EV democratization is fading in the West: Is the race already lost?

Munich, January 2026

E

lectric mobility is expanding globally, but along divergent paths. In Europe and the United States, BEV adoption follows a top-down model, concentrated in higher-priced premium segments (D-E) under the automotive A-F segmentation, which classifies vehicles by size, price, and comfort, with F representing the highest luxury tier.

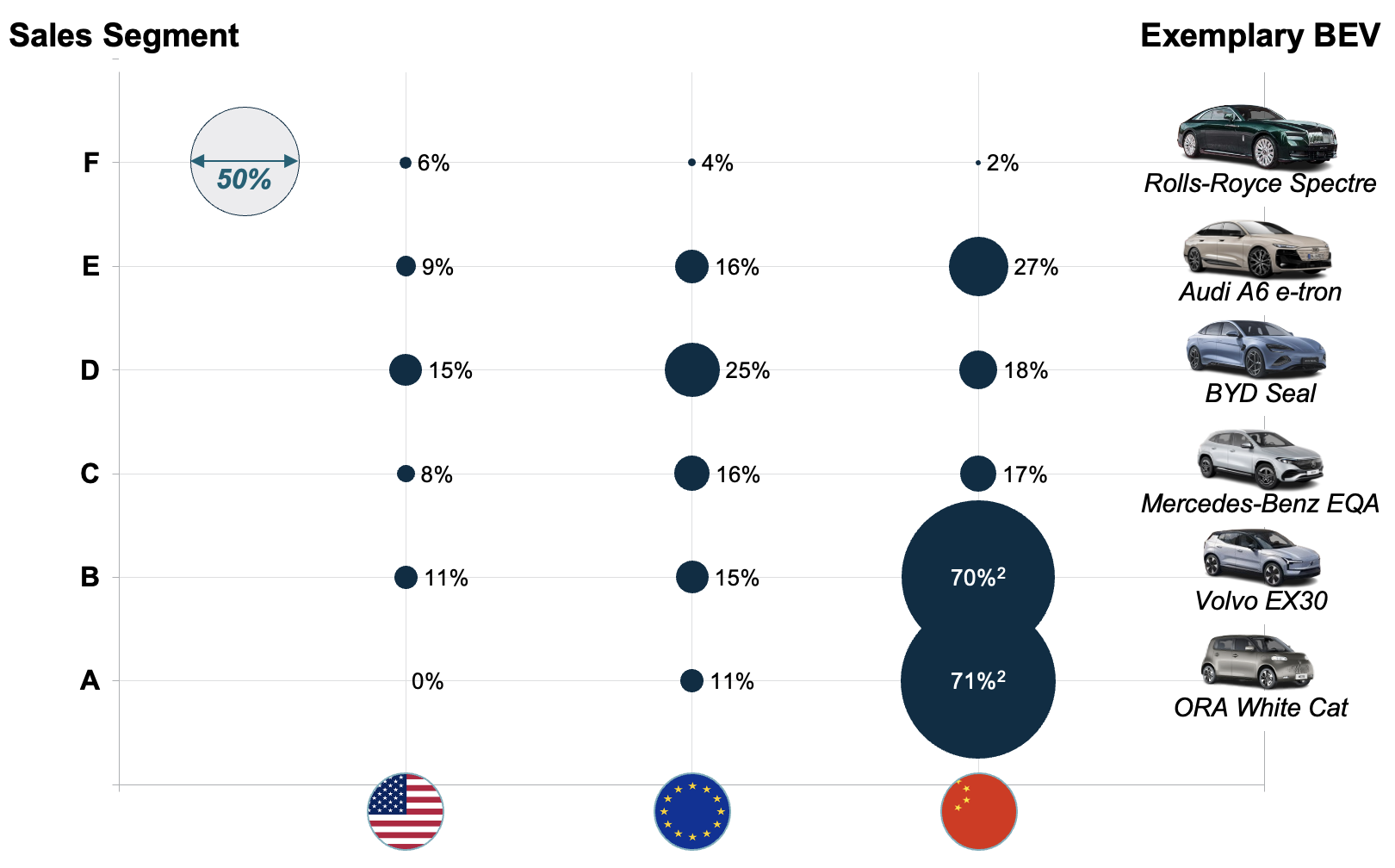

China, in contrast, is electrifying from the bottom up: entry-level segments (A-B) account for 38.1% of BEV sales, supported by electrification rates of 71.1% in the A-segment and 70.3% in the B-segment. This focus on affordability and scale enables broad adoption, faster learning curves, and rapid volume growth.

Figure 1– BEV sales share by region within respective sales segment across the United States, Europe and China, 2025.

