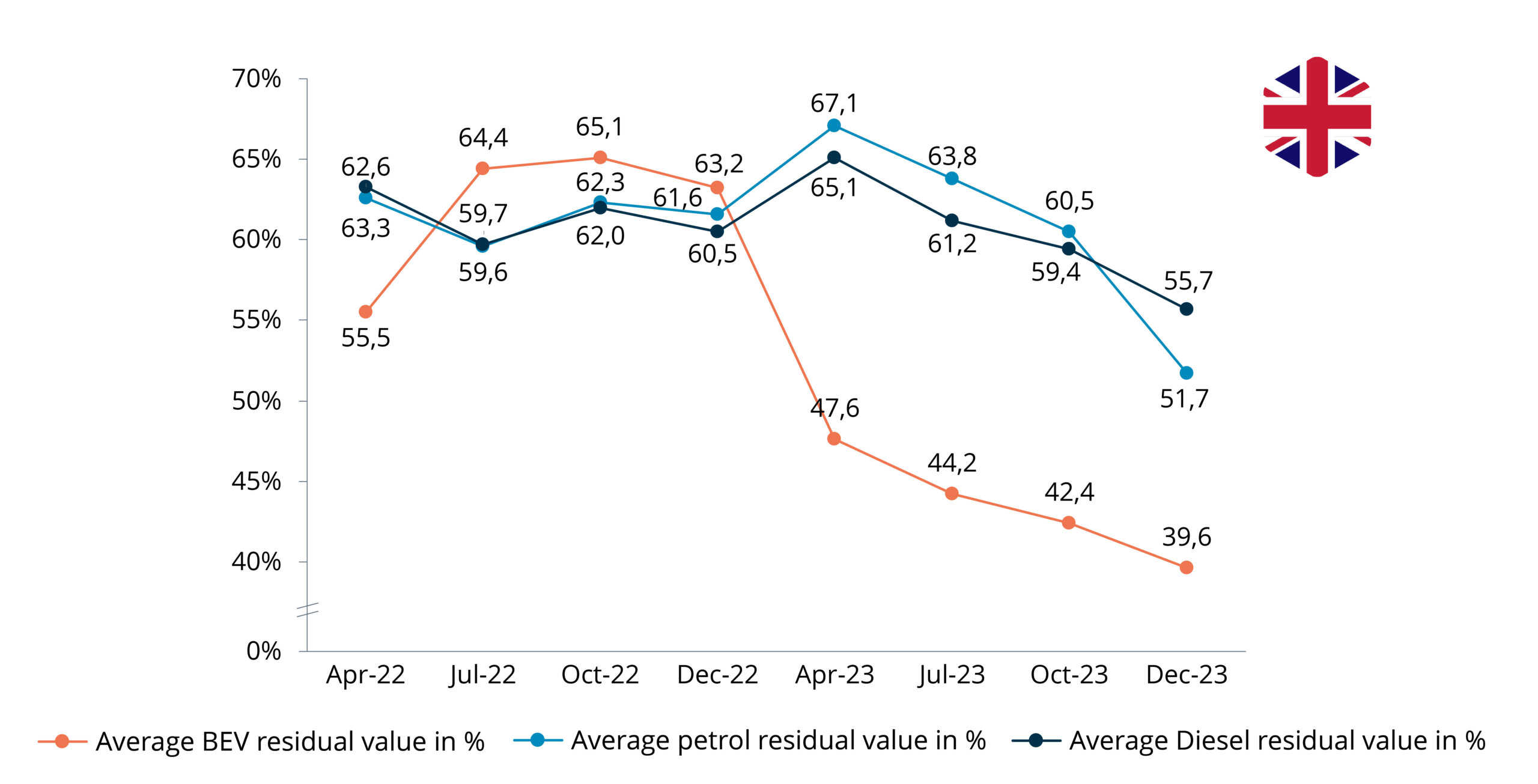

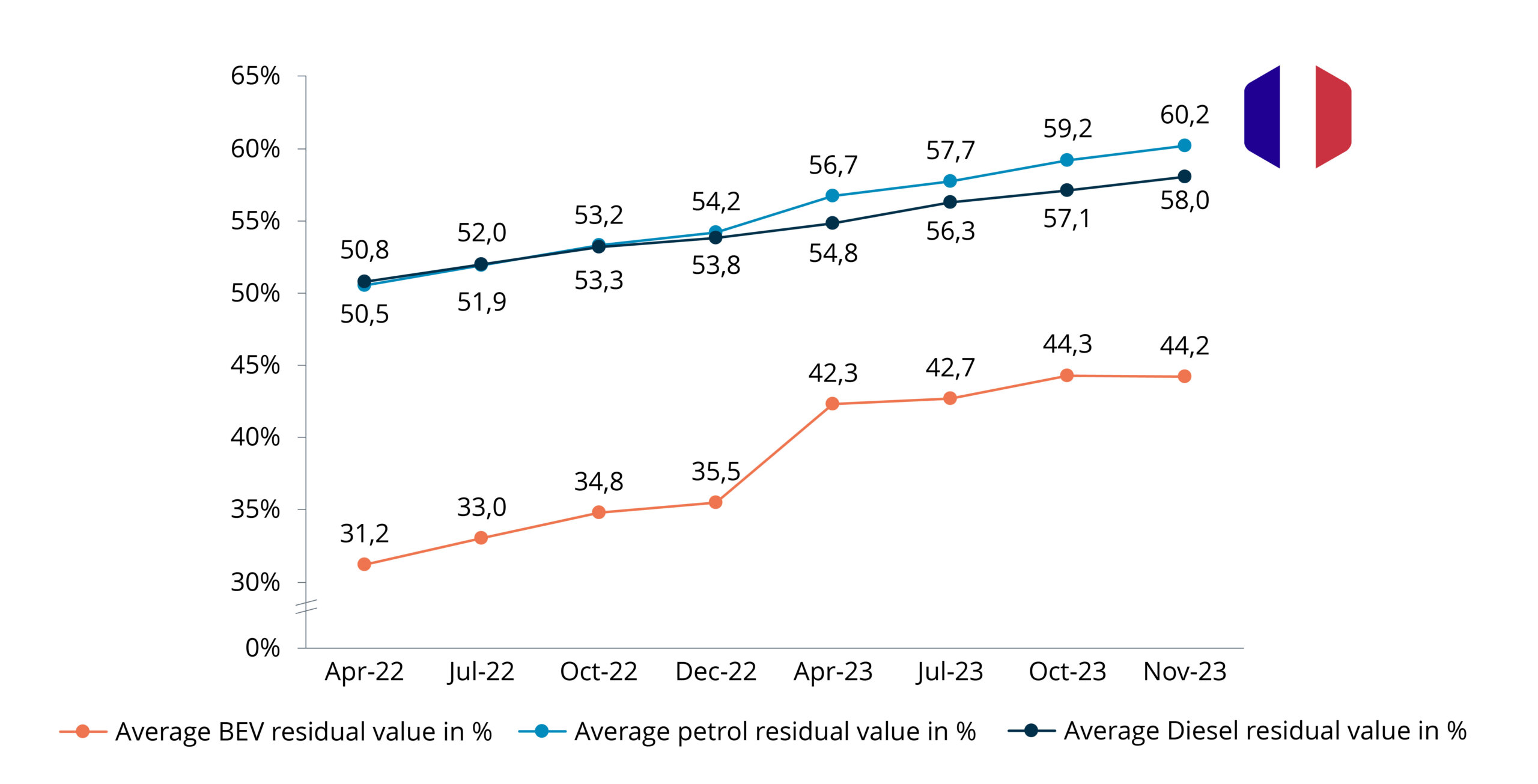

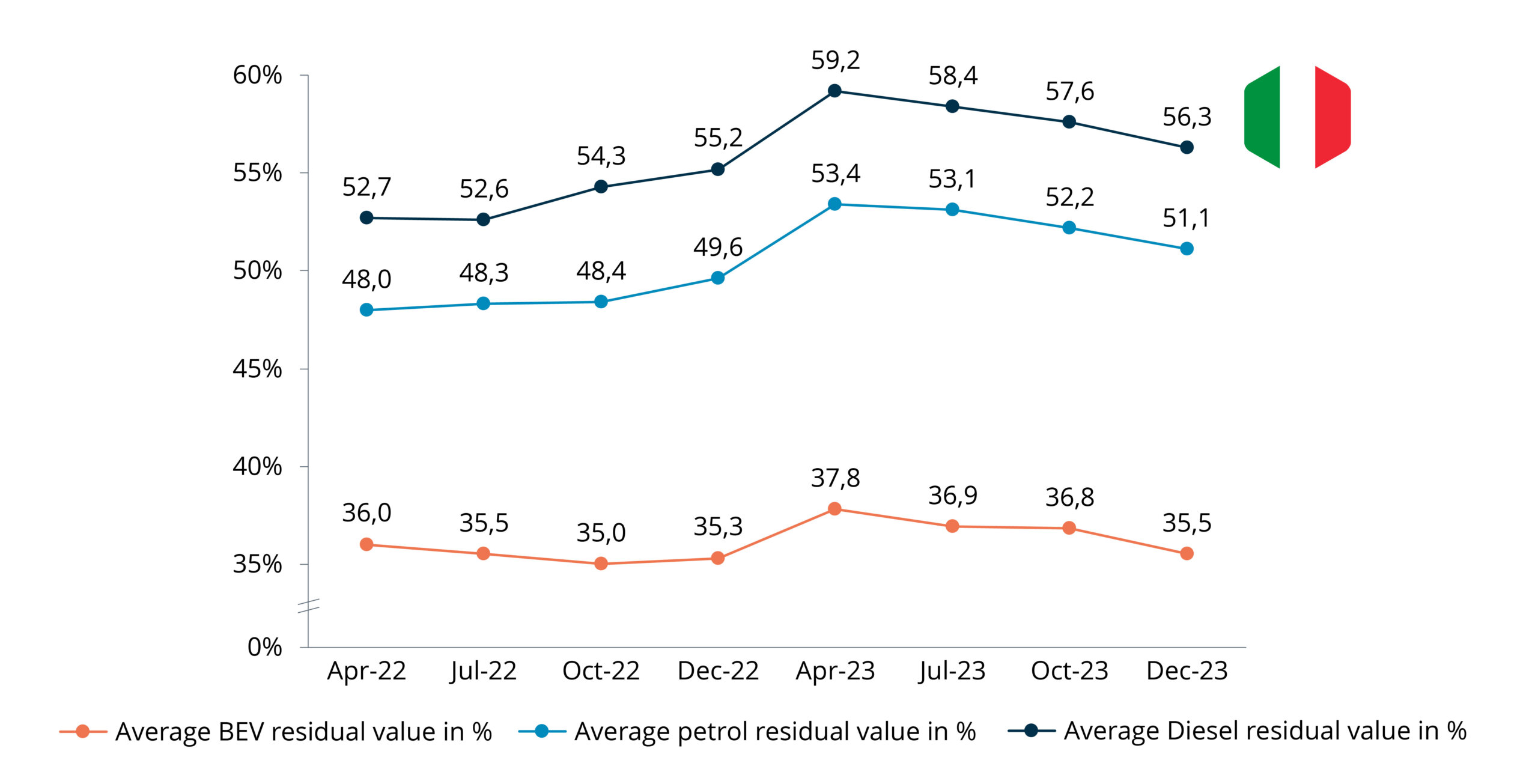

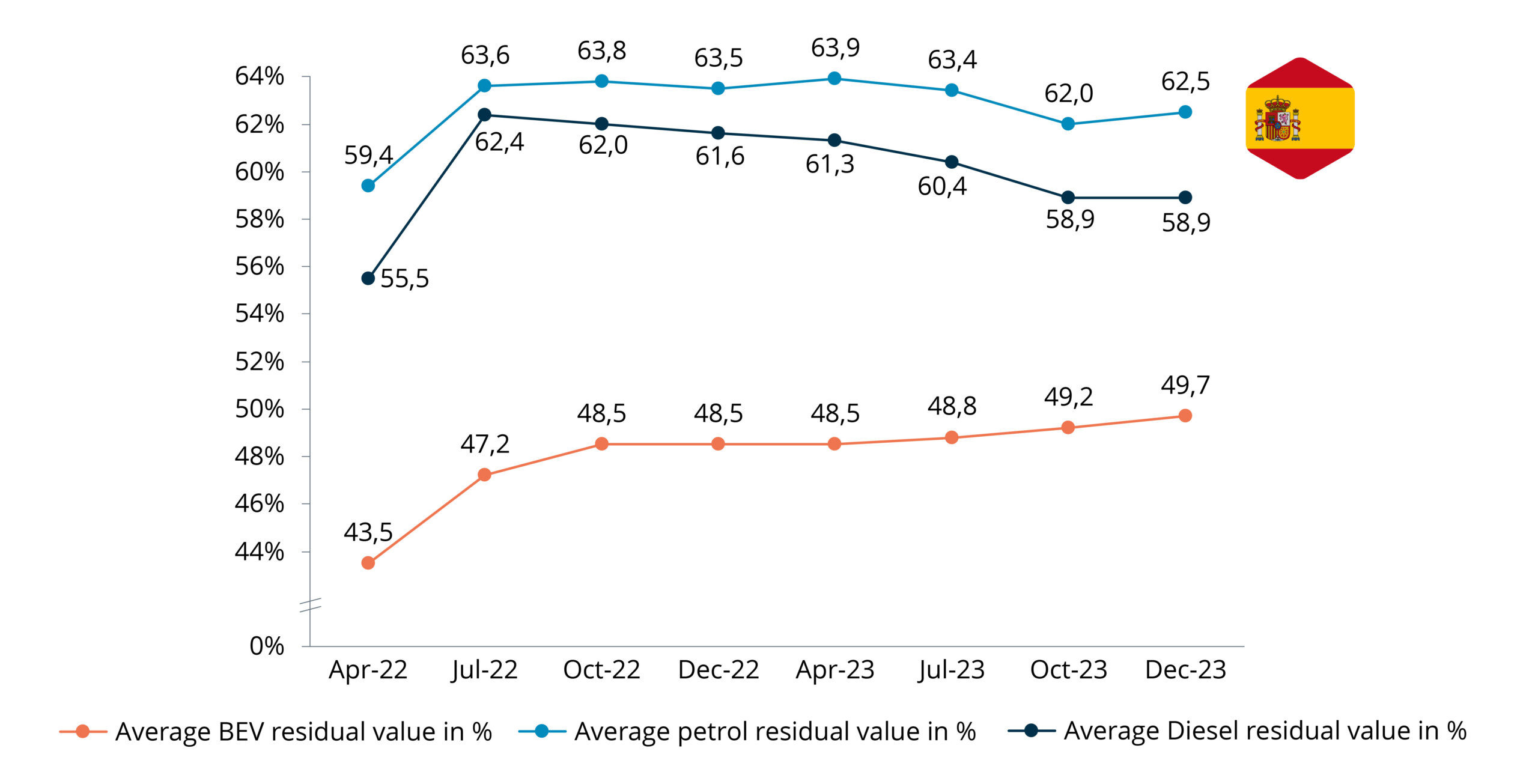

Used BEVs are performing significantly worse than ICEs throughout top European markets with regard to their residual values. On average across Europe, more than 50% of the initial value is lost after an average of three years and 60,000 kilometers.

RESIDUAL VALUE PER DRIVE TRAIN

Comparison of residual values along drive trains (BEV, Diesel, petrol), (all figures in %)

Source: Berylls Strategy Advisors, Autovista24, part of the Autovista Group

The situation is leading to a significant excess value loss for BEVs compared to ICEs, especially when factoring in the higher initial new car prices of BEVs.

In Germany, on average BEVs had an excess residual value loss of 13% compared to petrol vehicles in December 2023. The rest of Europe’s top 5 markets displayed similar tendencies with excess residual value losses ranging from 13% (Spain) to 21% (Italy) when comparing BEVs to petrol vehicles. Apart from Spain and France, used cars in all top 5 European markets have lost drastically in residual value. In the UK, the residual value of BEVs plummeted dramatically from 63% to 40% in the course of 2023.

