Rightsizing Sales Organizations: From Cost Cutting to Capability Building

Munich, November 2025

T

he automotive industry is at a structural turning point. For decades, growth masked inefficiencies: after the financial crisis, OEMs rebuilt their sales and marketing organizations, adding layers of regional and national headcount to capture rising volumes.

Today, that model has reached its limits. Demand in mature markets is stagnating, competition from new entrants is intensifying, and digital channels are reshaping customer interactions. Established OEMs can no longer rely on scale alone—they must rightsize their sales organizations to align with new realities while building the capabilities for future growth.

Four Drivers of Change

The transformation imperative is being fueled by four powerful forces:

Declining sales: flat demand and intensified competition require restructuring and capacity alignment to avoid overstaffed HQs, regions, and dealer networks.

Regionalization: regulatory and consumer dynamics diverge, requiring semi-autonomous regional sales units and localized go-to-market strategies.

Sales model uncertainty: as direct-to-consumer and agency models evolve, OEMs must balance control of pricing, brand, and data against rising distribution costs.

Digitalization & AI: advanced analytics, chatbots, and automation are reshaping the sales funnel, reducing the need for manual processes and enabling data-driven decision making.

Together, these forces mean that traditional sales structures—often centralized, overlapping, and headcount-heavy—are no longer fit for purpose.

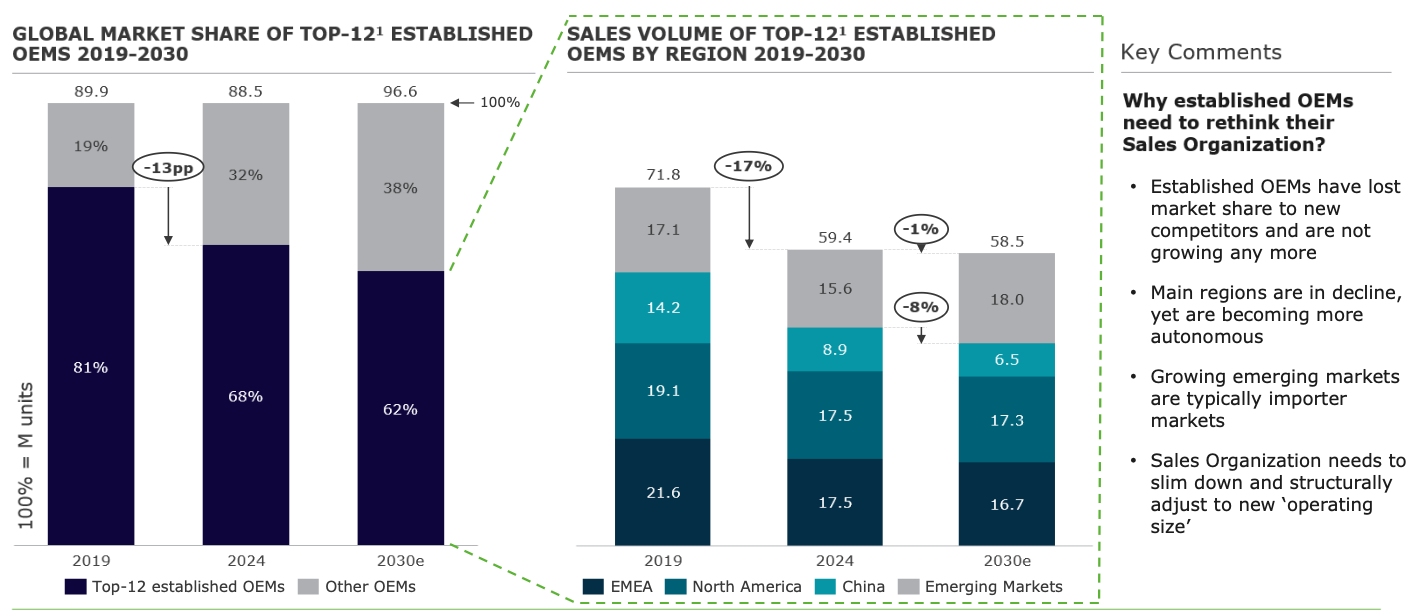

Deep Dive Declining Sales:

The end of growth through growing competition drives the necessity to reorganize Sales Organization across the entire sales chain

¹ Top-12 OEM established OEMs including Toyota, VW Group, Hyundai, Renault-Nissan-Mitsubishi, Stellantis, GM, Ford, Honda, Suzuki, BMW, Mercedes, Mazda

Source: AlixPartners / Berylls by AlixPartners analysis; S&P(IHS)

A Shrinking but More Demanding Market

“Streamlining retail standards across corporate groups and maintaining tight budget control are becoming essential for operational efficiency and profitability.”