¹ Only sales share depicted from 0-100%, no absolute sales figures shown. ² Entry-level segments in China are almost entirely Chinese-origin (Seg. A: 100%, Seg. B: 95%).

Source: Berylls by AlixPartners analysis based on S&P global LV sales

This difference is no longer a marginal observation. It is shaping market dynamics, cost structures, and long-term competitiveness in the global automotive industry. At its core lies a simple question: are electric vehicles becoming a mass-market solution, or do they remain a premium product for a narrow customer base?

Premium dominates BEV adoption in the US and Europe

In the United States and Europe, BEV demand is concentrated in mid-size and premium segments, mainly larger sedans and SUVs. Both regions show the highest EV shares in the D segment, with 15% and 25%, respectively. This is economically rational for manufacturers, as higher-priced vehicles better absorb battery and technology costs and protect margins. This leads to a distortion of the market towards more premium vehicles among BEVs: The share of the D-segment among BEVs is 8%p (Europe) and 14%p (US) higher compared to a total market view, also including combustion engine vehicles.

The downside however is weak penetration in smaller, high-volume segments. The U.S. illustrates this clearly: electrification lags not due to technology limits, but because affordable entry-level BEVs are scarce and consumer preferences strongly favor pickups and large SUVs. Due to this, the A- and B-segments are traditionally small in the US (combined market share of 5% in 2025). However, lagging electrification is showing also in the large C-segment (38% of total market), highlighting problems with entry-level BEVs on this market.

Europe reaches a similar outcome for different reasons. While small segments matter more than in the U.S. (combined market share of 34%), BEV demand is heavily influenced by company car taxation. In markets such as Germany, company cars represent over 53% of new BEV registrations, reinforcing demand for larger, better-equipped vehicles and skewing the BEV mix toward premium segments.

China’s bottom-up electrification model

China follows a fundamentally different electrification path. Small and compact electric vehicles dominate everyday mobility, supported by dense cities, short driving distances, and a well-developed charging network that makes entry-level BEVs practical and economical. Electrification has therefore advanced fastest in smaller vehicle segments, where BEV penetration is already very high and electric powertrains dominate in some categories. This shows especially in the A&B segment. With a combined market share of 14% across all propulsion types, these segments are not the most attractive from an OEM perspective, at least on first look. However, these segments make up over 38% of the BEV market, driven by a high BEV sales share of 70%+ in both segments (see figure 1).

This scale-driven approach has accelerated learning and cost reduction, turning BEVs into a mainstream mobility solution rather than a premium niche. Structural cost advantages – an integrated domestic supply chain, strong battery manufacturing, and widespread use of cost-efficient LFP chemistry – enable Chinese OEMs to price BEVs aggressively while sustaining scale.

Why Western markets struggle to replicate this approach

The divergence between China and Western markets is structural, shaped by market design, incentives, and policy. High upfront investments have pushed Western OEMs toward premium vehicles to protect margins, slowing mass-market electrification. Policy frameworks reinforce this: Europe’s 2035 target offers long-term direction but weak near-term pressure, while U.S. incentives are constrained by price caps and sourcing rules.

China, in contrast, has consistently driven mass-market electrification through stable policy, infrastructure investment, and industrial coordination – making small vehicle segments the core of large-scale adoption.

How the picture evolves toward the end of the decade

Looking ahead, global BEV adoption will become more balanced, but regional differences will persist.