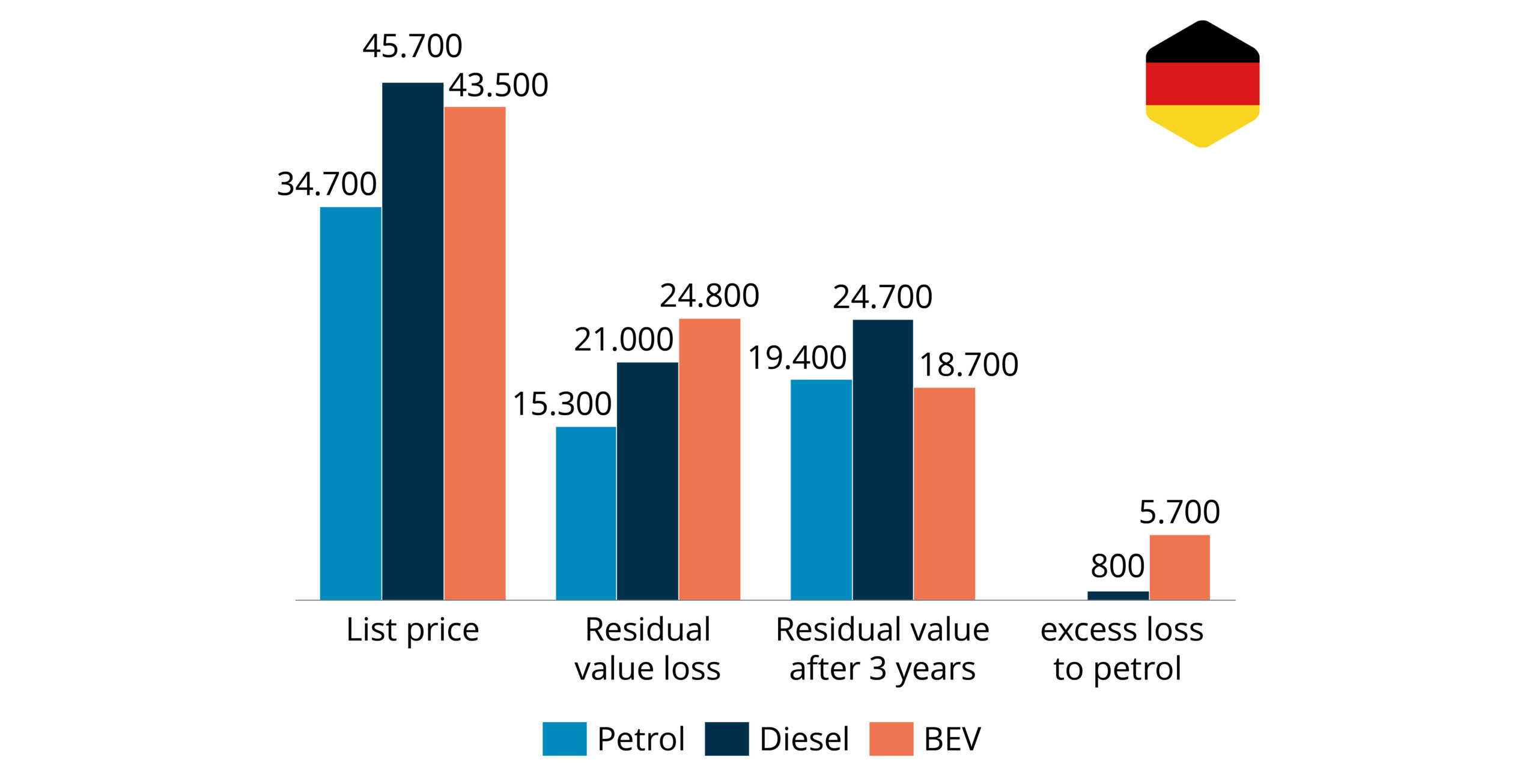

Based on an average new BEV list price of EUR 43,529 as stated by Autovista Group for Germany in December 2023, the absolute amount of excess loss of an average BEV compared to an average petrol vehicle is 13%, which equals EUR 5,659 compared to the initial list price. Looking at a 36-month lease contract with a total of 60,000 km, this would make a BEV EUR 157 more expensive per month compared to a petrol car, just to cover the excess loss and excluding interest effects, in addition to the higher lease installments due to the higher list price.

Likewise, lower residual values also affect new car lease contracts, as providers will try to pass on higher depreciation to their customers. An analysis conducted by Transport & Environment in 2023 reveals that across major European markets, leasing companies charged consumers 57% more to lease an EV compared to an equivalent petrol model.

RESIDUAL VALUE PER DRIVE TRAIN AND EXCESS LOSS IN COMPARISON TO PETROL

Comparison of residual values per car of BEV vs. Petrol and Diesel in DE, (rounded figures, December 2023)

Source: Berylls Strategy Advisors, Autovista24, part of the Autovista Group

The calculation is even more alarming when the initial incentives funded by taxpayers’ money are also taken into account. The current market & technology immaturity is turning out to be a gigantic value burn.