- CSO, Volume OEM

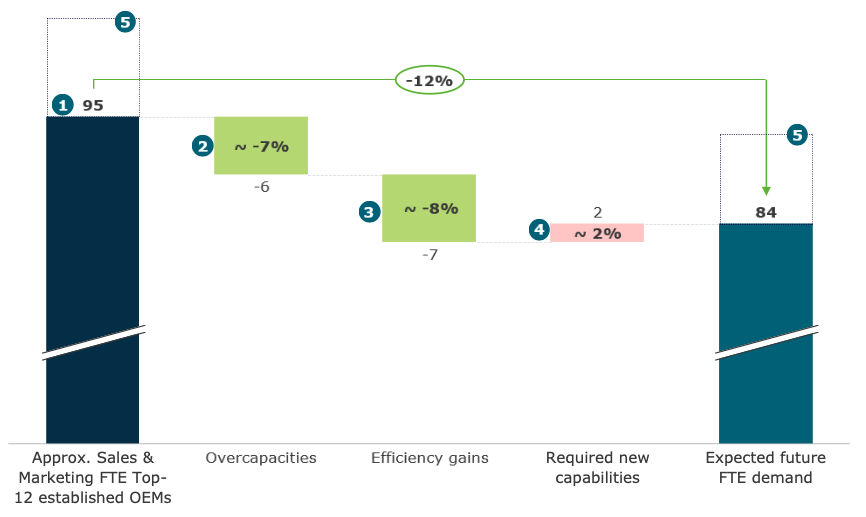

The Sales & Marketing organizations of the Top-12 established OEMs employ around 95,000 people today. But the landscape is shifting fast. With declining sales volumes, overcapacities are becoming visible – an estimated 7% of roles are at risk. In parallel, efficiency gains of about 8% can be unlocked through new operating models, automation, and the increased use of digitalization and AI.

However, the picture is not only about reductions. Roughly 2% of future demand will be created by the need for new capabilities – in areas such as AI, data analytics, and digital expertise. This signals a clear direction: while traditional roles will decline, demand for tech-driven skills is growing rapidly.

In total, the expected future demand is around 84,000 FTEs, reflecting a net decrease of 12%. The implications are clear – OEMs will need to actively manage this transition, balancing efficiency gains with investments in reskilling and capability building. At the same time, further job losses are likely to occur at service providers, as OEMs continue to optimize their own headcount by outsourcing.

Estimated own Sales & Marketing FTE of Top-12 established OEMs1 and future demand (in k FTE)

¹ Top-12 OEM established OEMs including Toyota, VW Group, Hyundai, Renault-Nissan-Mitsubishi, Stellantis, GM, Ford, Honda, Suzuki, BMW, Mercedes, Mazda Source: AlixPartners / Berylls by AlixPartners

At the same time, market dynamics are diverging. Regional regulatory frameworks, shifting customer expectations, and competitive pressures demand more localized, agile approaches. OEMs face a dual challenge: reduce structural overcapacity while equipping organizations with the digital and analytical skills needed to compete in a more fragmented, data-driven environment.

Three Emerging Organizational Archetypes

To respond, OEMs are experimenting with new organizational blueprints:

1. Market-led – full local ownership and accountability, giving national sales companies (NSCs) end-to-end responsibility.

2. Region-led – consolidated regional hubs with lean field structures, balancing efficiency with local responsiveness.

3. HQ-led – centralized control with AI-enabled processes, shifting many functions directly to HQ for scale and cost advantages.

Source: AlixPartners / Berylls by AlixPartners

Each archetype comes with trade-offs. The right choice will depend on market exposure, product portfolio, and the degree of control OEMs want to retain over pricing and customer data. But across all models, the trend is clear: leaner structures, fewer overlaps, and stronger digital enablement.

Rightsizing ≠ Cost Cutting

Rightsizing should not be equated with simple headcount reduction. While efficiency gains will reduce structural costs—AI-driven automation alone could replace up to 8% of current sales roles—the true opportunity lies in capability building. OEMs must reinvest savings into future-critical skills:

Data analytics & AI operations – to optimize pricing, lead management, and campaign effectiveness.

Digital customer engagement – to bridge the gap between online interest and retail conversion.

Agile organizational skills – to adapt quickly to regional dynamics and new sales models.

In this context, rightsizing is less about cutting fat and more about building muscle: creating lean, capability-driven sales organizations that can outperform in a digital-first, regionally fragmented market.

A New Operating Model for Sales

The future sales operating model will combine the best of both worlds—dealers, direct-to-consumer, and agency approaches—tailored by market. It will decouple regional development, allowing greater autonomy where needed, while leveraging AI, automation, and data-driven processes at scale.

OEMs that succeed will not only reduce costs but also unlock efficiency gains, improve customer retention, and ensure they remain competitive in a world where new entrants and tech-driven players are redefining the rules of automotive sales.

From Overcapacity to Future Readiness

The end of growth as usual means OEMs can no longer afford bloated, overlapping structures. Rightsizing is inevitable—but its true value comes when it is combined with capability building. By aligning organizational size with market realities and reinvesting in digital skills, OEMs can transform sales organizations from cost centers into competitive weapons.

The winners of tomorrow will be those who move fastest today: slimming down, smartening up, and preparing their salesforce not just for survival, but for sustained advantage in a transformed industry.