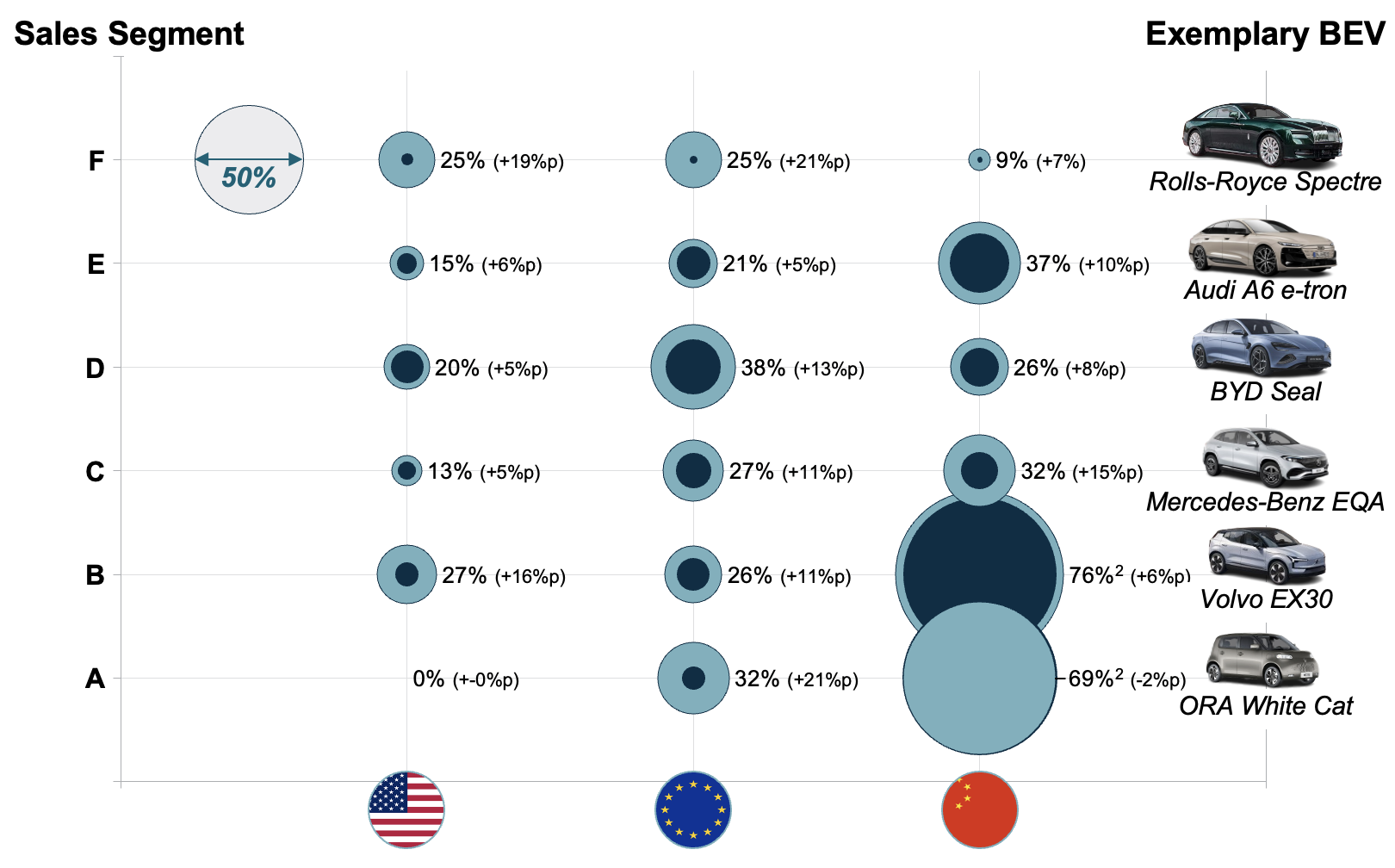

Figure 2 – BEV sales share¹ by region within respective sales segment, 2025 vs. 2030

¹ Only sales share depicted from 0-100%, no absolute sales figures shown. ² Entry-level segments in China are almost entirely Chinese-origin (Seg. A: 100%, Seg. B: 94%).

Source: Berylls by AlixPartners analysis based on S&P global LV sales

The United States is likely to remain the slowest major BEV market, with adoption polarized between premium models and a limited set of lower-end offerings due to affordability, infrastructure, and segment constraints. In the largest market segments (C/D/E), the BEV sales share growth is at 6&p or lower until 2030.

Europe, on the other hand, is on a broader electrification trajectory. BEV adoption is expanding across all segments by 2030 and driving a gradual shift toward near-complete fleet electrification within the next decade. In every segment except for the E-segment, the BEV share will grow by double-digit percentage points until 2030.

Lastly, China is entering a new phase: Having almost entirely electrified lower segments by 2025, Chinese fleet electrification is moving upmarket, intensifying competition in mid-size and premium segments domestically and internationally. Even though the electrification growth in the C-/D- and E-segments are comparable to Europe over the next five years, the continent will still be ahead based on higher BEV shares from the get-go (except for the D-segment).

Strategic implications for Western manufacturers

The global shift to electric mobility is becoming structurally asymmetric: Europe is slowly advancing toward full-fleet electrification, China is moving up the automotive value chain, and the United States risks falling further behind.

For Western OEMs, the question is no longer whether to electrify, but how. Long-term competitiveness depends on closing the affordability gap in lower segments while defending premium positions against increasingly capable Chinese competitors. At the same time, China remains a critical strategic market – both as the world’s largest BEV ecosystem and as the primary source of competitive pressure as Chinese OEMs expand into Western markets.

The window remains open but is narrowing. Without a credible path to mass-market electrification, the democratization of electric mobility in the West will remain incomplete, with lasting competitive consequences.