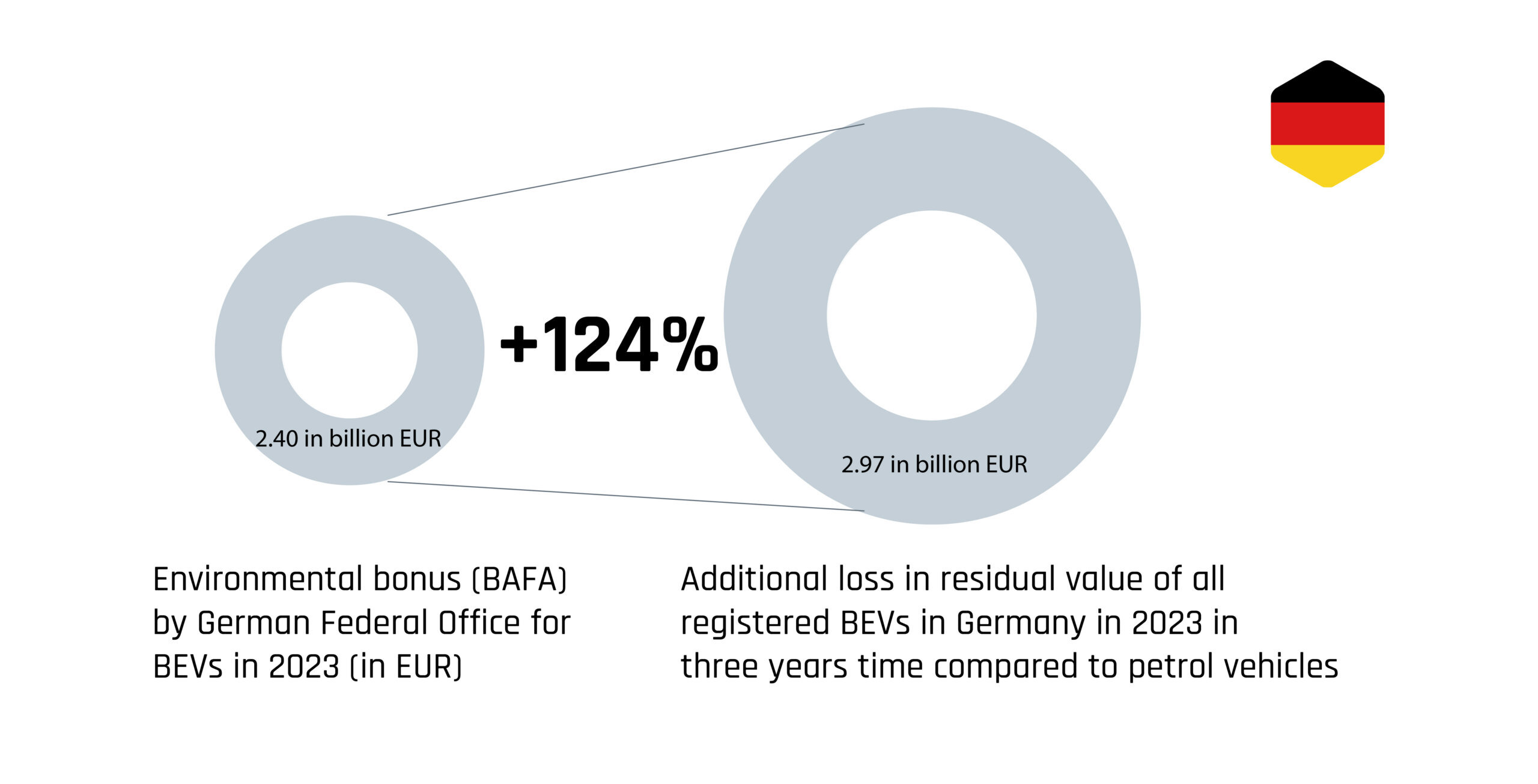

Just assuming the gap between the residual value developments of BEVs and petrol vehicles remains constant in the future, the additional value loss of all the 524,000 BEVs registered in Germany in 2023 in three years’ time compared to petrol vehicles will equal EUR 2.99 billion. The figure surpasses the total of German BEV tax incentives (BAFA environmental bonus) of EUR 2.4 billion for all eligible BEVs in 2023.

COMPARISON OF LOSS IN RESIDUAL VALUE FOR BEVS AND SUBSIDIES IN GERMANY

Excess in loss in residual value of BEVs outpaces environmental bonus in DE in 2023

Note: Excess in residual value loss as aggregation of excess loss of residual value per BEV to petrol (13%) of 524.000 registered BEVs at avg. list price of 43.529 EUR in 2023 in Germany

Source: Berylls Strategy Advisors, Autovista24, part of the Autovista Group

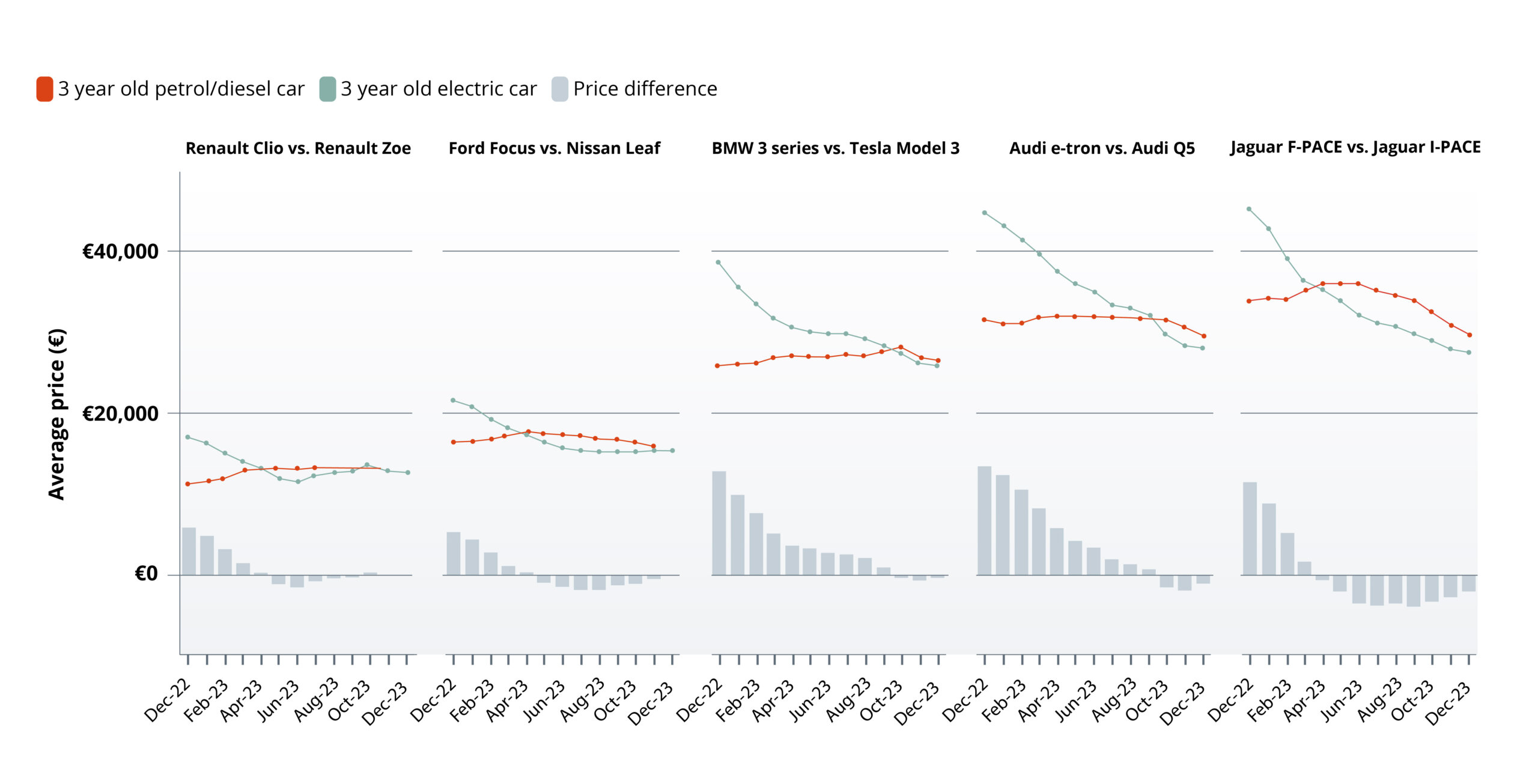

The value losses become even more apparent when comparing the residual values of similar BEV and ICE models:

Upfront price difference based on stock advertised on AutoTrader.co.uk

Source: autotrader.co.uk

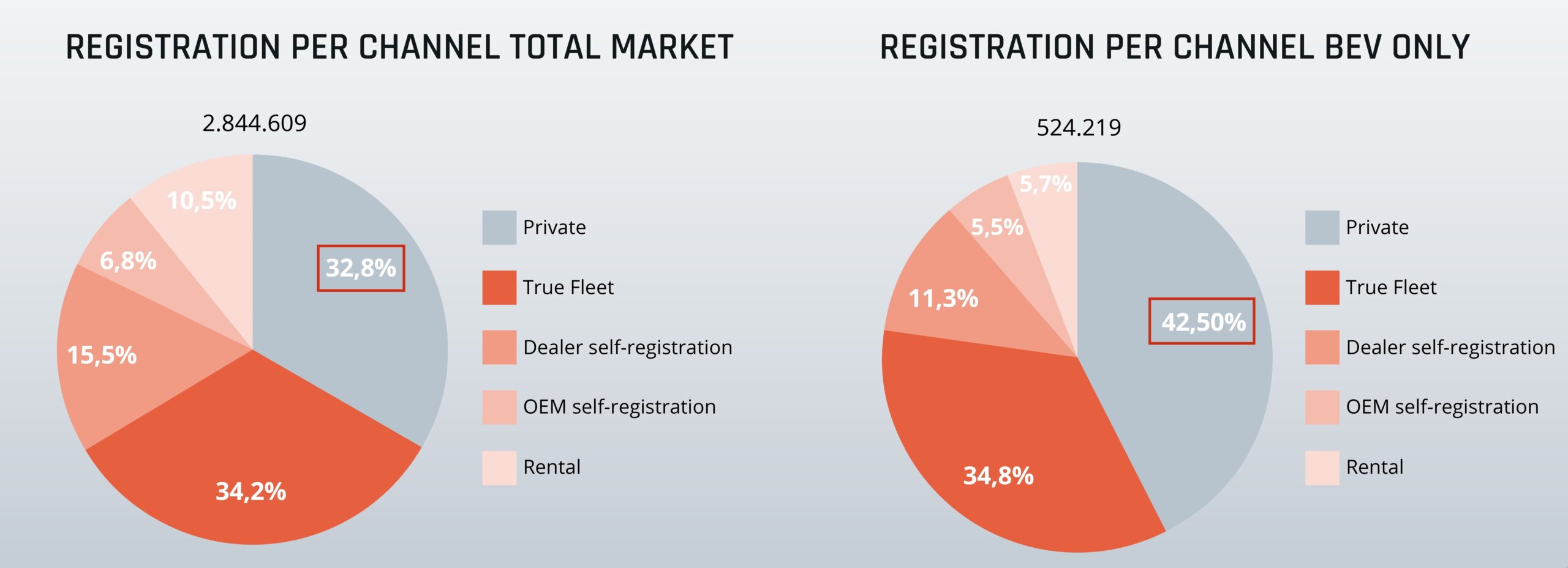

In Germany, less than one third of new vehicles are bought by private customers. On the other hand, more than two thirds of all new cars are registered to corporate customers. The greatest share is the ‘true fleet’ segment, which comprises fleets of company cars, either for particular purposes or as an employee incentive. The second biggest segment comprises vehicles registered for tactical reasons by OEMs or their dealer networks, which are typically brought to the market later with discounts. Rental fleets also make up a relevant part of the total fleet.

Sales Split per channel in Germany in 2023 Total vs. BEV only

Source: Berylls Strategy Advisors, KBA

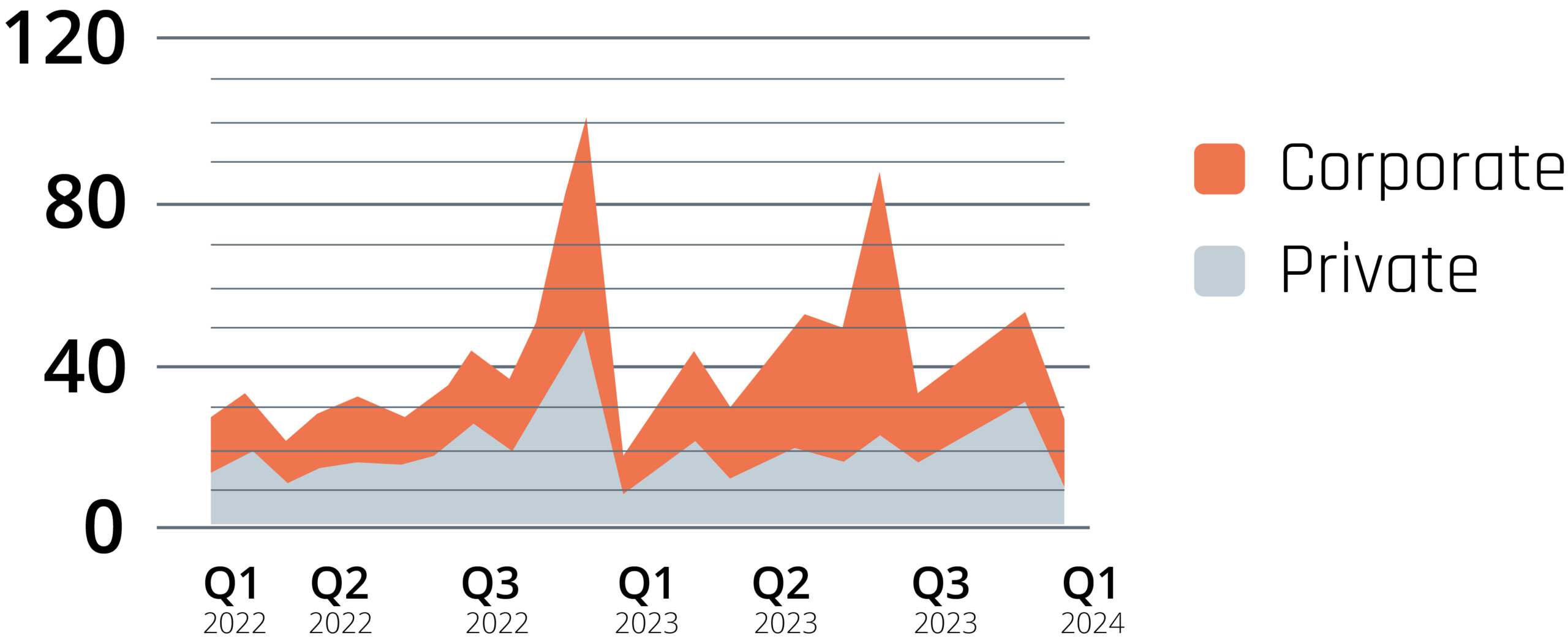

According to information from Dataforce, there was a setback in electrification following the final ending of the environmental bonus (BAFA) in 2023. During the last few months, the bonus was only eligible for private customers, which explains the decrease in the corporate segment. In the private market, the BEV-related share of new registrations fell from 35% in December 2022 to just 11% in December 2023. The share of BEVs in fleet registrations also remains at a low level.

BEV trend in vehicle registrations over the last 24 months in Germany (in thousand)

Source: Dataforce

A large number of these vehicles are sold via lease contracts that are typically returned to the leasing company at the end of the contract. Based on information from Dataforce, in 2023, 29% of private BEV customers opted for a leasing offer while the overall share of private customers taking the leasing option was only 7.2%. In the fleet segment, the majority of vehicles are bought via lease contracts.

In total, that leaves a majority of the residual value risk accumulating with the financial services companies of OEMs (Captives) or independent (Non-Captive) leasing companies.

Automotive dealers and OEMs are therefore currently seeing a drastic decline in demand for used BEVs, which is placing further pressure on resale values. As long as residual values continue to decline, it is hard to make a positive business case for buying a new or almost new electric vehicle due to this value loss. Even the cheaper cost of operation – drastically depending on actual cost for electricity – cannot compensate for this loss.

In an interconnected model, these factors also have an impact on demand and the sales prices of new BEVs.

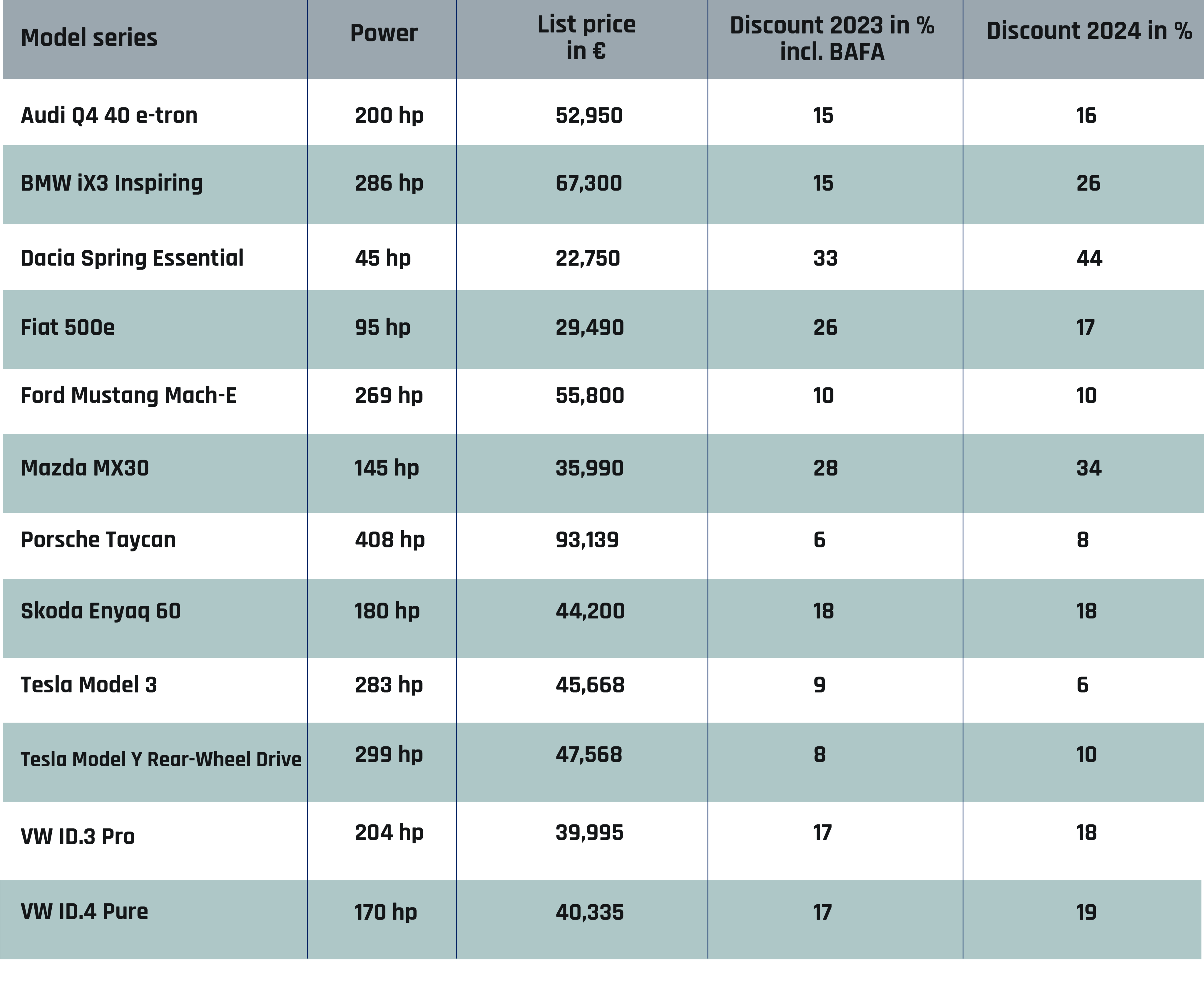

Looking at the current price discounts for new BEVs in Germany, it becomes apparent that OEMs and dealers will need to continue discounting BEVs in order to stimulate at least a certain level of demand. A recent analysis presented by the German newspaper Auto Motor und Sport based on price data from leading automotive platforms (carwow.de, meinauto.de, neuwagen24.de) shows that in January 2024 the average discount was 18% compared with an average discount of 21% in 2023. This point is especially interesting as environmental subsidies (BAFA) were terminated at the end of 2023. Therefore, OEMs and dealers within the German market are giving discounts at their own expense to offset the lack of a government bonus.

Discount comparison for selected BEV models in the German market

Source: carwow.de, meinauto.de, neuwagen24.de; all figures are rounded; last update: January 2024

From our perspective, there are several trends that reinforce one another, limiting the attractiveness of owning a BEV and potentially leading to a carnage in the BEV market in the coming months:

Overall, the outlook for OEMs, their Captives, leasing companies, and auto dealers can appear rather daunting in the next few years with regard to electrification. In order to stay profitable in the BEV market going forward, we at Berylls see several levers that need to be utilized in order to be successful. In our upcoming series, we will further deep-dive into these fields.

Christopher Ley

Christopher Ley joined Berylls by AlixPartners (formerly Berylls Strategy Advisors) in October 2021 as Partner. He has over 14 years of top management consulting experience with focus on new business models and market expansions within the automotive & mobility industry. He is an expert around Vehicle-as-a-Service, comprising vehicle finance & leasing, fleet management and mobility services. Christopher Ley is advising OEMs, Captives, Financial Services Companies, PE & VC Investors, Leasing & Rental Companies, Fleet Managers and Mobility Startups around the transformation from one-time sales towards use-based multi-cycle business models on a global level.

Prior to joining Berylls, Christopher Ley has been working for other international management consulting firms, amongst others Monitor Deloitte and Alvarez & Marsal. He holds a diploma degree in business administration from Johannes Gutenberg-Universität in Mainz and an MBA from Colorado State University.

NO TIME TO READ THIS WEBSITE?